With the government committing to one “fiscal event” a year, the Spring Forecast was, as expected, policy light but forecast heavy. There was some (rare) positive news for the Chancellor, with cash receipts coming in stronger than the Budget watchdog expected, rising to the tune of £22bn. An increase in receipts from self-assessment tax returns (including the impact of fiscal drag pulling more taxpayers into higher bands) alongside VAT and CGT increases are helping fill the coffers. This will be welcome news for the government, particularly following the loss of the Gorton and Denton by-election, with both the Greens and Reform making significant gains.

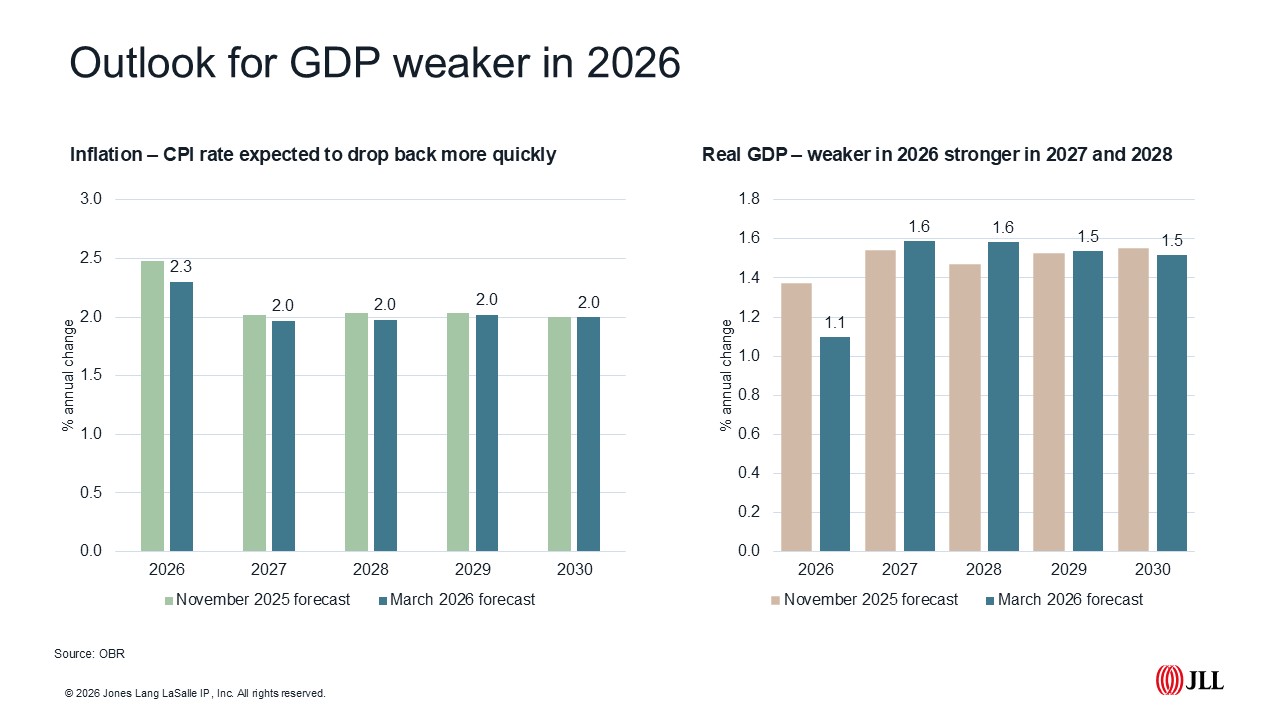

The outlook for UK GDP remains subdued, with the Office for Budget Responsibility downgrading their view on 2026 growth from a 1.4 per cent forecast in November to 1.1, although the outlook for 2027 and 2028 improved marginally from 1.6 per cent growth to 1.7. This downgrade was due, in part, to a drop in net migration, with the OBR now expecting net migration to average 235,000 a year between 2026 and 2030, 60,000 a year lower than the 295,000 it was predicting in November.

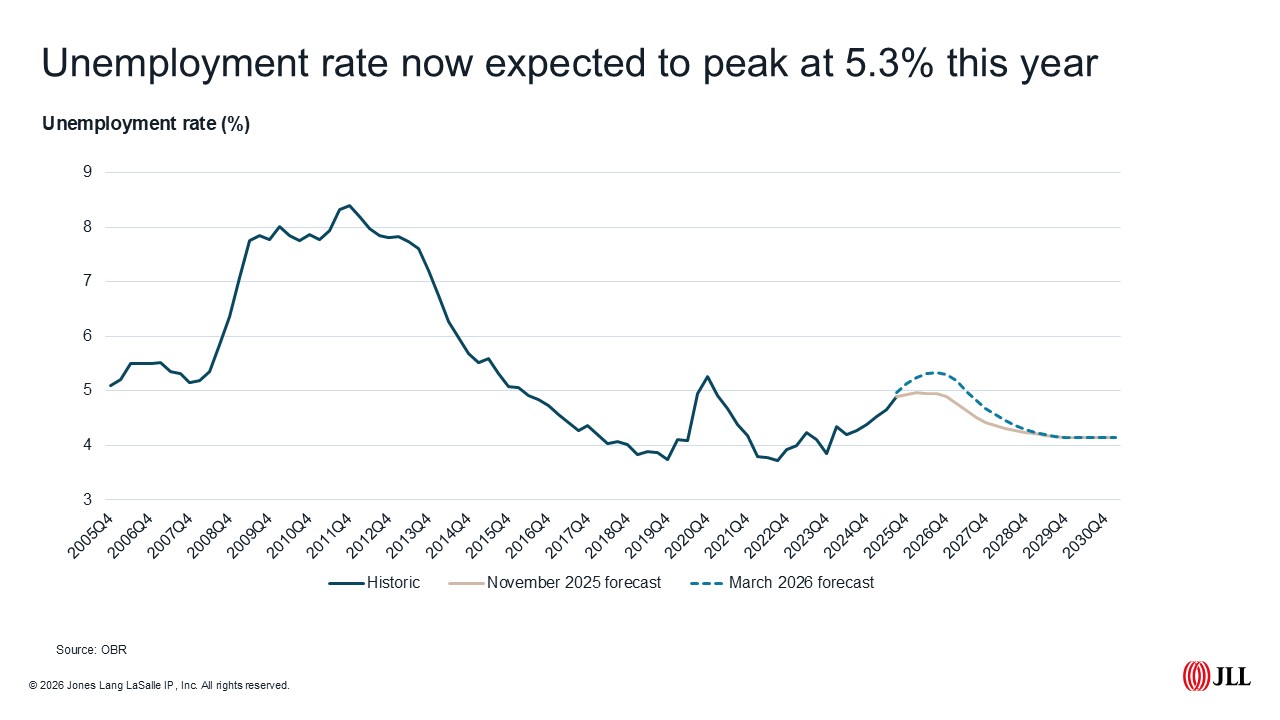

Unemployment is now expected to peak at 5.3 per cent this year, up from a November forecast of 4.9 per cent. Youth unemployment remains particularly challenging, with 16 per cent of 16- to 24-year-olds out of work in Q4 2025, nearing an 11-year high.

Inflation is expected to fall back from 3.5 per cent in 2025 to 2.3 per cent in 2026 – down from November’s forecast of 2.5 per cent. But as the conflict in Iran continues to escalate, the Office for Budget Responsibility’s forecasts looked out of date even before they were published, with continued military action in the Middle East sending shockwaves through the markets. Airline stocks dropped by more than 10 per cent while fears over oil supply saw the share prices of BP and Shell spike. Oil has hit $85 a barrel but crucially remained below the $128 threshold reached following Russia’s invasion of Ukraine in 2022. Similarly, the price of liquefied natural gas, of which around 20 per cent of global supply comes out of Qatar, almost doubled compared with pre-conflict levels as QatarEnergy confirmed a suspension in production following an attack on its primary operational hubs.

There are many reasons aside from the fiscal to hope for a quick resolution, but fears over the impact of a drawn-out conflict on inflation remain. Expectations that we may see a further rate cut at the next MPC meeting on 19th March have all but evaporated - the odds on a rate cut in March slashed from north of 70 per cent last week to around 20 per cent at time of writing.

Housing market

There was little in the Spring Forecast for housing, with those pinning their hopes on an outside chance that much needed buy side incentives would be announced again disappointed. Although rumours abound that the government is continuing to consult on how best to support first-time buyers. The OBR still expect the government’s housebuilding aspirations are unachievable, forecasting 1.3 million homes UK wide by 2029/30, 200,000 short of the government’s England only target. That said, the Spring statement adds 30,000 to the previous figures published in November. Here at JLL we’re a little more pessimistic, with expectations of closer to 1 million homes over the forecast period.

House prices were expected to rise by an average of 2.5 per cent per annum over the next five years, with only a marginal 0.2 percentage point increase and another 0.1 percentage point rise expected in 2027 and 2028 over the November outlook. This is more pessimistic than the JLL view, with our UK forecast expecting just shy of 20 per cent increase in prices by the end of 2029 against 16.4 per cent forecast over the next five years by the OBR.

In other news

Houses prices edged up in February, with the Nationwide Index showing prices rising 0.3 per cent month-on-month. But with inflation at circa. 3 per cent, prices on an inflation adjusted basis fell, meaning further improvement in affordability. For rents, Homelet’s reported average UK rental values rose 2 per cent in the year to February. The North East was the only English region to record above inflation increases in rents at 4.6 per cent, with rents rising in real terms in Scotland (+4.6 per cent) and Wales (3.1 per cent).

Yet despite notional increases in spending power in most markets, prospective buyers remained cautious in January. Mortgage approvals dropped below 60,000, their lowest for two years. Of course, January is never the busiest month for the mortgage markets, but the promise of better rates ahead, as well as continued economic uncertainty around growth and job security could well be impacting here. We’ll need a few more months of data to tell.

In case you missed it

Our latest JLL Big Six Residential Development Report shows the average price of new build apartments across the six cities rose 2.4% in 2025, while rental growth slowed to 1.7%. In the build-to-rent market, total investment volumes exceeded £1bn in 2025, 21% higher than 2024. North of the border the passing of the Scottish Housing Bill, and the exemption of BTR from future rent caps is expected to boost activity and put Scotland firmly back on investors’ radars. To download a copy of the report click here.

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.

Disclaimer: © 2026 Jones Lang LaSalle IP, Inc. All rights reserved. Data within this report is based on material/sources that are deemed to be reliable and has not been independently verified by JLL. JLL makes no representations or warranties as to the accuracy, completeness or suitability of the whole or any part of the report which has been produced solely as a general guide and does not constitute advice. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. JLL, its officers, employees shall not be liable for any loss, liability, damage or expense arising directly or indirectly from any use or disclosure of or reliance on such report. JLL reserves the right to pursue criminal and civil action for any unauthorized use, distribution or breach of such intellectual property.