UK inflation, which had been coming in below forecast earlier this year, spiked according to the latest April figures. This wasn’t unexpected, with the impact of higher energy costs alongside annual increases in council tax and rail fares contributing to the 3.5 per cent rise.

The optimist’s view is that this could be short lived though, with Ofgem announcing a 7 per cent reduction in the energy price cap between July and September this year, compared to a 6 per cent rise in the three months to June.

Higher than expected CPI figures follow news that the UK economy grew by 0.7 per cent in Q1 2025, above the 0.6 per cent forecast and 0.1 per cent recorded in Q4 2024. But policy change, both domestically and internationally, means the path for the remainder of 2025 is far from clear, with the impact of employer NI and tariffs still to play out in the GDP figures in the coming months.

Housing market

The post-stamp duty change hangover appears to have been short lived, with the latest figures from Zoopla showing the number of sales agreed in May at their highest level for four years and up 6% on 2024. Sellers are returning to the market too, with new listings up 6% and stock on the market 13% higher than at the same point a year ago.

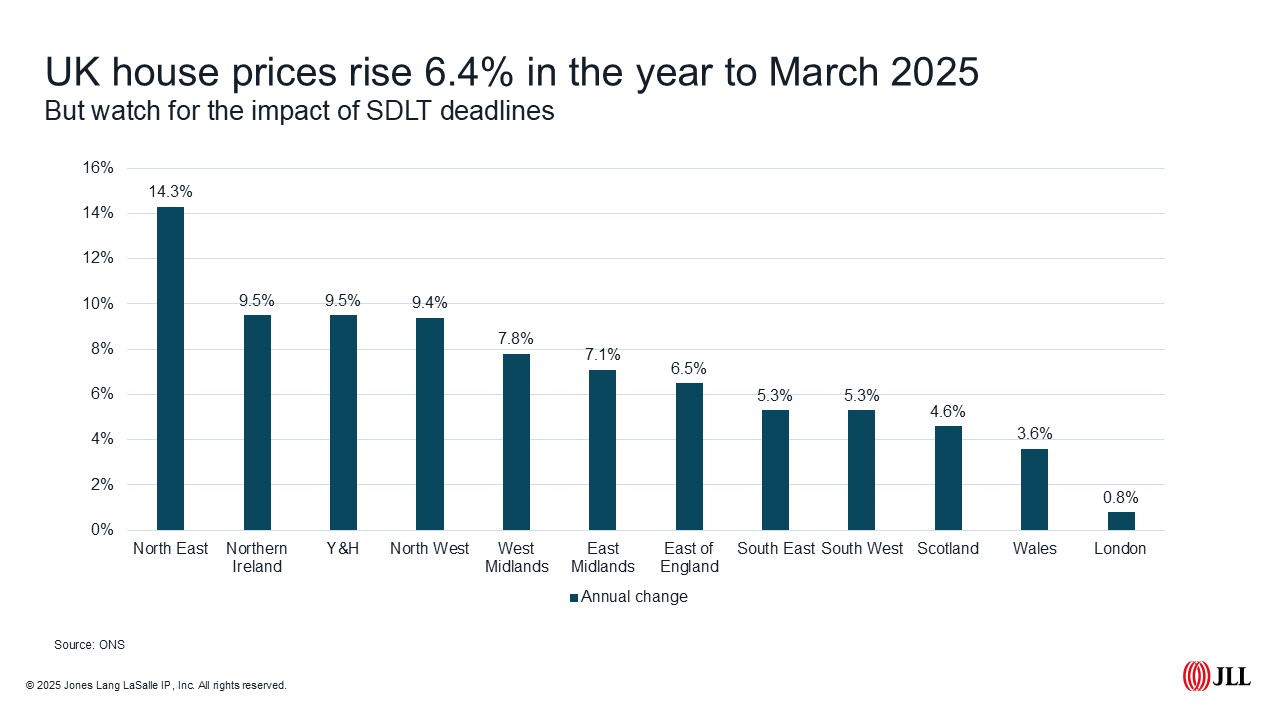

The latest ONS figures for March show average UK house prices rose 6.4 per cent annually to £271,000, equating to a £16,000 increase on March 2024. First time buyer prices rose 7.1 per cent, outpacing growth for home movers (5.4 per cent). Although it is worth noting the impact of the 1 April stamp duty change on these figures.

For rents, the ONS Private Rents Index showed an annual increase in rents of 7.4 per cent in the 12 months to April 2025. This is down from 7.7 per cent in March but continues to remain elevated compared with new let indicators, with April figures from Homelet up just 0.3 per cent annually.

Time to rethink incentives?

The government has made clear commitments to building more homes and improving the quality and efficiency of our existing housing stock. However, the responsibility for building this stock lies predominantly with housebuilders, who have responsibilities to their shareholders and need to ensure there is a market for any homes they deliver. Whether that be for open market sale, investment, or sales to affordable housing providers.

The cost to improve existing stock also lies (a few government subsidies aside) with property owners. Whether that be housing associations or other social housing providers, who need to improve stock without any demonstrable increase in rents, or owners in the private sector.

The government has clear ambitions to achieve a blanket EPC C+ rating for the private rented sector and social housing, but if we are serious about encouraging and rewarding improvements, we’ll need to rethink how we approach this going forward.

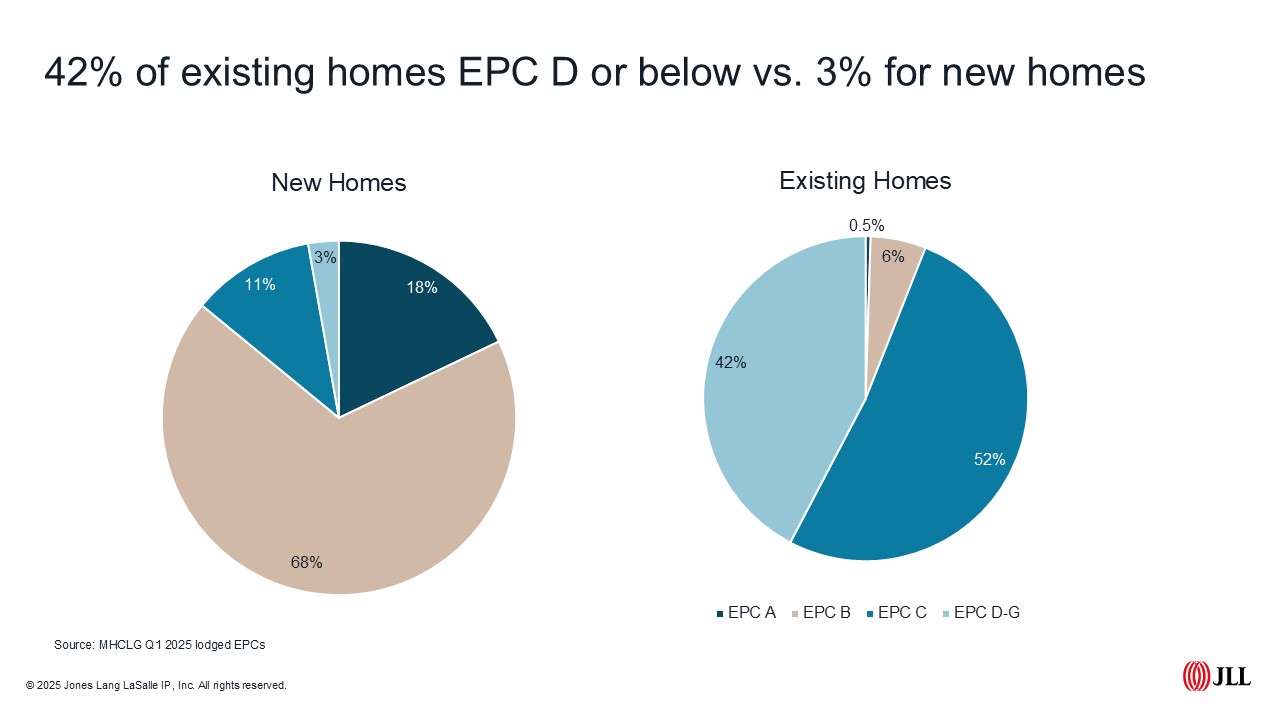

New homes are already a step ahead, with 97% of new homes delivered having an EPC of C or above, with 86% rated A or B in Q1 2025. This compares with 6% EPC A or B and 52% EPC C for existing homes.

To encourage purchasers to buy new and more energy efficient homes, or to reward homeowners for investing in improving the energy efficiency of their homes should we be offering Stamp Duty Land Tax (SDLT) incentives to encourage activity and improvements?

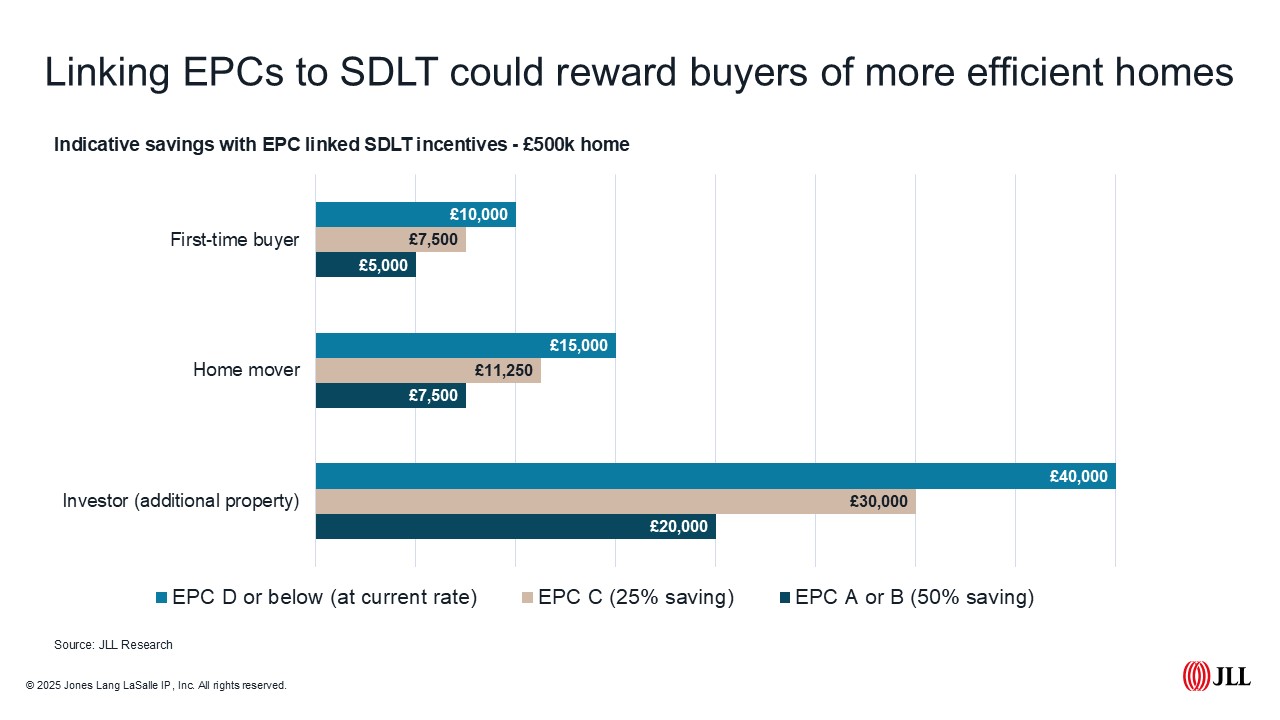

Cutting SDLT by 50% for A or B rated properties, and by 25% for those rated C could provide a clear incentive for buyers and rewards sellers too. Those bringing homes to market at EPC C or above may be more likely to attract buyers due to lower running costs and reduced purchase costs.

What difference could this make?

If implemented, a first-time buyer purchasing a home at £500,000 could save £5,000 buying an EPC A or B rated home, with home-movers paying £7,500, compared with £15,000 for a home rated D or below. Perhaps a harder sell for government would be applying this to investors too, but if we are looking to improve the quality and efficiency of our rental stock offering the same reduction in SDLT would further encourage the purchase of more efficient homes. An investor buying a £500,000 EPC A or B rated property would still be paying four times the SDLT of a first-time buyer, but saving £20,000 compared with an EPC D home.

But what about the black hole?

We understand that discussions on tax breaks at a time when government finances are increasingly stretched could be challenging. However, even if stamp duty take per property fell, more activity means the difference between overall receipts may not be as significant. Indeed, encouraging activity in the housing market brings in far more revenue than SDLT alone, providing a boost for the wider economy as well as helping to deliver more better-quality homes. We’ll hopefully know more following the June Spending Review, but in the meantime, we hope that the Government are considering demand and as well as supply when thinking about how to deliver more homes.

JLL Research

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.

Disclaimer: © 2025 Jones Lang LaSalle IP, Inc. All rights reserved. Data within this report is based on material/sources that are deemed to be reliable and has not been independently verified by JLL. JLL makes no representations or warranties as to the accuracy, completeness or suitability of the whole or any part of the report which has been produced solely as a general guide and does not constitute advice. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. JLL, its officers, employees shall not be liable for any loss, liability, damage or expense arising directly or indirectly from any use or disclosure of or reliance on such report. JLL reserves the right to pursue criminal and civil action for any unauthorized use, distribution or breach of such intellectual property.