Government announcements have been coming in thick and fast this week. They’ve confirmed the detail behind much-anticipated changes to leasehold ownership, provided clarity on decent homes, minimum energy efficiency standards, warm homes, affordable housing rent convergence and low-cost loans for housing associations. Here at JLL we’ve been busy releasing reports of our own too, with our latest Prime Central London and Living Roundup out now. So, buckle up, take a deep breath, and we’ll run through what we’ve learnt in the last fortnight.

Leasehold reform

The government has finally published the Draft Commonhold and Leasehold Reform Bill. Reactions differ depending on which side of the leasehold fence one sits. Owners of freeholds bought as investments (which include individuals and larger institutions) will be assessing the implications for income. Developers too will be keen for more clarity on the impact of commonhold structures for future development, something which we’ll be looking into more in the coming weeks. But for individuals owning leasehold properties or those looking to buy the reaction remains positive. The proposed capping of annual ground rents at £250 from 2028 (dropping to a peppercorn rent after 40 years) will mean existing homeowners who own properties with more complex ground rent structures (doubling ground rents being one of the most challenging) finding it easier to secure a mortgage or sell their homes. It also reassures prospective owners that costs will not escalate going forward, supporting increased activity in the market. With challenges around escalating service charges, the greater transparency a commonhold structure brings may mean common holders have more control (or at least better oversight) of fees charged too.

Housing delivery – a mixed picture

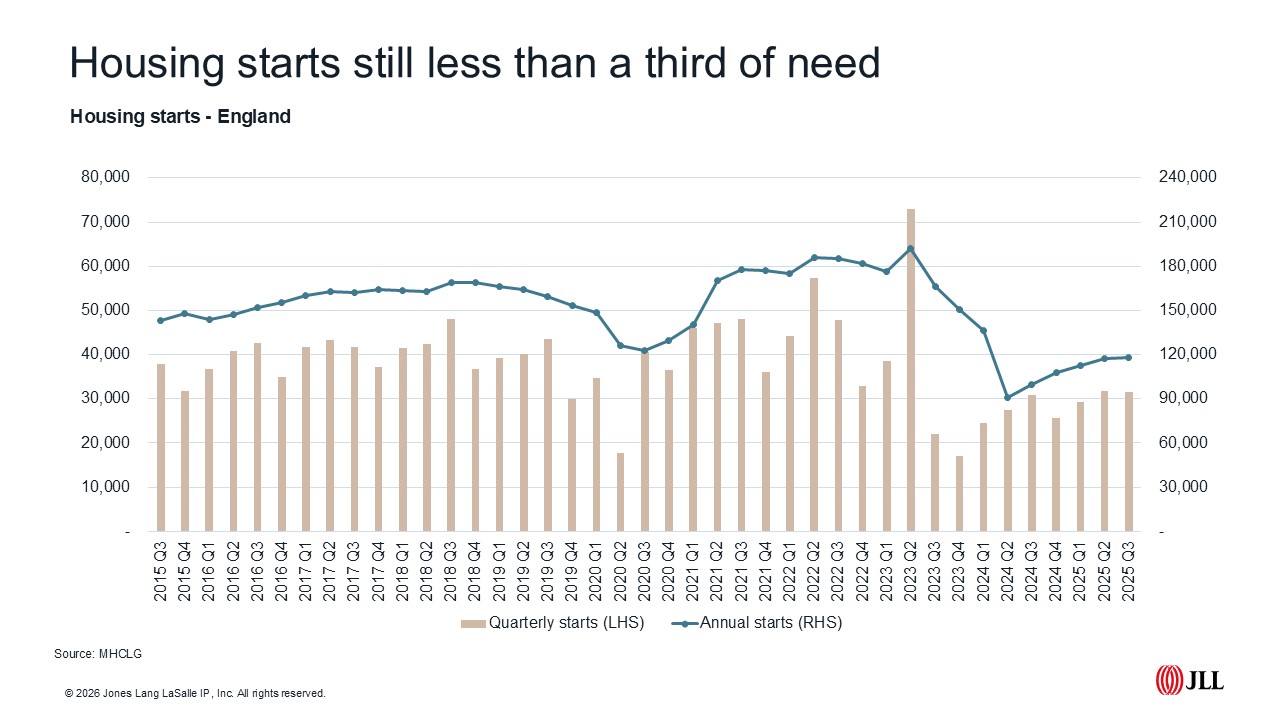

The government’s commitment to 1.5 million homes appears unwavering, however 18 months from coming to power the delivery of new homes has reached near record lows. The government will welcome some positive headlines, with an 18 per cent annual increase in housing starts in the year to September 2025. But this isn’t the full picture. Changes to building regulations meant starts spiked and then dropped back in Q2 2023, meaning the hike in starts comes off an abnormally low base.

In London Molior’s latest release was mixed too. The number of starts totalled just over 5,500 in 2025 - it was 34,000 a decade earlier - meaning Molior’s London starts in 2025 were just 6 per cent of London’s 88,000 housing needs target. But there was a glimmer of hope, with Q4 starts rising, accounting for 41 per cent of the albeit low 2025 total.

Affordable housing clarity

The government has set out the detail behind rent convergence for social housing. The announcements are designed to address the difference in rents charged for some social homes and formula rents for comparable properties. This means more fairness for tenants who won’t pay vastly different rates for similar homes just because they’ve lived in a property for longer or have a different social landlord. From April 2027 affordable housing providers will be able to increase rents by £1 per week over and above CPI plus 1 per cent rising to £2 per week above CPI+1 from April 2028. Rent convergence can run for up to ten years, or until they reach parity. London has the widest gap and is expected to take the longest with some regional markets needing only a year or so to regain lost ground. The announcements on rent convergence are seen as key in underpinning providers’ balance sheets and ensuring they have the confidence and financial ability to deliver more homes.

Details were also shared on the £2.5bn of low-cost loans for housing associations announced at the spending review. The 25-year loans will have an interest rate of 0.1 per cent. £250m will be set aside to support section 106, with the remaining 90 per cent supporting the delivery of social housing through grant-funding.

Living update

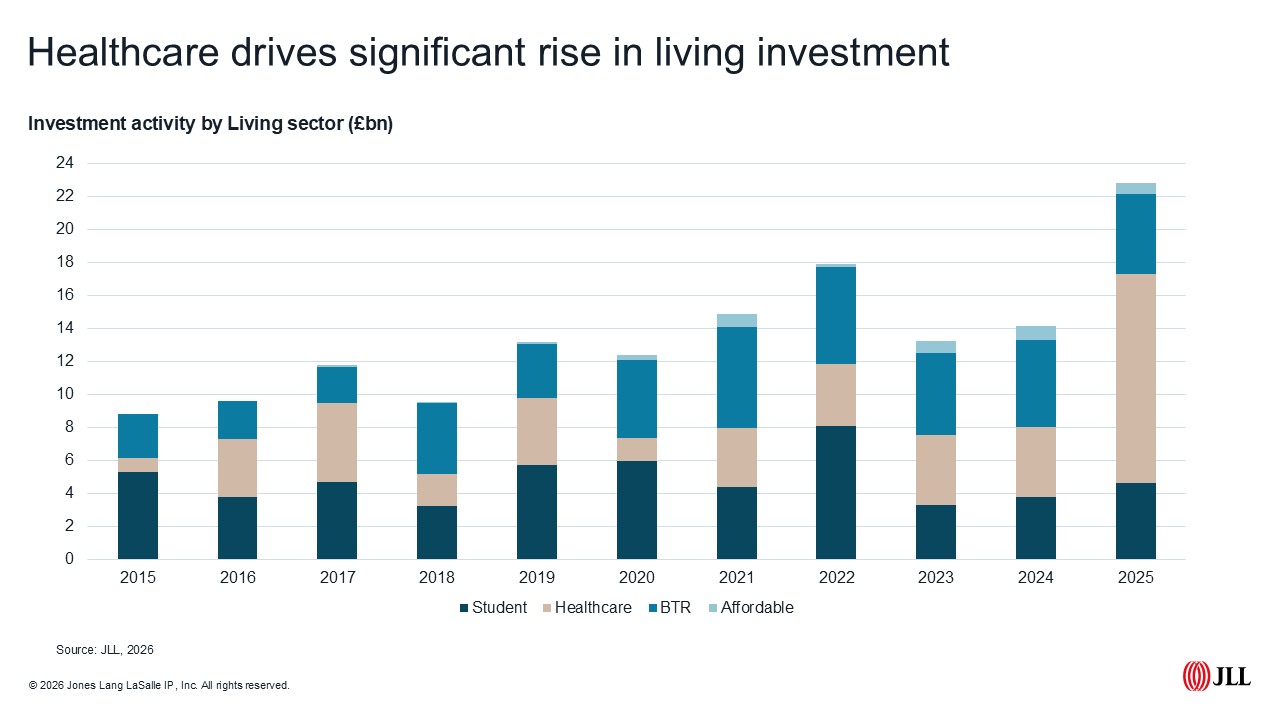

A record £22.8bn was invested in UK Living in 2025, with healthcare contributing more than half of the total as it ended the year with several £1bn+ M&A deals. Excluding healthcare, investment grew a more modest 2 per cent to £10.1bn, rising for the second year running from the trough in 2023 (£8.9bn). Single family investment overtook multifamily in 2025 with £2.6bn invested, accounting for just over half of all build-to-rent investment last year.

The 2024/25 student data released by HESA this week gives us a glimpse at the first full year impact of restrictions on international students brought in at the start of 2024. The number of international students has fallen 10 per cent from its 2022/23 peak, totalling 686,000 in 2024/25. Though still above the UK's (now scrapped) 600,000 target, it does represent a significant fall at a time that universities remain reliant on international tuition fees. The slowdown among international students resulted in a marginal 1 per cent decline in total university students. Despite a degree of uncertainty, investors were still active in the student market, with £4.6bn of investment completing across the year, up 22 per cent annually. For more analysis on the UK living sector read Karl Tomusk’s latest Living Roundup here.

Prime Central London

Pre-budget anxiety means drawing firm conclusions from Q4 data isn’t advisable, but there were some glimmers of hope for a sunnier year ahead. Prices across PCL were down 7.3 per cent year-on-year in Q4, following a 1.6 per cent quarterly decline.

But with more clarity post-Budget activity began to pick up with transactions above £10 million rising by 36 per cent over the quarter, with buyers who’d agreed prices pre-Budget gaining the confidence to exchange. Activity below £2million

was driven largely by domestic buyers, with transactions at this price point rising 7 per cent over the quarter. Activity in the £2–5 million and £5–10 million ranges was more subdued, likely reflecting lingering uncertainty

earlier in the quarter around proposed tax changes. To read Meg Eglington’s take on the Q4 PCL market click here.

JLL Research

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.

Disclaimer: © 2025 Jones Lang LaSalle IP, Inc. All rights reserved. Data within this report is based on material/sources that are deemed to be reliable and has not been independently verified by JLL. JLL makes no representations or warranties as to the accuracy, completeness or suitability of the whole or any part of the report which has been produced solely as a general guide and does not constitute advice. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. JLL, its officers, employees shall not be liable for any loss, liability, damage or expense arising directly or indirectly from any use or disclosure of or reliance on such report. JLL reserves the right to pursue criminal and civil action for any unauthorized use, distribution or breach of such intellectual property.