Halifax figures are also showing a 2.4 per cent annual rise in July. Mortgage approvals are rising too, with more than 64,000 mortgages approved in June, activity returning to pre-pandemic norms (when rates were significantly lower than they are now).

Housing market

The number of homes sold in June rose 13 per cent on May, with the impact of the 1 April Stamp Duty changes now dissipating. H1 figures show an 18 per cent annual increase in sales nationally, with June sales up 5 per cent year on year.

Affordability is improving, at least on paper, with the average house price to income ratio hitting a ratio of 5.75 - a ten-year low. This is down from a high of 6.9 in 2022. Although elevated mortgage rates mean affordability remains more challenging for those looking to get onto the ladder.

But sellers are having to be more realistic on price. Latest figures from Rightmove show average asking prices dropped by 1.2 per cent in July, equating to an average £4,500 reduction. A reduction in July isn’t unusual but the scale of the reduction is, with Rightmove reporting the highest July fall in more than twenty years of data. London saw the highest monthly fall, with asking prices 1.5 per cent lower in July than June. This is driven by central London and follows a similar trend to that observed in our latest PCL report.

News from the MPC

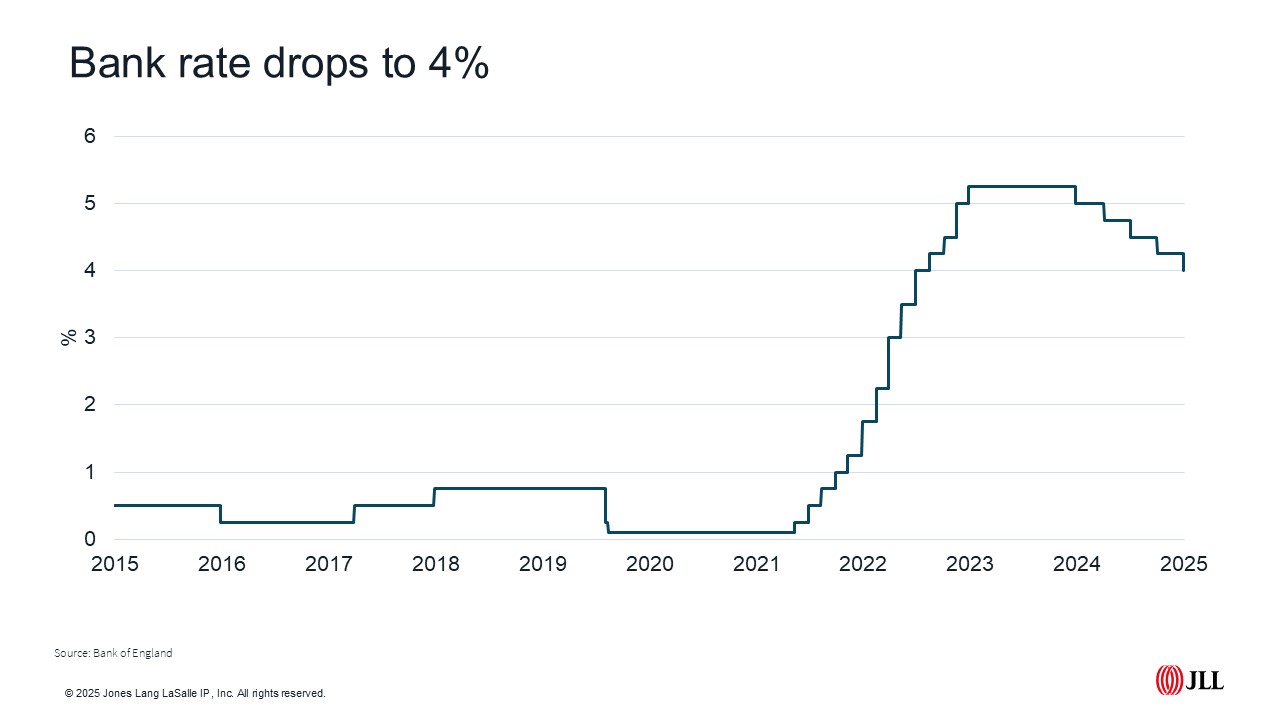

The big news of the week was always going to be the Bank Rate. While there were some wobbles, the long-term expectation had always been that August would see a 25bps fall, with the Monetary Policy Committee confirming a lowering of rates to 4 per cent on 7 August.

While the result wasn’t really a surprise, there were more hawks than expected this time round, with members of the Monetary Policy Committee only narrowly voting through the 25bps cut through by five votes to four. The remaining four all felt rates should remain at 4.25 per cent (with one of the rate cutters initially voting for a 50bps reduction).

This latest cut is unlikely to be a game changer for mortgage rates, with the August fall all but factored in. That said, effective interest rates on newly drawn mortgages fell for the fourth consecutive month in June, down to 4.34 per cent. Lifetime Capital is quoting best-buy rates at sub-3.8 per cent for those borrowers viewed upon most favourably by lenders.

Consensus forecasts expect one further 25bps cut in 2025 and another in H1 2026, taking us to a 3.5 per cent rate by mid-year 2026.

Bricks versus concrete

Those in government and those of us in the housebuilding sector will be hoping some of the positivity around lower rates feeds through into the new homes market this autumn.

In our last Roundup we discussed the latest Molior figures for London, with delays and additional financial pressures associated with ‘high risk’ buildings and the arduous Gateway process culminating in a drop off in flatted urban development.

But the challenge isn’t just a London one, or indeed just residential. The latest S&P Purchasing Managers Index (PMI) shows a slowdown in activity across their three monitored construction sectors, civil engineering, commercial and residential. Respondents cited a lack of tender opportunities and a hesitancy from customers to commit to projects.

Supply chain figures from the Mineral Products Association (MPA) echo the drop off in delivery. Sales of ready-mixed concrete fell 11.5 per cent in Q2 2025 compared with Q1, are down by a third in the last ten years and are at their lowest, lockdown aside, for 63 years.

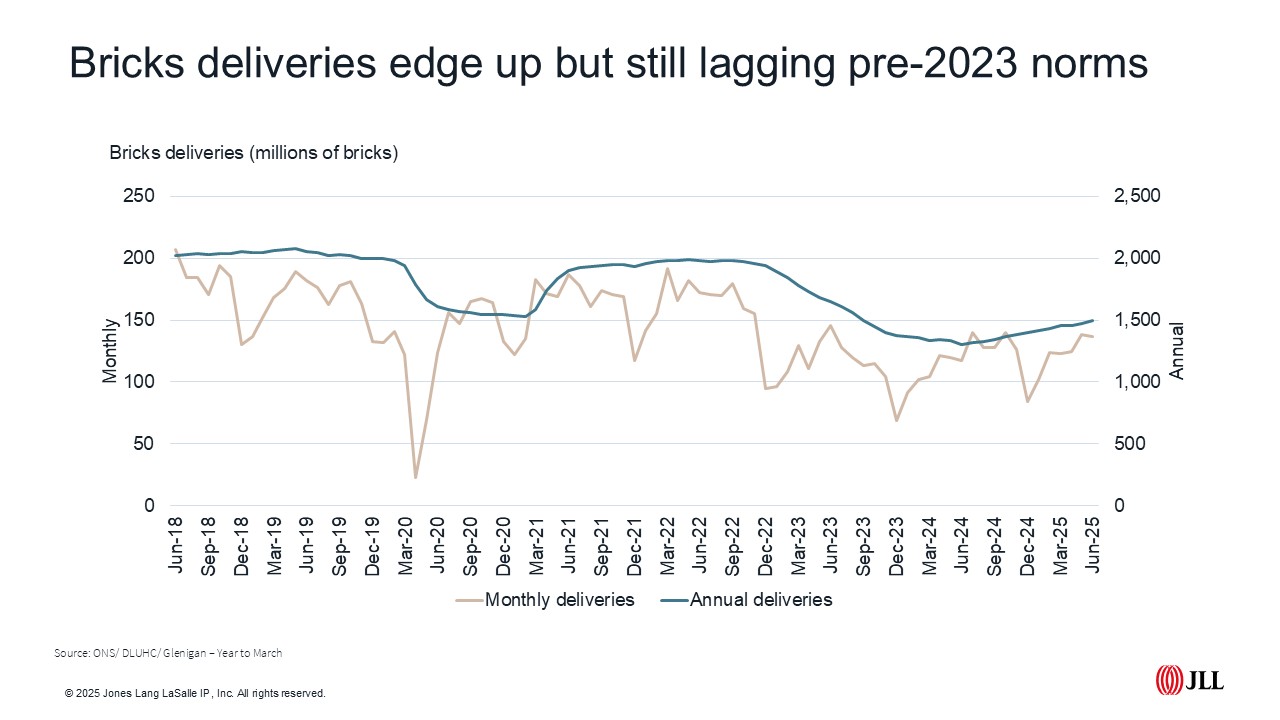

Brick deliveries are showing more of a mixed picture. Seasonally adjusted monthly data shows 5 per cent fewer bricks delivered in June than May, but activity was up 16 per cent annually, marginally up on the +15 per cent recorded in May. Deliveries are on an upward trajectory, with annual figures the highest for two-years, but we’ve still got some way to go to get back to pre-pandemic norms.

JLL Research