Welcome news of a two-week ceasefire in the Middle East has seen markets react favourably. Brent crude prices dropped to below $100 a barrel and shares in several UK and US property REITs have rallied. The outlook for the Bank Rate has also shifted, with markets now expecting a more cautious approach to rate hikes from the Bank of England this year. Forecasters, who had been predicting up to three 25bps increases in 2026 are pulling back and now expecting one. Swap rates at time of writing have also dropped, a positive sign for the fixed rate mortgage market.

But even if, as hoped, the ceasefire holds, much of the damage done to global supply chain and energy costs will take some time to unravel, with a similar impact on mortgage rates. All of which means any significant rebound in activity in the housing market may well take time to feed through.

Uncertainty hangs over the housing market

A series of decidedly glum indicators have been released over the last week, highlighting the impact of geopolitical unrest on the UK housing market. First up Halifax, whose house price index suggested prices dipped 0.5 per cent in March compared with February, meaning prices were just 0.8 per cent higher than they were a year ago.

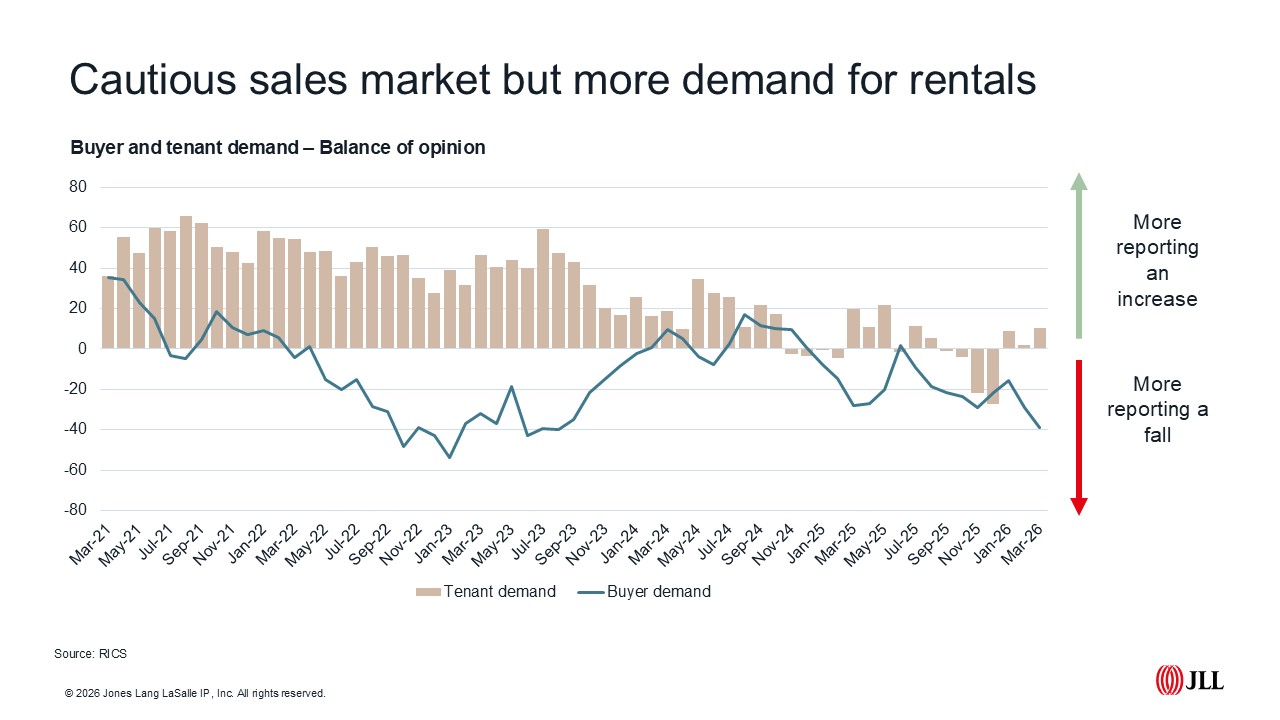

This was followed by the latest RICS survey, the first to fully cover the impact of Middle East conflict, which showed a drop in activity and appetite in the sales market. Needs based buyers were still looking to transact, and those with pre-March mortgage deals locked in were still active, but the discretionary market looked like it retreated again last month.

New buyer enquiries fell sharply, with the net balance declining to -39 per cent from -29 per cent in February—the weakest reading since August 2023. Agreed sales followed suit, dropping from -13 per cent to -34 per cent, also the lowest since summer 2023. Near-term sales expectations turned markedly pessimistic at -33 per cent (from -4 per cent), whilst twelve-month outlook sentiment weakened to -1 per cent. New instructions registered a net balance of -6 per cent, indicating a marginally slower flow of listings. Unsold stock on agents' books rose to an average of 47 properties, up from 45 at the start of the year.

On pricing, near-term expectations dropped to -43 per cent from -19 per cent in the previous month indicating accelerating downward pressure anticipated over the next three months. The twelve-month outlook sits at +2 per cent, suggesting a broadly flat trend— but is down sharply from +43 per cent in January.

But while caution reigned in the sales market, tenant demand rose (+10 per cent net balance in March) alongside a continued drop in landlord instructions (remaining firmly negative at -25 per cent). Expectations for rental growth strengthened to +29 per cent, with agents citing persistent supply-demand imbalances and expectations that the uncertain outlook in the sales market could benefit the rental market.

Construction activity remains muted

Geopolitical uncertainty also weighed heavily on the latest construction PMIs. The UK construction sector's woes deepened in March 2026, with house building bearing the brunt of the downturn, compounded by a wet first quarter that made construction even more challenging. Residential activity recorded the sharpest decline across all construction categories, with the index falling to 38.2—well below both commercial construction (47.1) and civil engineering (44.8). Remember, a score below 50 signals a contraction in activity. This marks the fifteenth consecutive month that the sector has contracted, driven by falling client confidence and a dearth of new project starts.

What's particularly concerning for housebuilders is the acceleration and unpredictability of build costs. Input price inflation surged to its highest level since November 2022, with nearly half of all construction firms reporting rising cost burdens. The outbreak of war in the Middle East has disrupted supply chains, pushing up fuel, transportation and raw material costs. International shipping delays meant that supplier delivery times rose for the first time since last summer, adding further pressure to already squeezed margins.

Falling short

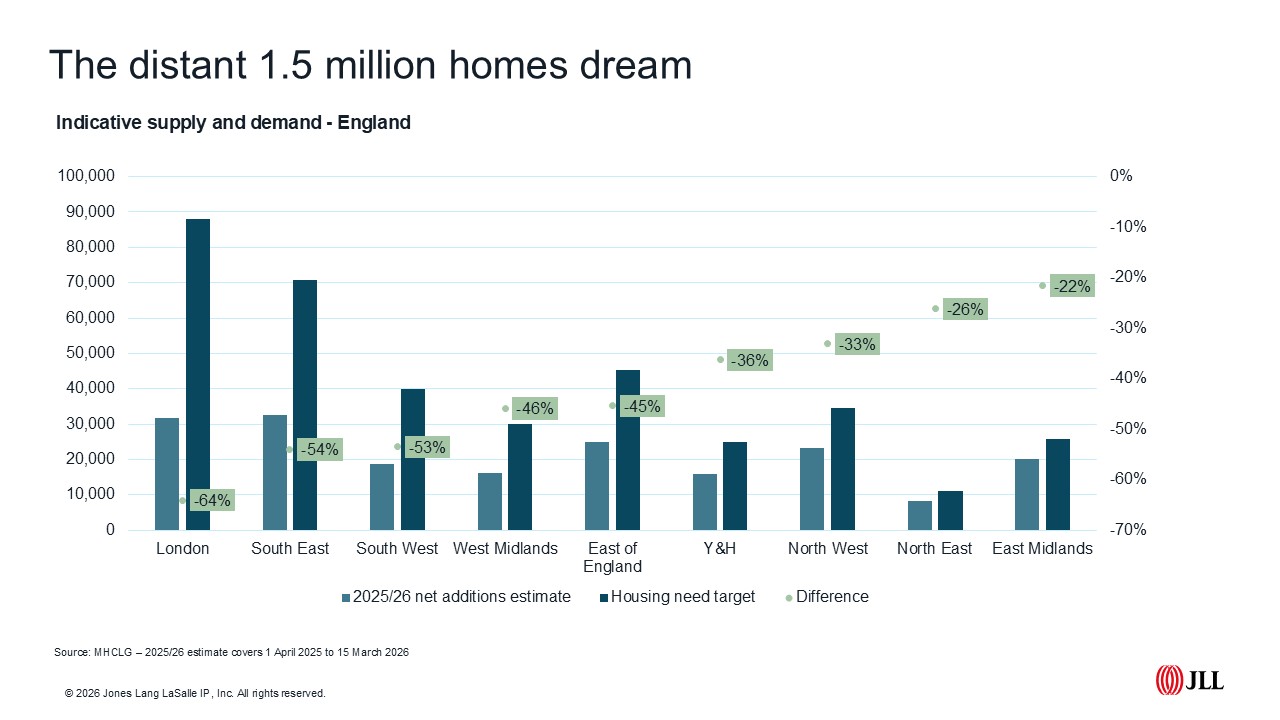

The latest estimated net additions figures highlight the need for further incentives to develop. Government figures suggest 191,300 homes were completed in England between 1 April 2025 and 15 March this year. This was 17,300 short of the previous 12-month total. Comparing estimates on net additions with housing needs targets shows the clear need for further intervention, with net additions (the most generous measure of housing delivery) 48 per cent shy of the 370,000 annual housing need across England.

Housing Bank to the rescue?

With a 180,000-home supply shortfall, debt more expensive, and viability more challenged, the launch of the National Housing Bank could not have come at a more important time. The National Housing Bank (NHB) is part of a raft of Homes England and GLA initiatives to promote further activity in the housing market, effectively aiming to alleviate some of the debt-based challenges faced by those delivering homes.

The scheme was launched with much fanfare, with a £100m JV with Aviva championed as an example of how the schemes could turbocharge activity. The NHB has £16 billion of debt, equity and guarantees aiming to assist in the delivery of half a million new homes. The bank also needs buy-in from the private sector, with an investment prospectus published to attract more than £50 billion of private capital. Announced in the 2025 Spending Review, the Bank is a wholly government-owned subsidiary of Homes England. Its mission is to drive housing delivery and create communities, with returns only covering the cost of government borrowing. The Bank will work alongside Homes England as an independent subsidiary to provide tailored support packages.

The NHB is open to different providers from large housebuilders to SMEs. Crucially it is not limited to those operators providing affordable or build-for-sale homes, with build-to-rent and later living also able to access funds. From 1 April 2026, the NHB offers seven debt products:

1-SME accelerator loans - providing site-specific lending enabling smaller developers to establish track records and scale operations. Targeted at supporting firms currently delivering up to 250 homes a year but looking to grow their output.

2-Revolving credit facilities - working with commercial lenders to provide multi-site facilities and land loans, again targeted at helping SME developers expand capacity.

3-Senior and mezzanine loans – targeted at mid-size developers with project-level funding, particularly for build-to-rent, later living and brownfield regeneration. Funding will sit alongside private capital to bring forward stalled projects.

4-Corporate balance sheet lending - supports housebuilders directly and sits alongside commercial lending, a key focus is supporting those specialising in Modern Methods of Construction.

5-Lending alliances - creating platforms leveraging private sector capital to broaden the Bank's reach and scale debt finance availability to SME housebuilders.

6-Infrastructure loans - long-term funding up to 15 years to large housebuilders and master developers for upfront infrastructure needs ranging from roads to placemaking.

7-Low interest loans for RPs - offers below-market interest rates to Registered Providers to unlock social and affordable housing investment, addressing pressures from increased debt costs and rising capital expenditure demands.

Partners are urged to reach out to their regional Homes England teams with specific sites or potential opportunities. With more information on the National Housing Bank available here.

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.

Disclaimer: © 2026 Jones Lang LaSalle IP, Inc. All rights reserved. Data within this report is based on material/sources that are deemed to be reliable and has not been independently verified by JLL. JLL makes no representations or warranties as to the accuracy, completeness or suitability of the whole or any part of the report which has been produced solely as a general guide and does not constitute advice. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. JLL, its officers, employees shall not be liable for any loss, liability, damage or expense arising directly or indirectly from any use or disclosure of or reliance on such report. JLL reserves the right to pursue criminal and civil action for any unauthorized use, distribution or breach of such intellectual property