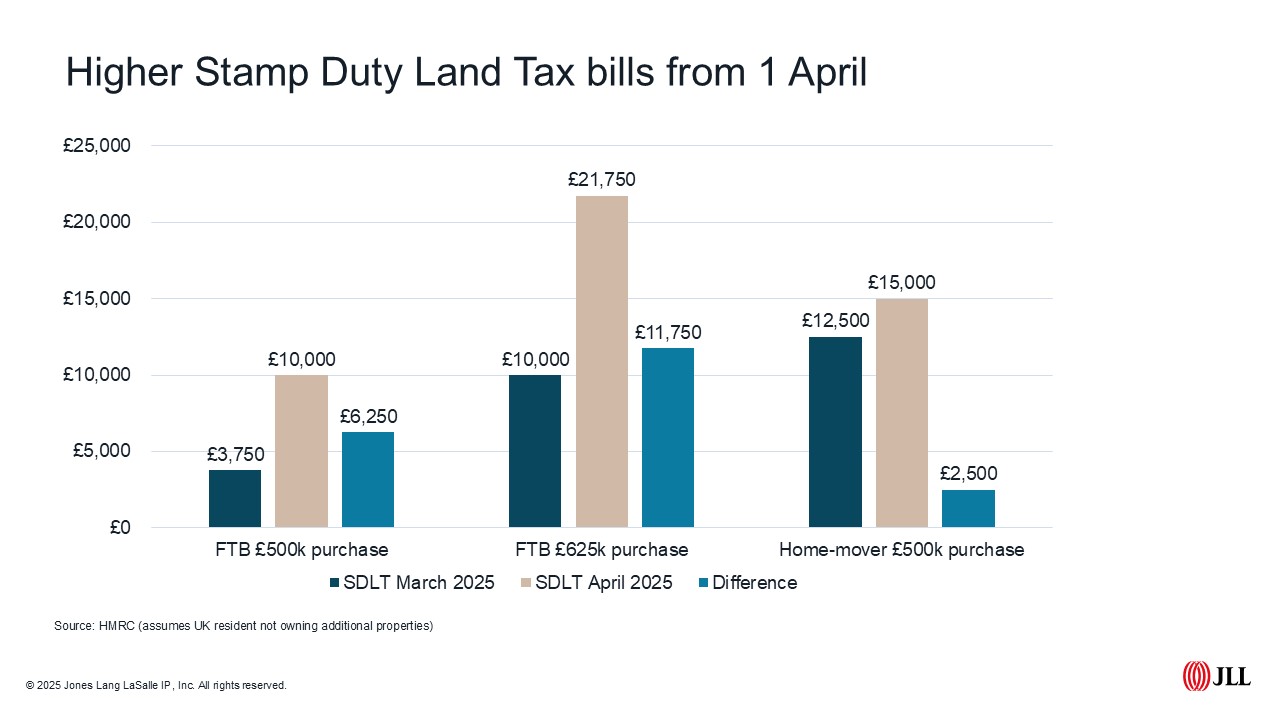

The clock is ticking for those looking to take advantage of stamp duty savings before rates revert to previous levels on 1 April. First-time buyers have the biggest incentive, particularly those purchasing more expensive homes. The threshold at which first-time buyers no longer benefit from relief drops from £625,000 to £500,000, with the nil rate dropping from £425,000 to £300,000. This means someone purchasing a £500,000 first home would see their stamp duty bill increase from £3,750 in March to £10,000 in April.

Transactions

The SDLT rush is evident in transactions figures, with just over 95,000 homes changing hands in January across the UK, 14% higher than the same month a year earlier. This is the highest January figure since 2022 and marginally up on the 10-year January average.

House prices

The impact on house prices is less clear cut. Figures from the Nationwide index show house prices rose 3.9% in the year to February 2025, up 0.4 percentage points month-on-month. The Halifax index shows a marginal slowing in February, with prices down 0.1% monthly and up 2.9% annually. But we could see the rate of growth fall a little in March. More first-time buyers, who are generally purchasing smaller (and often less expensive) homes, means we could see the overall average fall in March and potentially rise in April – as a result it remains prudent to not place too much emphasis on monthly fluctuations in prices this spring.

Mortgage approvals

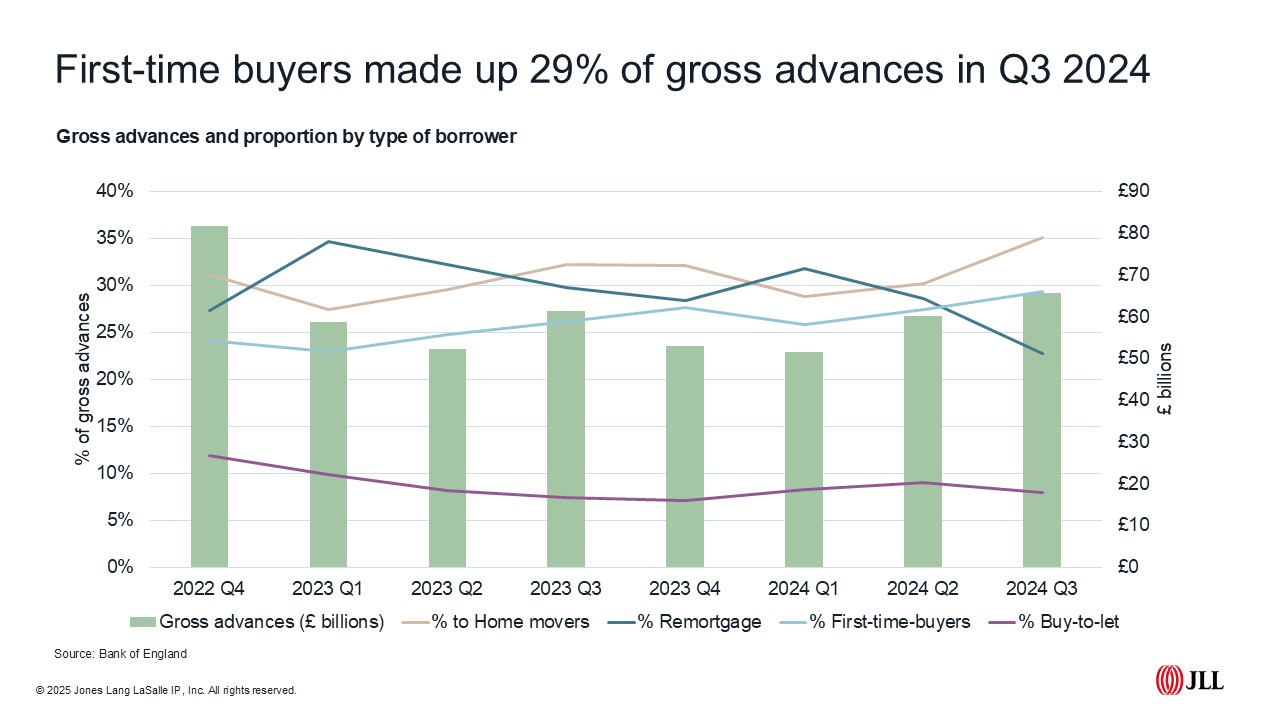

The pre-SDLT rush was evident earlier in the mortgage stats, with the time taken to complete a sale meaning those wanting to beat the deadline would need to have been well progressed by early 2025. In late 2024 we saw annual increases in net mortgage lending almost 50% higher than they were a year earlier. True, 2023 wasn’t a busy year, but the acceleration in activity was particularly evident in Q4. Lower rates helped, but first-time buyers were busy with their brokers too. The latest numbers from the Bank of England show mortgage approvals rose 19% annually in January 2025, with UK Finance showing a 16.4% annual increase in loans to first-time buyers in Q3 2024.

The death of leasehold?

Commonhold isn’t new; it was introduced back in 2004 as part of the Commonhold and Leasehold Reform Act 2002, but most new developments completed since continued to adopt a leasehold ownership structure. This looks set to change, with the Government publishing a White Paper proposing replacing leasehold with commonhold for new flatted developments (the sale of new leasehold houses has already been stopped). A consultation on how this could be introduced is set to take place in the coming months. Under a commonhold ownership structure, homeowners would effectively own the freehold of their individual unit, with the freehold of the building held by the building’s commonhold association. Each owner would be a member of their building’s commonhold association and would be expected to contribute to overall maintenance and running costs, similar to a leasehold service charge. No ground rent would be payable. Plans are afoot, too, to make it simpler for existing owners of leasehold properties to convert to commonhold, although this is a more challenging prospect than imposing the new structure on new build homes.

Big Six

The latest data from Zoopla shows annual rental growth fell from 3.9% in Q4 2024 to 3.0% in their latest Q1 release. The lowest level for more than three years, it follows a significant increase in rents over that period. This ‘normalisation’ in the rental market has been evident for some time. Stock levels per agent have risen from recent lows but are still down on pre-pandemic norms. There are still 12 enquiries for every rental home according to Zoopla, with the number of homes to rent per agent averaging 13 in February 2025, up from a low of 10 in 2023, but still below the longer run average of 16 between 2017 and 2021.

Our recently released JLL Big Six Residential Development Report shows a similar trend. The report tracks changes in prices and rents across mainstream and prime developments in six cities outside London: Birmingham, Bristol, Edinburgh, Glasgow, Leeds and Manchester.

Average annual rental growth across the Big Six stands at 4.2%. New stock coming to the market continues to demand higher rents, however more balance between supply and demand has meant average growth returning to single digits in all six cities.

Interest rates have remained higher than expected and continue to impact development viability and buyers’ budgets through higher mortgage rates. Average prices for new build apartments have risen 2.1% across the Big Six. Markets with lower average prices, notably Birmingham and Glasgow, have seen the highest price growth.

After a sharp slowdown in the first half of 2024, the Big Six build-to-rent market had its most active second half since 2021, bringing full-year investment to £1bn. Though reflecting a 12% year-on-year decline, it was a strong finish to 2024.

To read the latest JLL Big Six report click here.

Build-to-rent and UK living

It is not just the Big Six where build-to-rent activity rose at the back end of 2024. With £5.4bn invested nationally in 2024, BTR activity was up 9% on 2023. Across all sectors of UK living investment rose 5% year-on-year to £13.9bn. There were more than 230 deals completed in 2024, 16% above the five-year average.

An uncertain outlook for build and debt costs contributed to drop in forward funding deals, falling 26% below the five-year average, the lowest level since 2018. At the same time, forward purchases and investments in standing stock rose 31%. Domestic investors led the pack, with 44% of total living investment originated in the UK.

To read more on our outlook for UK living in 2025 click here.