But as the removal vans manoeuvre into No. 10, many in the industry will be thinking about the housing market and what the incoming Labour government will bring. Of course, housing was high on the agenda in the run up to the election, but the vagaries of the manifesto will now need to make way for greater clarity.

The new Prime Minister had previously committed to turbocharging the housing market from “day one”. Realistically, we might be waiting a few days longer to find out Sir Keir’s plans. But those close to the top have signalled an announcement could be a matter of a few weeks rather than a few months away.

They’ll need to pull their socks up as building 1.5 million homes over the next parliament will be a Herculean task. The main plans touted so far have been a recruitment drive for planners, with the intention to recruit 300 additional planning officers to ease bottlenecks and get Britain building. Undoubtedly a recognition of the challenges in the planning process, in practice this is the equivalent of less than one planner per planning authority and may not be the game changer we really need (a step in the right direction though).

The term grey belt is also likely to enter the vernacular as Labour attempt to make developing on the greenbelt more palatable (their landslide victory and corresponding majority will help here).

Plans are afoot, too, for encouraging first-time buyer activity through further promotion of a mortgage guarantee scheme. However, the temporary increase in the first-time buyers stamp duty threshold (from £300k to £425k) won’t be extended under Labour – although this mostly affects higher value markets.

Before we delve too deeply into what-ifs we’ll need to wait and see what emerges in the coming weeks. Until then, let’s look at what the new government are inheriting:

The economy

Whisper it quietly, but things might not be quite as bad as we thought. The new Labour government aren’t inheriting an economy in rude health, but quarterly GDP growth for Q1 was revised up in June to 0.7% (from 0.6%), putting GDP 0.3% higher than it was a year earlier in Q1.

With growth revised up, expectations of economic growth at sub 1% in 2024 may be looking conservative. Oxford Economics expect 0.9% and consensus forecasters 0.5% this year, but we could well see these figures creep up as we move through the summer.

Despite CPI hitting the 2% target rate, stubborn services inflation has thrown some cold water on the prospect of multiple rate cuts this year. But we still expect the bank rate will be cut before the year end, meaning more favourable mortgage rates, which are already starting to creep into the market, continue to emerge in the second half of the year.

House prices

House prices edged up in June, 0.2% higher month-on-month and 1.5% higher than they were at the same point a year ago. The latest figures from Nationwide show London was the only region in southern England where prices have risen in the last 12 months, up 1.6%. East Anglia saw the most significant annual fall at -1.8% with the North West and Northern Ireland both recording annual increases of 4.1% in Q2 2024.

House prices have risen 59% since Labour were last in power back in 2010. They are up 68% since they last won an election back in 2005 and up 353% since the last won an election in opposition back in 1997. In 14 years under the Conservatives (2010 to

2024) prices have risen by 57%, versus 191% in the 13 years under Labour (1997-2010)

Activity

Mortgage approvals for house purchase continue to hover around the 60,000 mark, around 10,000 (or 19%) higher than they were a year ago. Despite rising off a low base, activity remains around 15% down on long-run norms.

The number of transactions has risen too so far this year. The latest May figures show an estimated 91,660 sales, 24% (or almost 18,000) higher than volumes in May last year and just 2% shy of the 2015 to 2019 average.

The latest S&P Global Construction Purchasing Managers’ Index (PMI) was released the day we went to the polls. The UK construction sector remained in growth territory for the fourth consecutive month in June, albeit dipping slightly month-on-month. Growth was led by the commercial sector, with housing, which had moved into positive territory for the first time in 19 months in May, dropping back in June.

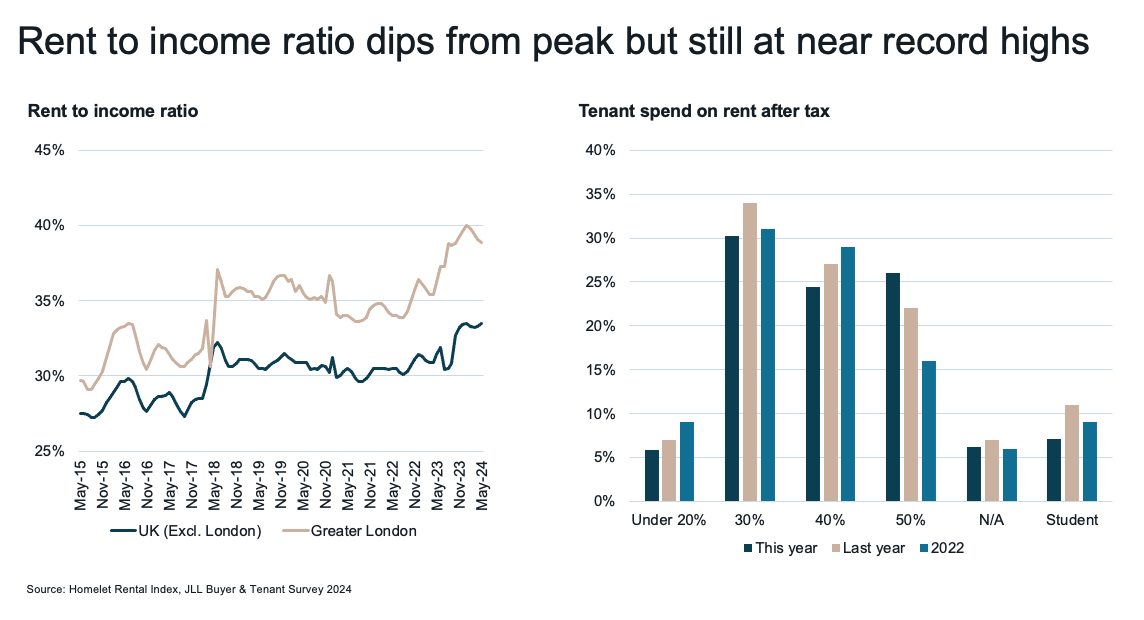

Rents

As we enter the busy summer market for lettings, prices achieved on new lets, according to the latest June figures from Homelet, were up 6.9% nationally. London and the South West were the only regions where rents fell month-on-month but were still 4.9% and 3.4% higher annually.

Rental growth rates in London have finally dropped below wage growth, meaning the rent to affordability ratio dropped from 40% in January to 38.9% in May, but it remains 10 percentage points higher than it was a decade ago.

Results for the latest JLL Buyer and Tenant Survey highlight the challenge facing tenants, with half of the tenants surveyed spending more than 50% of their take home pay on rent each month, up from 45% in 2022. To read more from the latest JLL Buyer and Tenant Survey click here.