It’s been quite a week (again) in Westminster, with further revelations about the former U.S. Ambassador looking at points as if they could topple Starmer. Yields on ten-year government debt rose to just shy of 4.6 per cent in response but have since settled, with the pound weakening against both the dollar and euro, too.

But despite calls from Scottish Labour leader Anas Sarwar for the PM to stand down, the cabinet came out broadly in support. For Sarwar, the upcoming Holyrood election will be at the forefront of his mind, but for Starmer, too, the 7 May local elections remain a thorn in Labour’s side, with the potential for ‘protest’ voting to further destabilise Starmer and Labour’s front benches.

UK economy

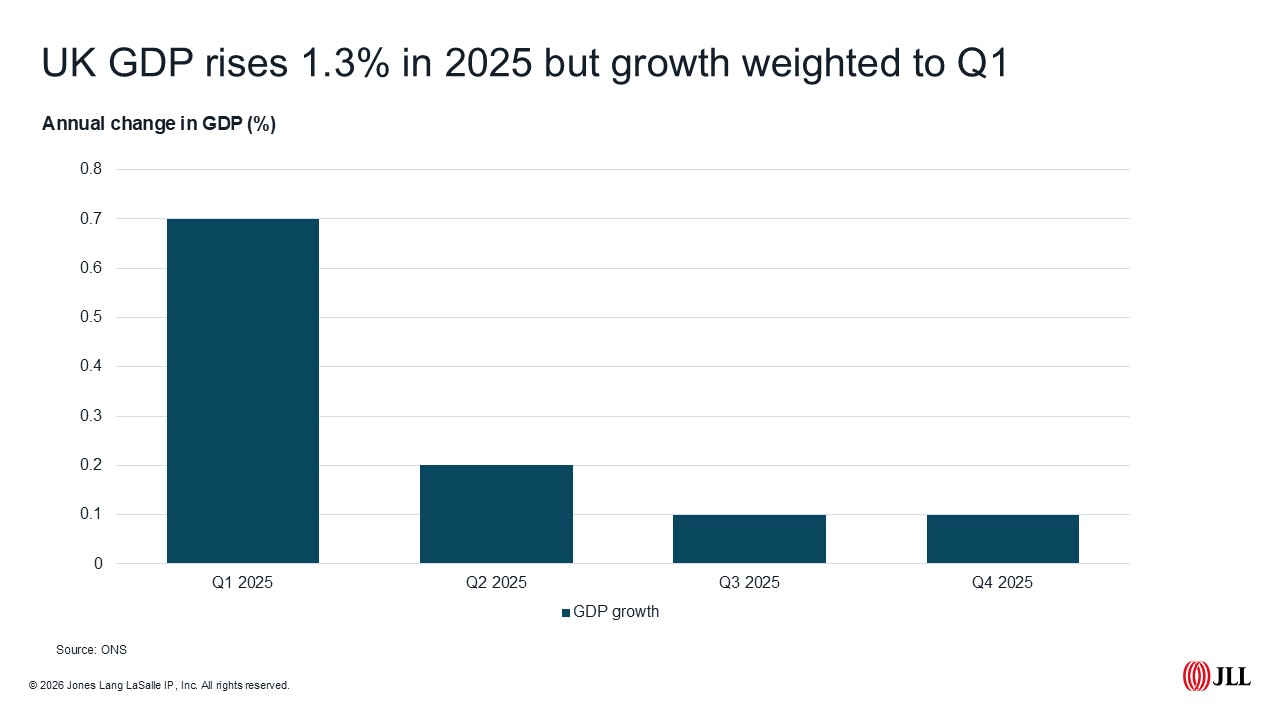

Like front line politics, unpicking what’s happening to the UK economy remains challenging. Following a surprise 0.3 per cent uptick in GDP in the three months to November, the December (Q4) figures came in at a somewhat underwhelming 0.1 per cent, the same as recorded in Q3. This took full-year 2025 growth to 1.3 per cent, notably above the figure most forecasters predicted earlier in the year.

The announcement of these results resulted in some significant political cherry-picking, with Labour citing the UK as the best-performing European G7 nation (effectively we did better than France, Germany and Italy). The Conservatives took a different stance, with the flatlining of GDP in the second half of the year blamed squarely at Rachel Reeves’ decision making.

Looking ahead, the OBR expects growth of 0.9 per cent in 2026, whereas consensus forecasts are a little higher at 1.0 per cent.

Caution around the labour market

The labour market has continued its gradual cooling from the post-pandemic tightness that characterised recent years. The unemployment rate remained at 5.1 per cent in the three months to November—October, the highest level since 2016 when excluding the pandemic disruption. But there are now 3.7 million more people in employment than when unemployment last reached this level. Job vacancies remained stable in November at 2.3 per 100 employee jobs for the fourth consecutive month, sitting modestly below the pre-pandemic average of 2.6.

The inflation picture presents a much brighter outlook than we've seen over the past two years, despite some uneven progress. Core inflationary pressures, particularly in goods, continue to subside, and slower wage growth is expected to gradually filter through to services inflation.

Most forecasters anticipate inflation will continue its downward trajectory throughout 2026, drawing closer to the Bank of England's 2 per cent target. Financial markets expect this will permit further gradual monetary easing as we move through 2026. The Bank of England maintained its policy rate at 3.75 per cent at its most recent meeting but signalled the possibility of additional cuts. Markets and economists are forecasting up to two further 25 basis point reductions in the year ahead.

UK investment

JLL data on UK real estate investment volumes (all sectors), shows volumes increased 64 per cent quarter on quarter to £16.4bn in Q4, from £10.0bn in Q3. This represented a 28 per cent increase on 2024 where volumes reached £12.8bn in Q4. Growth also remained higher than the long-run average, at 10 per cent above the 10-year Q4 average.

A strong Q4 means total 2025 volumes rose to £49.0bn, 27 per cent above 2024 volumes of £38.7bn and 2 per cent above the 10-year average.

Affordability at a decade high

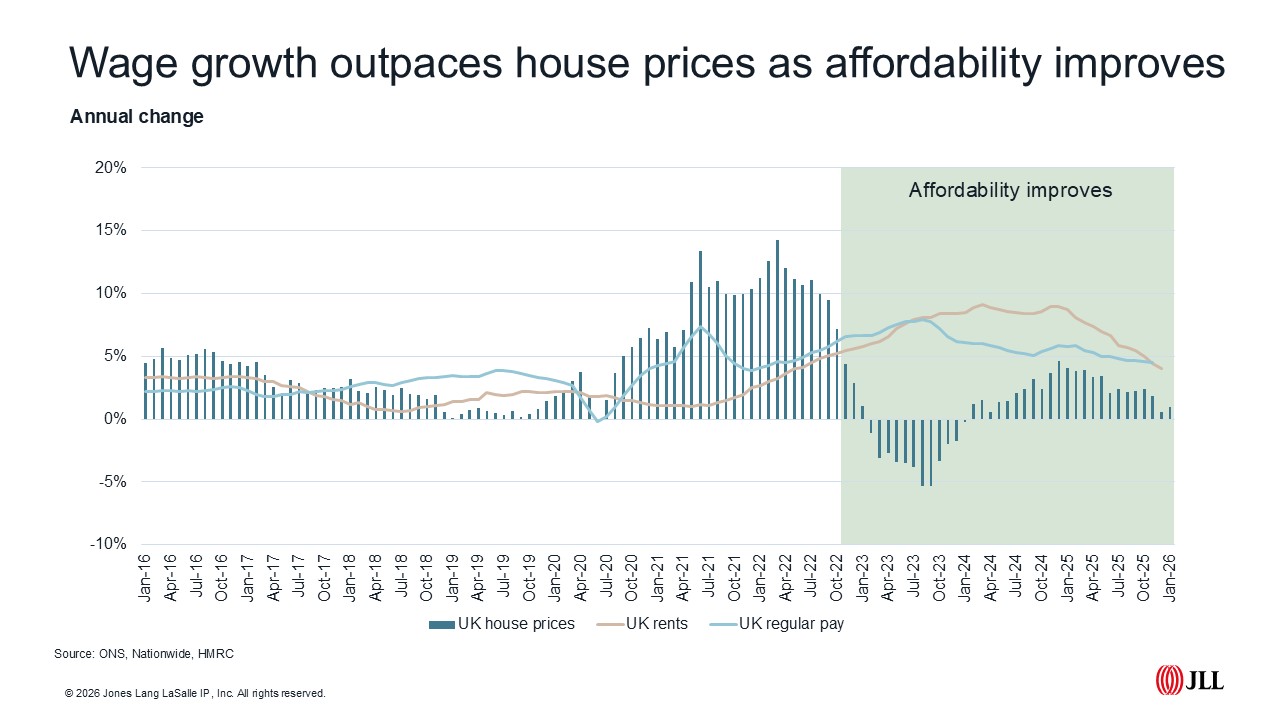

UK wage growth dropped to its lowest level since 2022 in the three months to November, rising 4.5 per cent year-on-year. Yet despite the recent drop in the rate of wage inflation, increases in earnings have been outpacing house prices for some time now. This has resulted in house price to earnings ratio dropping from a high of 6.9 times earnings in Q2 2022 to 5.6 times in Q4 2025. This means house prices, when measured as a multiple of earnings are at their most affordable for over a decade.

London has followed a similar trajectory. Back in 2016 average London house price hit 11.7 times earnings but almost a decade on the ratio had fallen to 8.8. The last time London had a similar ratio was back in Q4 2013.

The challenge more recently has been around mortgage costs, with higher rates effectively wiping out affordability advantages. But rates are improving, best-buys are under 3.6 per cent and the effective interest rate on new mortgages edged down to 4.15 per cent in December from 4.20 per cent in the previous month.

Housing market

Responses to the January RICS survey point to some green shoots in the residential market this year. The 12-month view on house prices rose for the fifth consecutive month, with a net balance of +43 per cent of respondents expecting prices to be higher at the same point in 2027. The outlook for rental growth remains positive too, with a net balance of +28 per cent expecting near-term rental increases.

JLL Research

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.

Disclaimer: © 2025 Jones Lang LaSalle IP, Inc. All rights reserved. Data within this report is based on material/sources that are deemed to be reliable and has not been independently verified by JLL. JLL makes no representations or warranties as to the accuracy, completeness or suitability of the whole or any part of the report which has been produced solely as a general guide and does not constitute advice. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. JLL, its officers, employees shall not be liable for any loss, liability, damage or expense arising directly or indirectly from any use or disclosure of or reliance on such report. JLL reserves the right to pursue criminal and civil action for any unauthorized use, distribution or breach of such intellectual property.