News that the first Universal theme park in Europe would be built in Bedfordshire was not the biggest roller coaster announcement this week. That accolade was reserved for Trump's tariffs. At the time of writing (an important caveat right now), the US has announced a 90-day 'pause' on implementing variable tariffs on all countries bar China. This doesn't mean the rest of the world is off the hook this quarter. Blanket tariffs of 10 per cent remain, alongside a higher rate for steel, aluminium and cars of 25%. But America's tone has shifted to one of negotiation, with delegations from across the globe encouraged to come to the table to discuss plans.

The negative reaction to the tariffs rippled through the money markets. Trillions of dollars were wiped off the value of global stocks, but news of a pause saw the markets breathe a sigh of relief, with single-day gains of 9.5 per cent for the S&P 500 and 12 per cent for the tech-heavy Nasdaq, although worth noting still not back to their pre-'Liberation Day' highs. Similar rebounds occurred across the Asian markets, and closer to home, the FTSE 100 rose 6 per cent, but remains 5 per cent lower than on 1 April.

The pausing of variable tariffs arguably has less of a direct impact on the UK, as in essence we are in the same position here as we were before 9 April. The UK's more passive approach over the last week should curry favour with the White House, with much pinned on the potential for further negotiations in the coming days and weeks. But arguably some of the UK's 'advantage' in being a lower tariff trading partner could be watered down; we'll need to see how negotiations pan out.

What does this all mean for the UK economy and housing market?

There was better news on the state of the UK economy in February, with monthly GDP growth of 0.5 per cent, up from 0 per cent in January. But economically February seems a long time ago, with the wider impact of tariffs, employer NI and increases in utility bills and council tax all likely to impact GDP figures in the coming months.

US tariffs, whatever numbers are eventually settled on, are likely to have a negative impact on growth for economies outside the US – and possibly for the US too. Inflation rates outside the US could drop back as exports become more expensive and goods previously destined for the US find their way to more tariff-friendly shores. Whatever happens, the £9.9bn headroom from the Spring Statement looks set to be challenged, meaning further tweaks to taxation could be on the cards at the next fiscal event in the autumn. But as the last seven days have proven, a week is a long time in politics (and economics), so we'll need to wait and see what the ramifications are for the UK in the longer term.

Mortgage rates drop

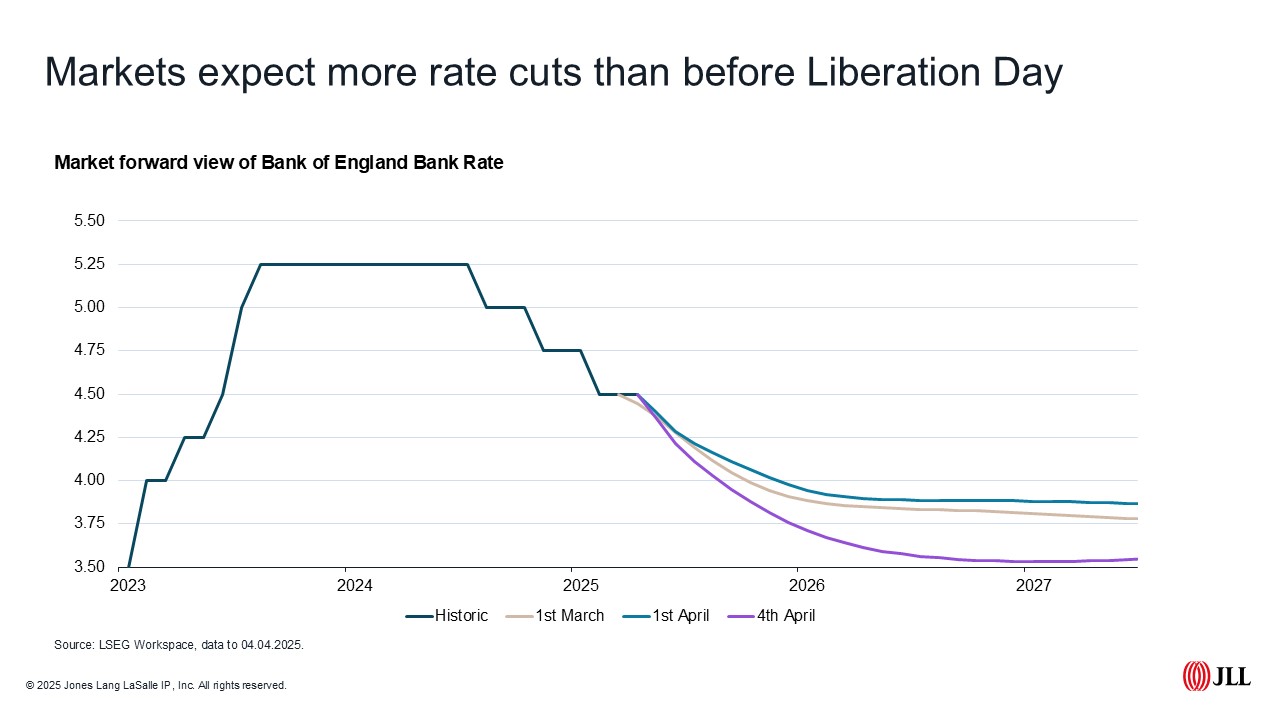

Tariff-induced uncertainty has impacted bond yields and the interbank lending rate, with two-year swaps at their lowest level since Liz Truss was in No.10. This means forecasters now expect the Monetary Policy Committee could reduce the bank rate up to four times this year, up from a consensus forecast of just two rate cuts back in March.

Mortgage lenders have reacted, with Barclays, TSB, and Coventry Building Society amongst others cutting rates by more than 25 bps, with best-buy two and five-year fixed rates now available at sub 4%. This could prove positive for the UK government too, with lower debt servicing costs if rates fall more quickly than anticipated.

Housing market

In the short term at least, it is likely that the 1 April Stamp Duty deadline will have contributed more to the Q2 outlook for the housing market than tariffs. Figures from the Nationwide suggest house prices were 3.9 per cent higher in March than they were a year earlier, with growth flat compared with February. Halifax were a little more downbeat, with prices down 0.5 per cent month-on-month and up 2.8 per cent annually.

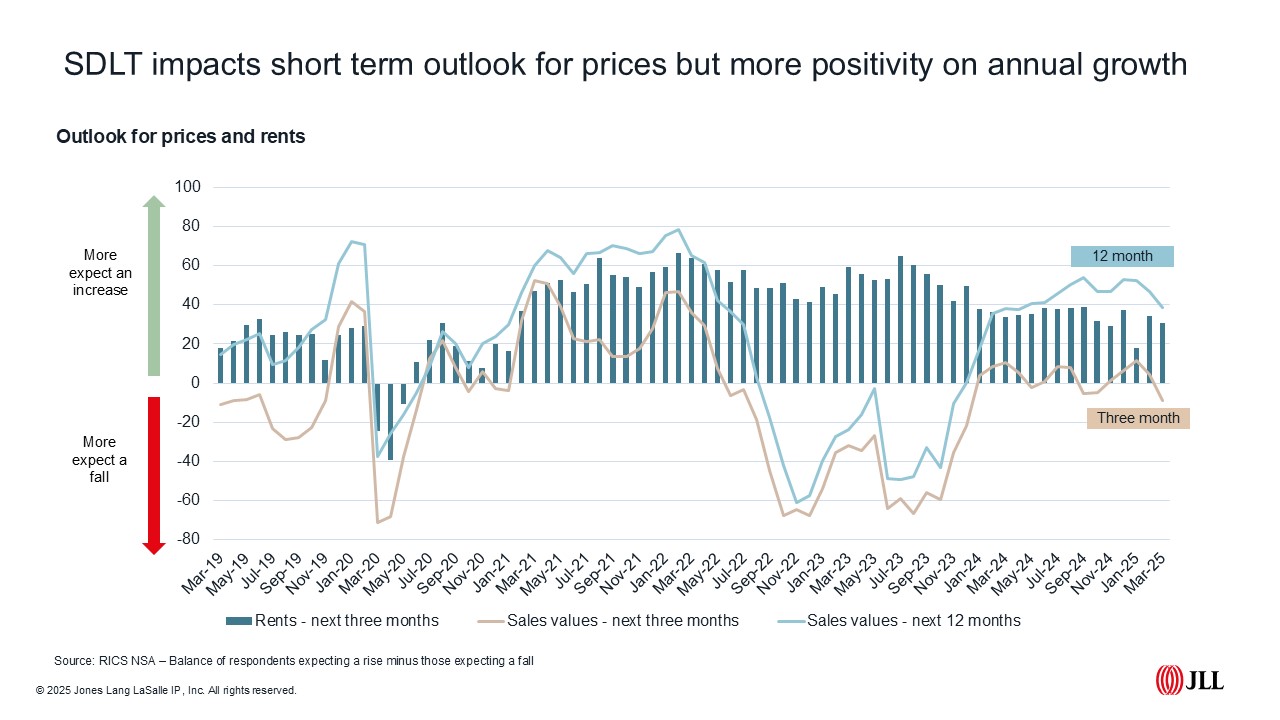

The latest survey from the RICS released this week remained gloomy. New buyer demand dropped back in March, with a net balance of -32 per cent of respondents reporting a drop in new buyer demand, down from -16 per cent the previous month.

As is often the case following an increase in Stamp Duty costs, expectations on activity in the short term remain subdued, with more respondents (a net balance of -18 per cent) expecting fewer agreed sales in Q2.

More agents reported an increase in stock reaching the market, but this had also dropped back, with a net balance of +6 per cent in March compared with an average of +17 per cent average over the last six months. This is all impacting the short-term outlook for prices, with a higher proportion of agents expecting prices will fall over the next three months. But looking at the next 12 months, some positivity remains, with +39 per cent of respondents expecting prices would be higher in 12 months' time.

Rental market

The outlook was more positive for the rental market. Tenant demand is increasing as we move into the Spring, with the March RICS survey reporting a net balance of +20 per cent of agents who had seen tenant demand rise in Q1, with expectations on rental increases also remaining in positive territory at a net balance of +31 per cent. Stock levels remain constrained, with a net balance of 24 per cent of agents reporting a drop in new landlord instructions. Homelet data shows average UK rents for new lets rose to £1,288 per month in March, up 1 per cent on February. Average rents on new lets were 2.0 per cent higher in London and 3.5 per cent higher in the rest of the UK on an annual basis.

JLL Research

JLL is a leading global professional services firm specialising in real estate and investment management, with $16.6bn annual revenue in 2020, operations in over 80 countries and a global workforce of over 90,000. With over 7,000 employees and 15 offices in the UK, we support our investor, developer, and occupier clients at every stage of the property lifecycle across both commercial and residential asset classes. This includes land purchase, access to capital, planning, development advisory, leasing, building management and sales.

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.

Disclaimer: © 2025 Jones Lang LaSalle IP, Inc. All rights reserved. Data within this report is based on material/sources that are deemed to be reliable and has not been independently verified by JLL. JLL makes no representations or warranties as to the accuracy, completeness or suitability of the whole or any part of the report which has been produced solely as a general guide and does not constitute advice. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. JLL, its officers, employees shall not be liable for any loss, liability, damage or expense arising directly or indirectly from any use or disclosure of or reliance on such report. JLL reserves the right to pursue criminal and civil action for any unauthorized use, distribution or breach of such intellectual property.