Angela Rayner has committed another £350 million to address the shortfall of affordable homes. £300m has been signed off to boost the Affordable Homes Programme with a further £50m for the Local Authority Housing Fund. Every little helps for those looking to deliver affordable housing, but the scale of the problem and the years of shortfall in delivery means that further funding will be needed on top.

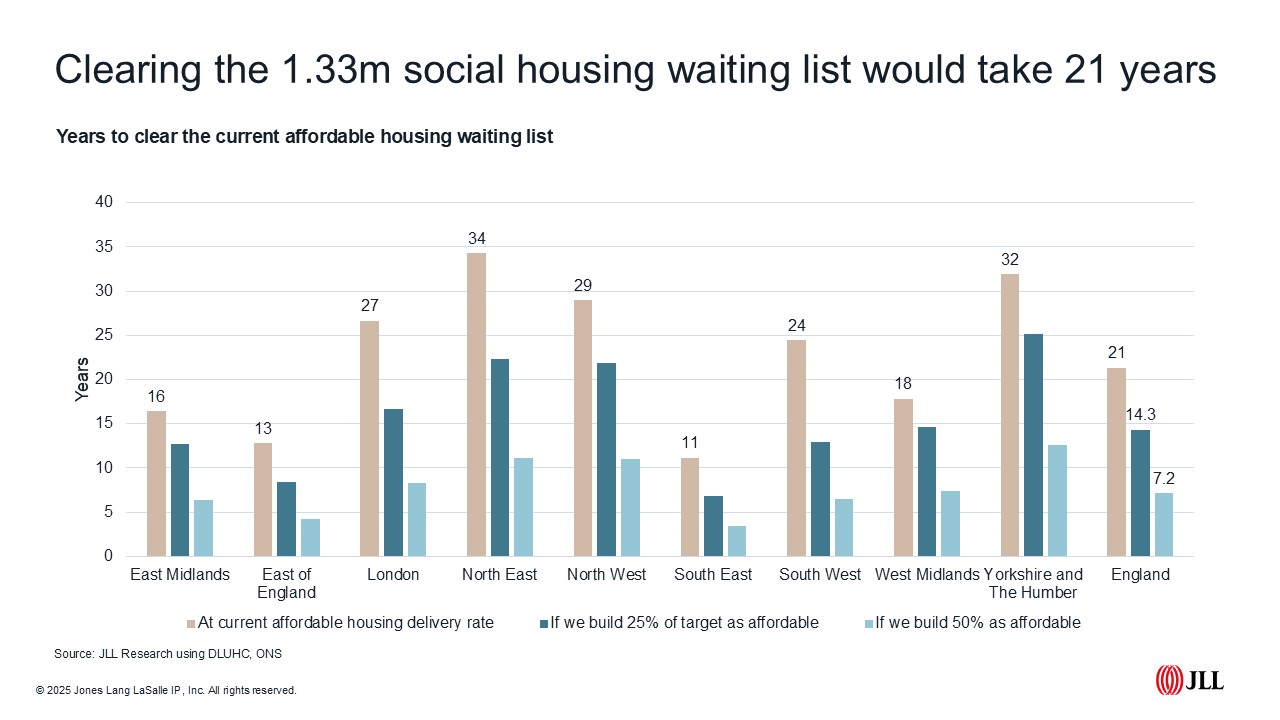

The £300m injection is forecast to deliver 2,800 homes (equating to roughly £107,000 per home), but recent analysis of the housing waiting list shows the number of households on the list topped 1.33 million at last count (March 2024), up 43,000 in 12 months. Meaning that to build the 43,000 homes required just to keep the list at 2023 levels would have required £4.6 billion in funding at £107,000 a home. If we look to tackle the 1.33 million households on the waiting list it would take 21 years at current affordable housing delivery rates to build enough homes, before we even consider new entrants over that period.

Fiscal headroom disappearing

The outlook for the UK economy has become more challenging in the last few weeks. The Bank of England cut the base rate (hurrah!) but were pessimistic about the UK’s growth prospects. Their expectations for GDP growth in 2025 cut from 1.5% to 0.75%. Of course, the Bank are not the only forecasters, with the latest consensus forecasts remaining north of 1%, but we expect to see a more tempered short-term outlook emerge in the coming weeks.

The Office for Budget Responsibility will deliver their next forecast to parliament on 26 March. The combined effect of weaker economic growth and higher borrowing costs expected to have significantly reduced Rachel Reeves’ £10bn of fiscal headroom.

But fears of a recession in the second half of 2024 have been allayed by news that UK GDP grew by 0.4% in December, up from 0.1% in November. This means estimates for Q4 2024 have tipped (marginally) into positive territory at 0.1% growth, higher than the 0.1% contraction forecasters were expecting in a recent poll by Bloomberg. Annually GDP is estimated to be 1.5% higher in December 2024 than it was a year earlier, with full year estimates lower at 0.8% year-on-year.

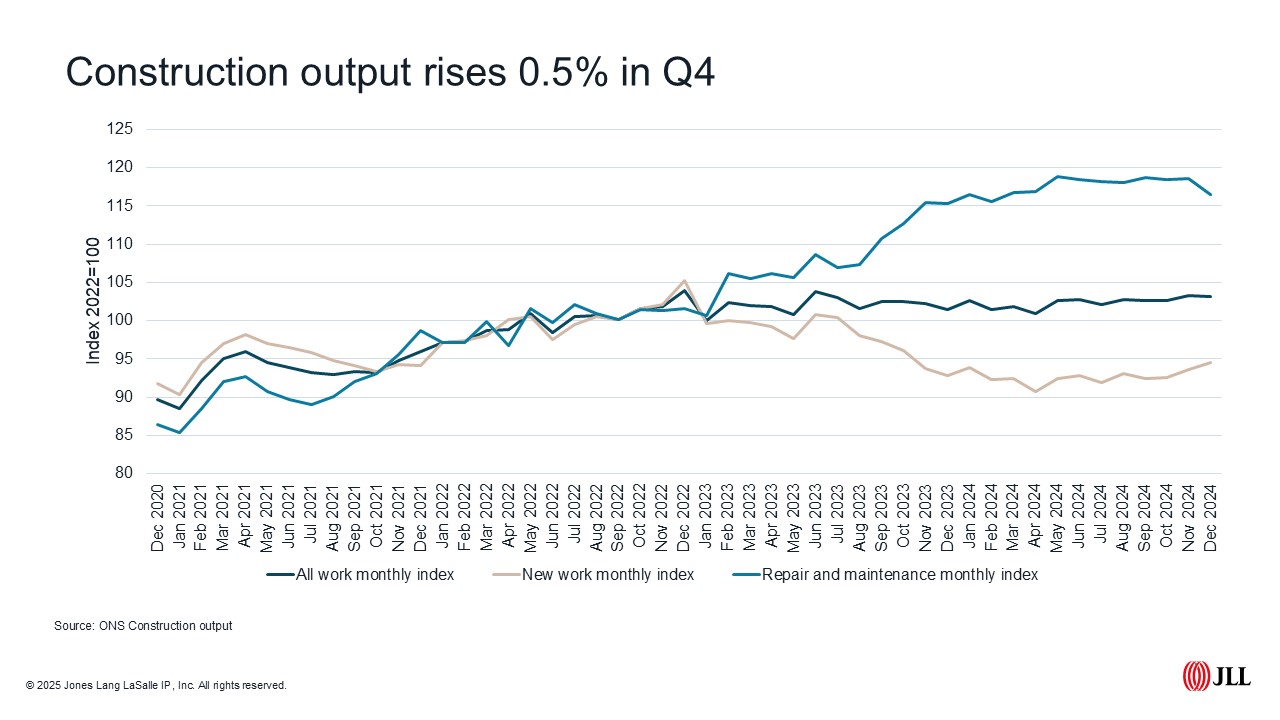

Increased construction activity contributed to the latest growth figures. Government estimates suggest construction output rose 0.5% in the three months to December 2024 compared with the three months to September. The rise in activity was led by new work, which increased by 1.2%, with repairs and maintenance activity falling marginally by 0.4%. Private new housing was one of the main drivers in the growth in new work, rising 1.3%. Positive news for the sector but still 20% lower than the post-pandemic peak in September 2022.

The return of the sub 4% fix

Both Santander and Barclays have announced new 3.99% fixed rates deals, signalling the return of the sub-4% mortgage which has been absent from the market for a few months now (although with a hefty fee and low loan-to-value). It’s hoped that breaching the psychological sub 4% barrier will bring more home movers, who had become accustomed to record low rates, back to the market.

Fewer home movers have meant the proportion of first-time buyers in the market has risen significantly. UK Finance figures crunched by Halifax show there were more than 340,000 first-time purchases in 2024, up 19% on 2023. First-time buyers accounted for more than half (54%) of mortgaged purchases last year, a record high since the data was first collected back in 2014.

Latest from the RICS

The proliferation of lower rates will be good news for activity in the housing market, but in their absence the latest RICS Survey shows a tentative start to the year in January. Activity in the sales market remained broadly flat last month, with the same number of respondents reporting new buyer enquiries rising than falling in January. Here at JLL we’re in the (marginally) more positive camp, with data from our offices showing a modest uptick in new applicants registering so far this year, up 6% on the same period in 2024.

Sellers continue to return to the market, with more respondents (a balance of +25%) reporting an increase in new instructions, higher than the +16% recorded in December. Stock per surveyor rose too, reaching 45 homes in January, up from 41 at the same point a year ago.

For lettings, tenant demand remained broadly flat, with the balance of opinion at +2% in January, meaning marginally more respondents reported a rise than a fall. Fewer landlord instructions were reported again in January (net balance of -19%), with March 2022 being the last month when we saw a positive net balance recorded. Lack of stock, through fewer landlord instructions, is still expected to underpin further rental growth this year.

New Towns

Housing Minister Matthew Pennycook has announced that more than 100 potential sites across England have been submitted to the New Towns Taskforce for consideration. The sites, the majority of which are urban extensions, aim to provide more than 10,000 homes each with the government promising spades in the ground before the end of this parliament. Initial reports suggest the government could green light around 12 schemes, or more than 120,000 homes. But few, if any, of these homes will be delivered within this parliament, meaning their (self-imposed) challenge of building 1.5 million homes remains.