As has become customary, anticipation is building in the run-up to the 7 August meeting of the Bank of England’s Monetary Policy Committee.

Markets still appear to be on the side of the doves, expecting a further reduction in the bank rate next month, but recent announcements on the UK economy have muddied the waters.

Inflation, which came in a little hotter than many had expected in June, could trouble the MPC. CPI rose 3.6 per cent, with the three f’s: fuel, flights and food all contributing. Yet despite inflation rising, GDP, jobs and wage growth all fell

back in the latest numbers. Growth in UK GDP, which had shown some promise in Q1 fell for the second consecutive month in May, down 0.1 per cent, following a -0.3 per cent reading in April. Real GDP is still expected to have grown 0.5 per cent in

the three months to May, albeit much of this is down to a stronger Q1. But the outlook for UK GDP has improved marginally this year, with consensus forecasts expecting 1 per cent growth this year, up from 0.8 per cent in 2024.

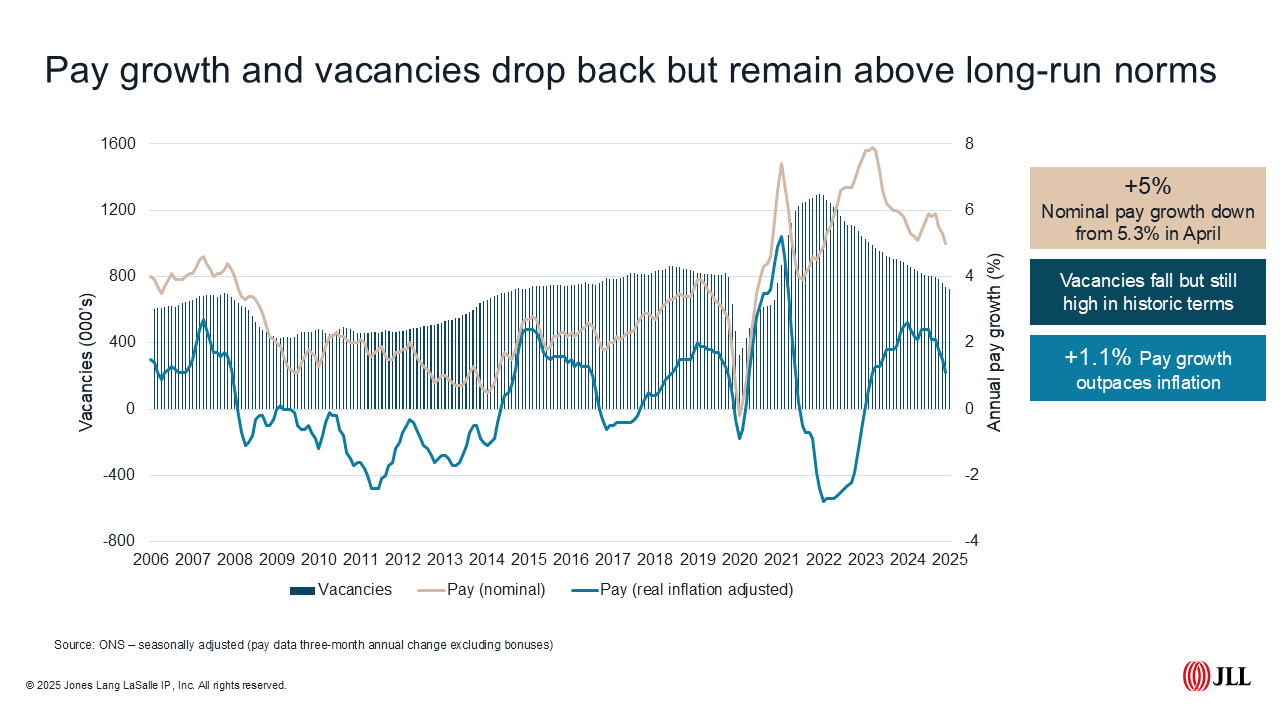

Wage growth dropped back in the latest figures, with average earnings excluding bonuses 5 per cent higher in the three months to May compared with the same period a year earlier. This was lower than the 5.3 per cent recorded in April. The ONS Labour Force Survey, which I’d approach with caution due to low participation rates at present, showed unemployment rose to 4.7 per cent in the three months to May, up from 4.6 per cent a month earlier.

Fallout from the rise in employers’ national insurance, combined with ongoing uncertainty around tariffs and the health of the global economy has seen the number of payrolled staff fall in May, with a 25,000 reduction in May versus April. Yet this is lower than previous estimates of more than a 100,000 drop. The latest major announcement was the loss of 500 jobs at Jaguar Land Rover, which posted an 11 per cent reduction in quarterly sales following the pausing of US exports.

Early estimates suggest we could see a further reduction in June, with the number of payrolled staff expected to be 178,000 lower in June this year than last, or a reduction of 0.6 per cent. This follows a fall in job vacancies for the 36th consecutive month, albeit setting aside pandemic disruptions, we remain at or above long run norms.

News from Mansion House

In her annual speech to business leaders at Mansion House, the Chancellor’s key theme was loosening regulation to turbocharge growth. Much of the emphasis was around supporting our ailing IPO sector and encouraging investment in the UK stock market rather than cash ISAs, albeit not as previously trailed limiting the cash ISA allowance (yet).

For the housing market, there was some loosening agreed too. Income thresholds for those applying for certain first-time buyer mortgages will be lowered and more mortgages will be available at over 4.5 times income. A move which is expected to provide

up to 36,000 additional mortgages to first-time buyers in its first year. In addition, a new mortgage guarantee scheme has been confirmed to ensure the ongoing availability of loans at 90 and 95 per cent loan-to-value to assist prospective buyers

with lower deposits.

Where have all the flats gone?

There was some encouraging news in the latest S&P Purchasing Managers Index. While overall construction activity remained in contractionary territory housebuilding moved into growth territory for the first time since September 2024.

But an increase in activity, which will be welcomed by a government sticking steadfastly to their 1.5 million homes target, is not evident in our cities. Ongoing viability challenges, particularly around ‘High Risk’ buildings – those at 18 metres or seven storeys high – and increasing frustrations with the Gateway process and the Building Safety Regulator mean activity is falling.

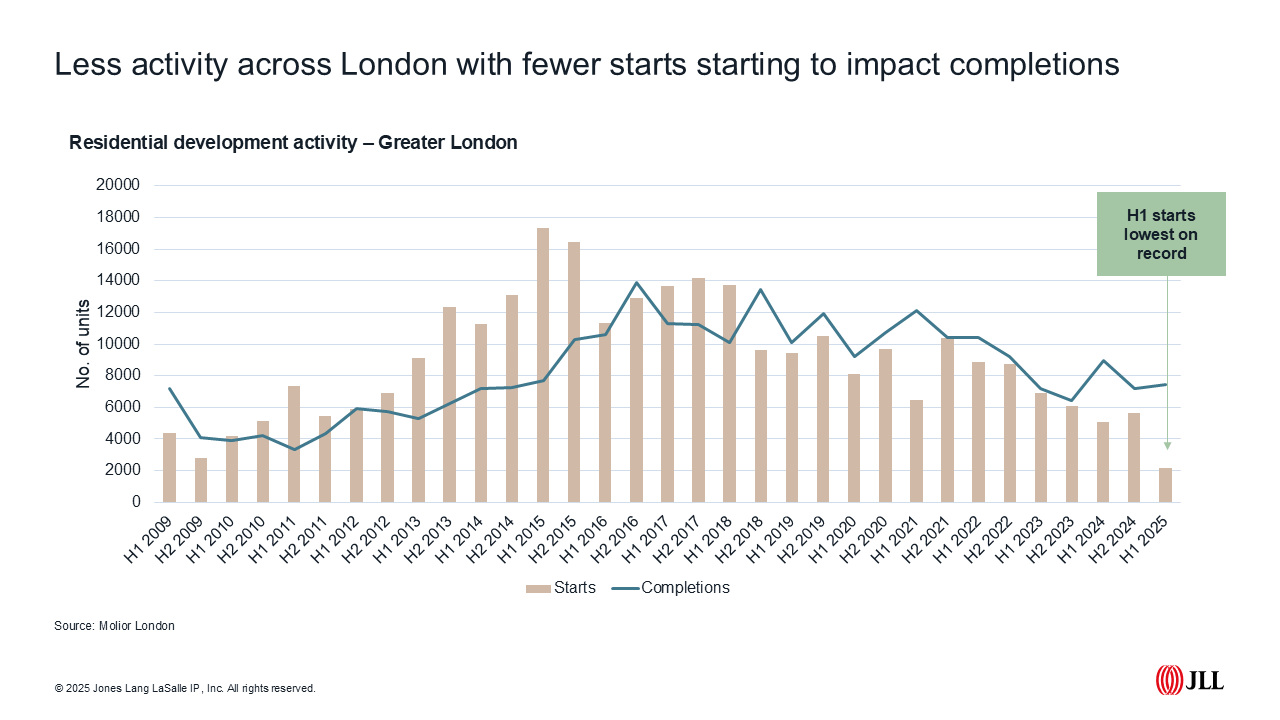

Figures from Molior London show there were fewer than 2,200 private homes started across London in H1 2025, the equivalent of fewer than 5% of the 44,000 private homes target. In the second quarter of 2025, 23 London Boroughs saw no schemes of 20 or more private homes start.

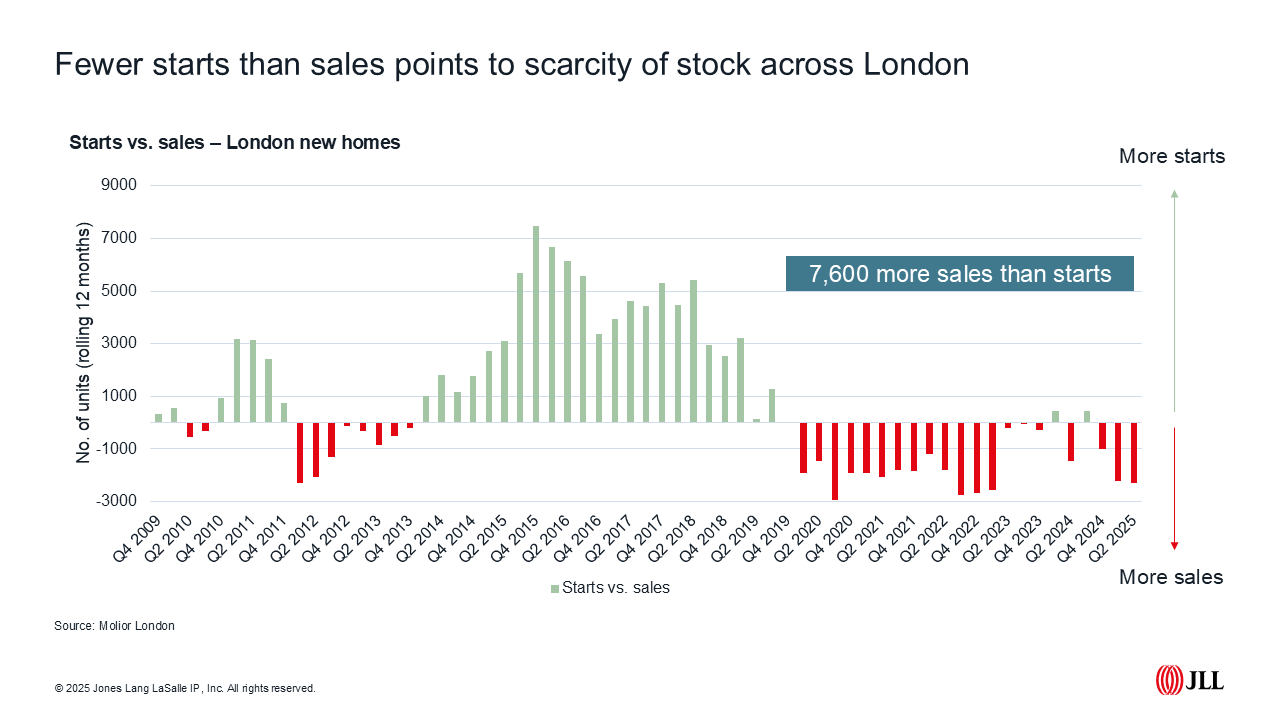

But 2025 figures follow recent trends, with activity across London dropping back since the peak in 2015. Analysis of new homes sales shows that there have been 7,500 more sales than starts in the last five years, with the number of homes under construction across Greater London falling by a third in the last five years. This will have implication for future completions, with Molior London expecting fewer than 10,000 private homes will complete in 2027 and 2028 combined.

JLL Research

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.