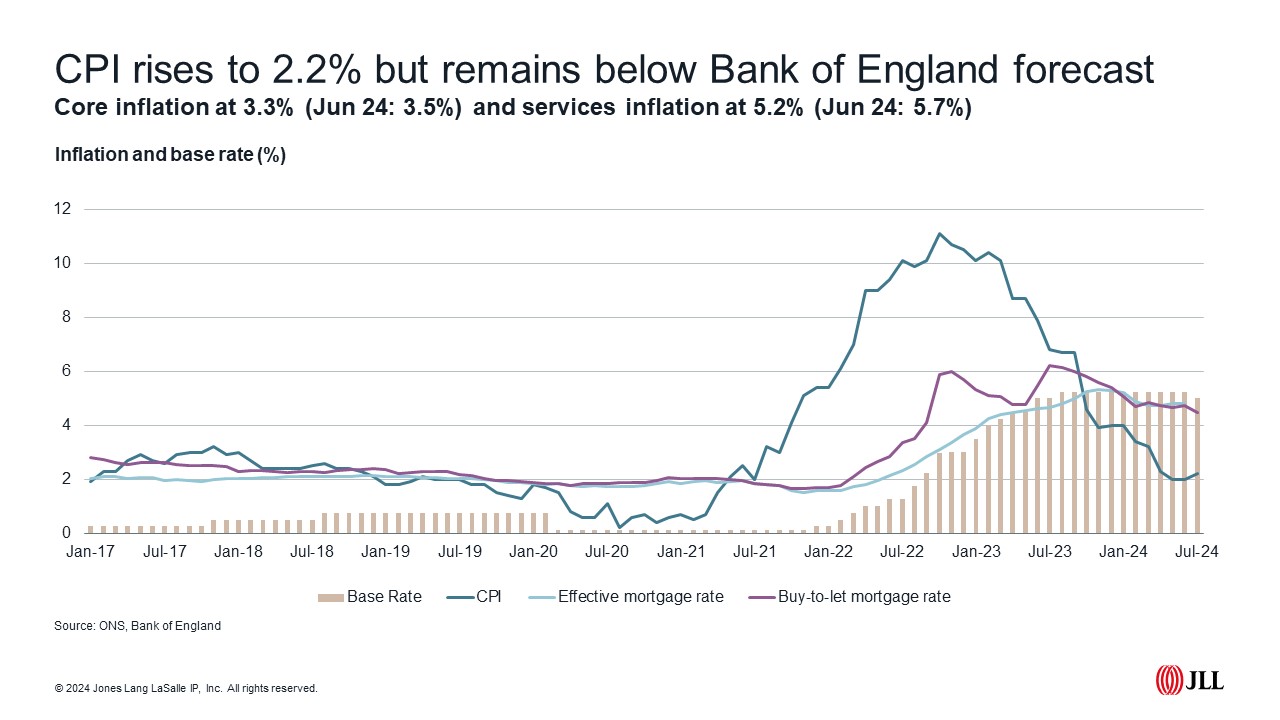

On the face of it the July inflation figures could give cause for concern, with CPI (Consumer Prices Index) rising for the first time this year, from the 2% Bank of England target in June to 2.2% in July. But dig a little deeper and there is more positivity in the numbers. Forecasters expect inflation to hover somewhere between 2% and 2.75% for the rest of the year, and the July figure is lower than the 2.4% the Bank predicted.

The outlook is more positive for services inflation, too (an indicator that has been watched closely by rate setters on the Monetary Policy Committee) with the July figure of 5.2% down from 5.7% in June and lower than the forecast of 5.6%. Will that be enough to convince the MPC to cut rates further when they meet next month? So far, the markets are doubtful, but further cuts later in the year remain on the cards.

UK unemployment fell to 4.2% in July, again below the Bank of England’s forecast of 4.4%. Total earnings, including bonuses, rose 4.5% in the latest three-month period. This is the lowest figure since November 2021 but still higher than the Bank would like, throwing more cold water on the likelihood of a September rate cut. Total pay in the private sector was up 5%, down from 5.6% previously.

GDP rising

The UK economy grew by 0.6% in the three months to June, following a 0.7% increase in Q1. The services sector was the key driver behind growth, rising 0.8%, with both manufacturing and construction posting a marginal fall of 0.1% (although worth remembering this was pre-election and pre-rate cut). Annually, this means real GDP is estimated to have risen 0.9%. There is good news on per capita GDP growth, too, rising for the second quarter running, albeit still down 0.9% on pre-pandemic highs.

What does this mean for my mortgage?

The Bank of England’s rate cut has started to feed through into the mortgage markets. Five-year fixes for those with healthy deposits are now available at below 3.9%, with best-buy two-year equivalents sitting at circa 4.3%.

More activity?

The latest data from the S&P Purchasing Manager Index (PMI) suggests activity in the construction sector continues to increase. Its latest release shows activity rising for the fifth consecutive month in July. More activity has also led to increases in recruitment, with firms reporting a rise in staffing levels for the third consecutive month. Housebuilding, which had lagged the commercial sector, has now also entered growth territory.

Rental Market

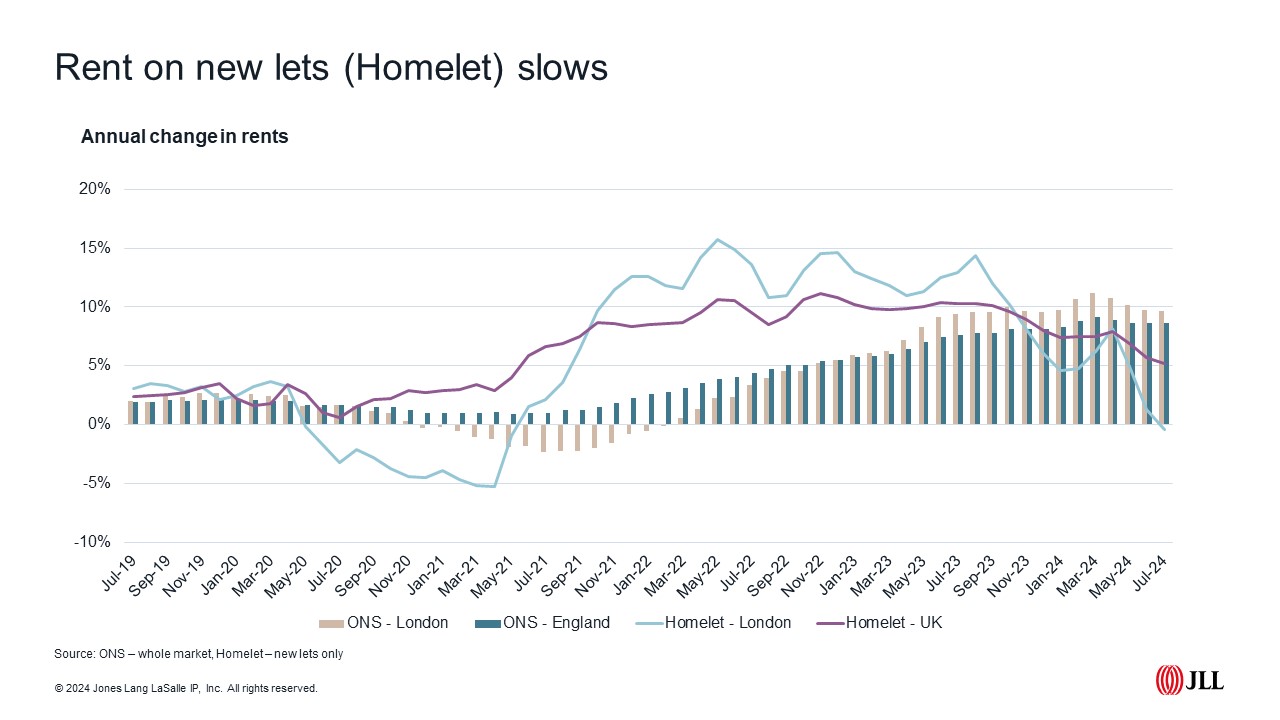

Overall rental growth remains high and unchanged at 8.6%, according to the latest figures from the ONS (Office for National Statistics), but new lets data tells a different story, particularly in London. Rental growth among new lets has fallen from 5.7% to 5.2% nationally over the last month, dragged down especially due to London registering a negative reading (-0.4%) for the first time since May 2021. Despite this, RICS (Royal Institution of Chartered Surveyors) survey data shows a positive net balance of respondents who expect rents to rise in the coming months, including in London.

House prices up

Rightmove figures show an increase in activity in July, with the number of sales agreed up 15% on the same period a year ago. The Land Registry House Price Index remains unchanged, with annual growth of 2.7% in June – the fourth consecutive month with rising prices. Nationwide and Halifax indices similarly show growth of more than 2% annually.

Investor activity

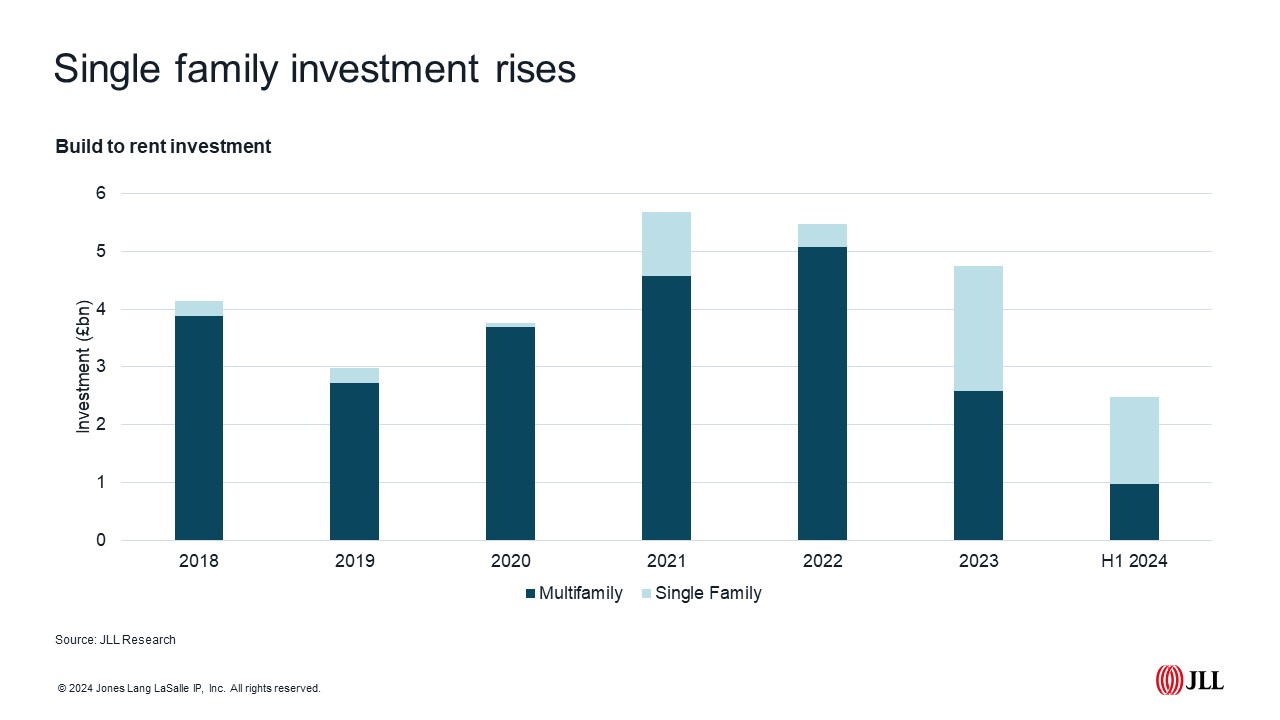

The Living sector continues to draw investment. The latest JLL figures show investment in Living account for 30% of total real estate investment in H1 2024. The build to rent sector continues to grow, with the number of operational units rising 24% in Q2 2024 compared with the same period in 2023.

But the multifamily sector faces many similar challenges to new homes, with high debt cost, increasing regulation and uncertainty over build costs impacting activity in the sector. As a result, the number of units in the pipeline (planning approved or under construction) dropping 12% annually in Q2.

As many of the challenges facing the multifamily sector unwind (a little), investment in single family has continued apace. UK single family investment topped £1.5 billion in the first half of 2024, accounting for more than half of total build to rent investment in H1, with the second quarter this year seeing record single family investment of £826 million. To read more Click here.