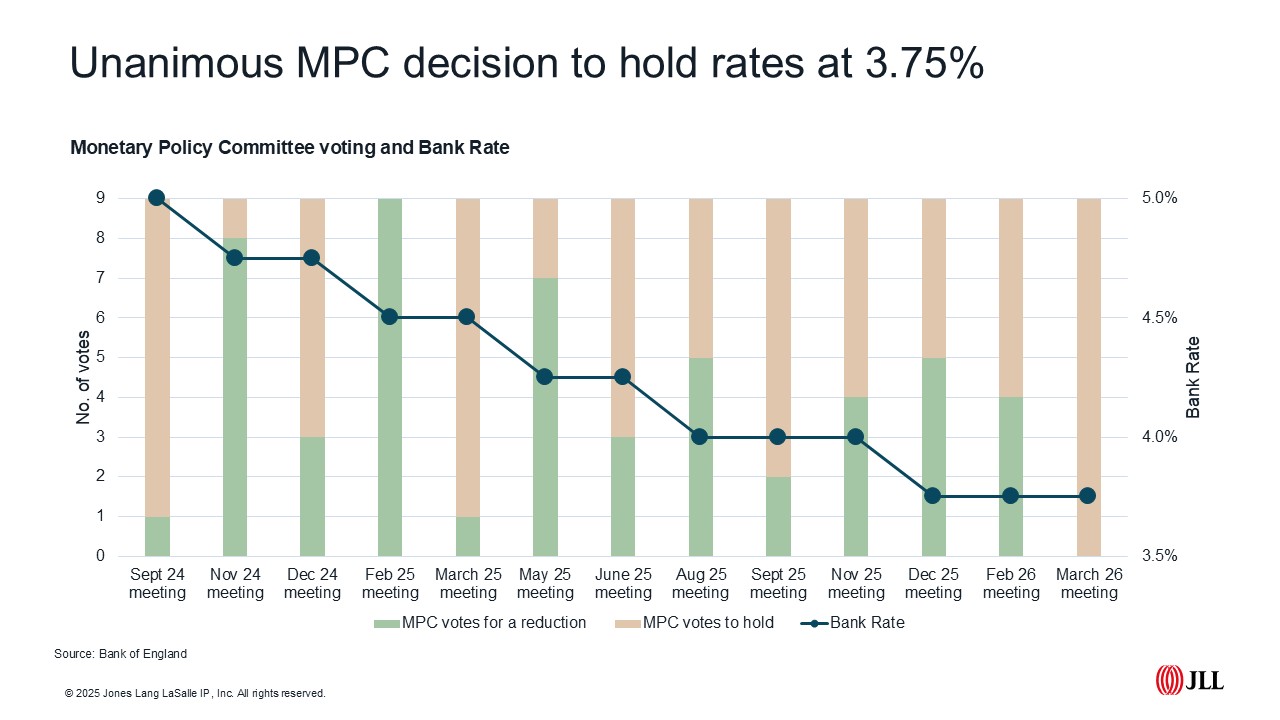

All nine members of the Monetary Policy Committee unanimously voted to hold rates at 3.75 per cent at the March meeting. This came as little surprise considering the many unknowns around the length and impact of the conflict in the Middle East. Just a few weeks back, following the February meeting the odds on a rate cut topped 80 per cent, with observers hinting at further downward movements in the coming months. Obviously much has changed since then.

But with odds on a reduction in the Bank Rate falling from near certainty to less than 10 per cent in the run-up, market attention shifted to what committee members were saying rather than the decision itself. Some thought (or hoped) the committee would choose to ‘look through’ energy cost driven inflation risk and concentrate on the ongoing weakness in the employment market. But the Bank’s key focus – keeping inflation in check rather than focussing on growth – won out.

The Bank of England's decision to maintain its current interest rate stance reflects a broader pattern of monetary policy restraint among major central banks worldwide this week. The narrative emerging from all the Central Banks’ announcements was one of caution. The US Federal Reserve opted to keep rates within its existing 3.5 per cent to 3.75 per cent range, signalling continued caution in its approach to monetary adjustment. Canada held firm at 2.25 per cent, while both the Bank of Japan at 0.75 per cent and the European Central Bank at 2 per cent announced they too would be maintaining their respective rates for the time being.

Outlook for inflation

Maintaining its key focus on inflation, the Bank emphasised that it will be monitoring developments "extremely closely" and stands ready to act to ensure inflation returns to the 2 per cent target level. With the Consumer Prices Index (CPI) having fallen to 3 per cent in January, MPC forecasts back in February had anticipated inflation dropping back towards 2 per cent from as early as April, largely thanks to falls in the energy price cap. However, on Thursday, the MPC acknowledged that recent increases in wholesale energy costs would delay inflation's return to target, as these rises were already translating into higher fuel prices at the forecourt. The Committee now expects inflation to sit at around 3 per cent in the second quarter of 2026, a notable increase from the 2.1 per cent in the February forecast.

Looking ahead, higher wholesale gas prices are likely to feed through into a higher Ofgem energy price cap from July, which the Bank anticipates could add 0.75 percentage points to inflation over the third quarter. When combined with the prospect of firms passing on elevated energy costs to consumers, the MPC warned that CPI inflation could climb to as much as 3.5 per cent in the third quarter, considerably higher than the previous 2 per cent forecast.

Employment figures

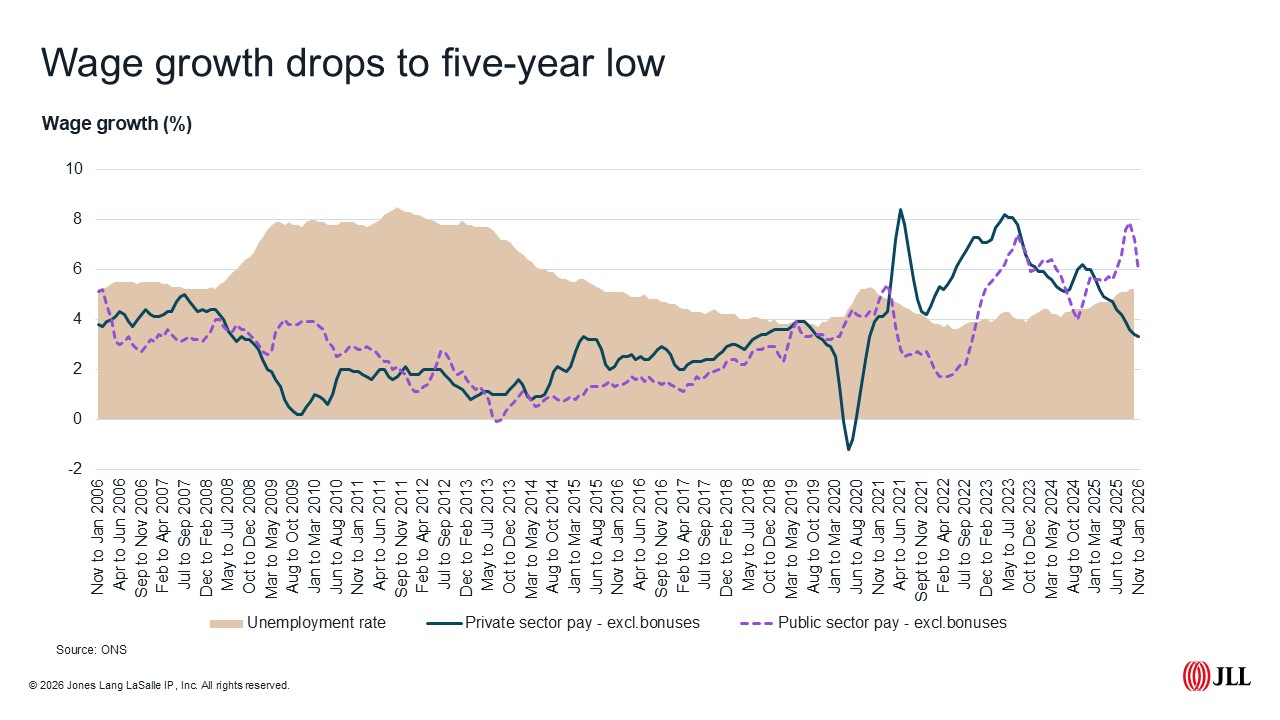

The latest government figures revealed continued weakness in employment markets. Growth in private sector wages, excluding bonuses, was 3.3 per cent in the three months to January, below the 3.5 per cent expected by the markets. The jobless rate remained at 5.2 per cent, marginally lower than the 5.3 per cent forecast previously.

Impact on mortgage rates

With oil breaching $100 a barrel and the prospect of higher inflation for longer, swap rates (the benchmark rate for fixed rate mortgages) have risen. Markets are certainly pricing in the uncertainty – particularly in the short term, with two-year swaps now sitting higher than five-year. Products are being pulled, with the last of the sub 4 per cent deals now disappearing from lenders’ books. Moneyfacts data shows the average shelf-life of mortgage products fell from 33 days in early February to 14 in early March, the lowest for over two years.

Moneyfacts tracked the removal of 600 mortgage products over the past few weeks. Not great news for borrowers, but this does reflect only around 10 per cent of the overall market. The number of mortgage products available is still more than double those offered in the weeks following the 2022 mini-Budget. Average two-year fixed rates have risen from 4.84 per cent at the start of March to 5.32 per cent on the morning of the MPC meeting.

What does this mean for the housing market?

Uncertainty often leads to greater caution among buyers, particularly those who are less needs driven. In the short term, we expect those who have already locked in more favourable mortgage deals will be keen to push through transactions. But for those thinking of entering the market, heightened uncertainty alongside higher rates will likely deter some from moving.

Our 2026 forecast, made back in November, always predicted a stronger H2 than H1. It’s still too early to call, and we are obviously all hoping for a swift resolution to the current conflict. But if the conflict persists, we could see a delay in the recovery this year. We’re reviewing our outlook and will keep you posted once we have a clearer view.

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.

Disclaimer: © 2026 Jones Lang LaSalle IP, Inc. All rights reserved. Data within this report is based on material/sources that are deemed to be reliable and has not been independently verified by JLL. JLL makes no representations or warranties as to the accuracy, completeness or suitability of the whole or any part of the report which has been produced solely as a general guide and does not constitute advice. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. JLL, its officers, employees shall not be liable for any loss, liability, damage or expense arising directly or indirectly from any use or disclosure of or reliance on such report. JLL reserves the right to pursue criminal and civil action for any unauthorized use, distribution or breach of such intellectual property.