Hopes of a more settled geopolitical landscape in 2026 have been quickly dashed, with Trump’s intervention in Venezuela, little progress on a peaceful resolution in Ukraine, the return of transatlantic friction over Greenland and distressing scenes in Iran leaving questions over the prospect of further US intervention.

But there are signs that economically 2026 could prove more settled. The Budget is behind us and the promise of one fiscal event a year – and hopefully lessons learnt from the pre-Budget paralysis last year – mean we could see more activity this year. The Bank of England has hinted they expect inflation will drop back to levels at or close to their 2 per cent target by the end of 2026, with two or more rate cuts this year looking more likely.

There was some promising news on GDP in November, recovering from an October contraction of 0.1 per cent to grow 0.3 per cent in November, a five-month high. It isn’t always prudent to read too much into monthly GDP numbers, but the increase in November does point to modest growth rather than a contraction once the Q4 figures surface. The reopening of the Jaguar Land Rover production line supported the November figure (and fed into the negativity in October), with car manufacturing rising 26 per cent month-on-month.

For the housing market 2026 also brings some much-needed clarity on acronyms, with the NPPF, SAHP, RRA and rent settlement now published or expected to be released in Q1. We’re forecasting a slow recovery rather than a step change in prices and activity this year. Our latest forecasts, published in early December, point to marginal growth of 2 per cent in prices and 2.5 per cent in rents this year. If you missed them, you can read more on our latest forecasts here.

Market activity

UK property transactions reached 100,350 in November, up 7.7 per cent annually and 1.3 per cent month-on-month, according to HMRC data. This sits just 1 per cent below the long-term pre-pandemic average (2013-2019). Rightmove’s full year figures show sales agreed in 2025 were 3 per cent higher than 2024. But with transactions taking more than six months to progress from listing to exchange the slowdown in activity observed later in 2025 will take months to show up in the figures, meaning we’re in for a few months of underwhelming figures, even if the market is feeling a little rosier.

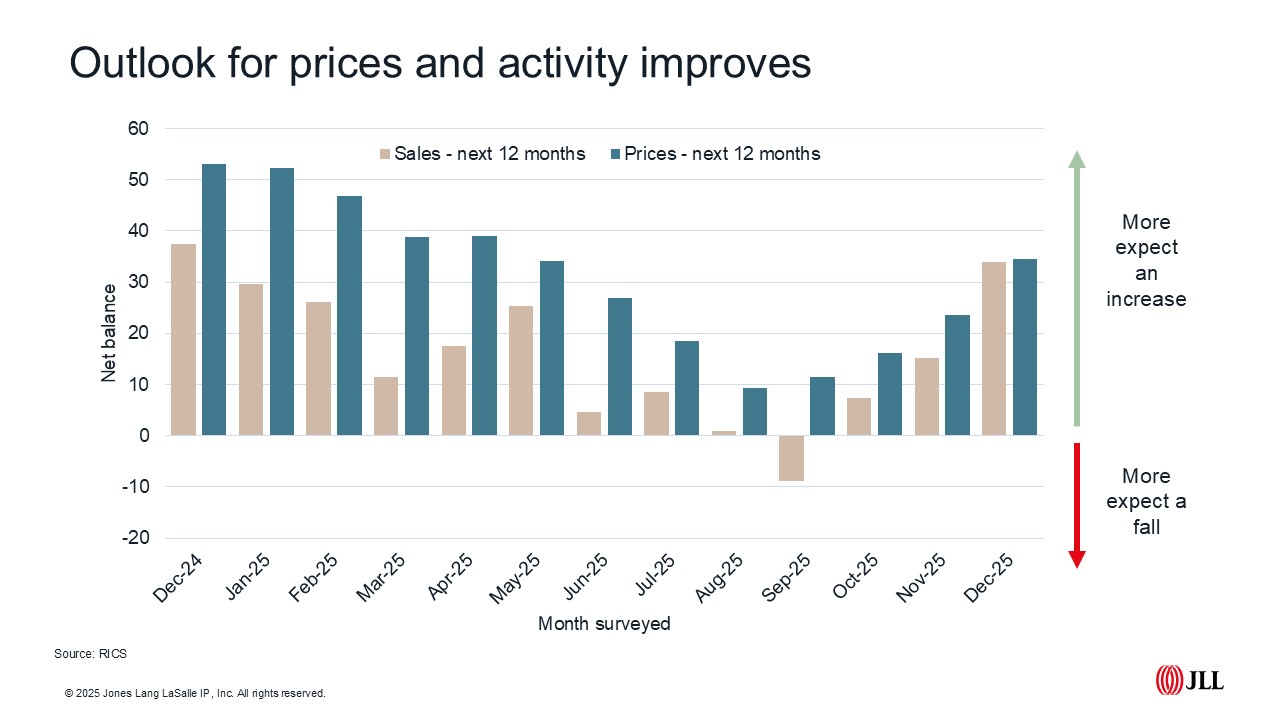

The RICS survey provides a timelier picture of market sentiment. It has been decidedly gloomy of late, with uncertainty pre-Budget weighing heavily on respondents’ market outlook. But their December survey, the first post-Budget, looks more promising.

December isn’t the best month to take the temperature of the housing market, with little change in new instructions reported by RICS and the near-term outlook for prices remaining broadly flat, but a higher number of respondents are now expecting

prices to rise in 2026. A net balance of +35 per cent of respondents expect an increase, up from +16 in October and +24 in November. Sales expectations rose too, with a net balance of 34 per cent of respondent expecting activity to increase in 2026,

the highest reading since December 2024. Rents are expected to rise in 2026 too, with respondents to the survey forecasting growth of 3 per cent nationally in 2026.

Prices

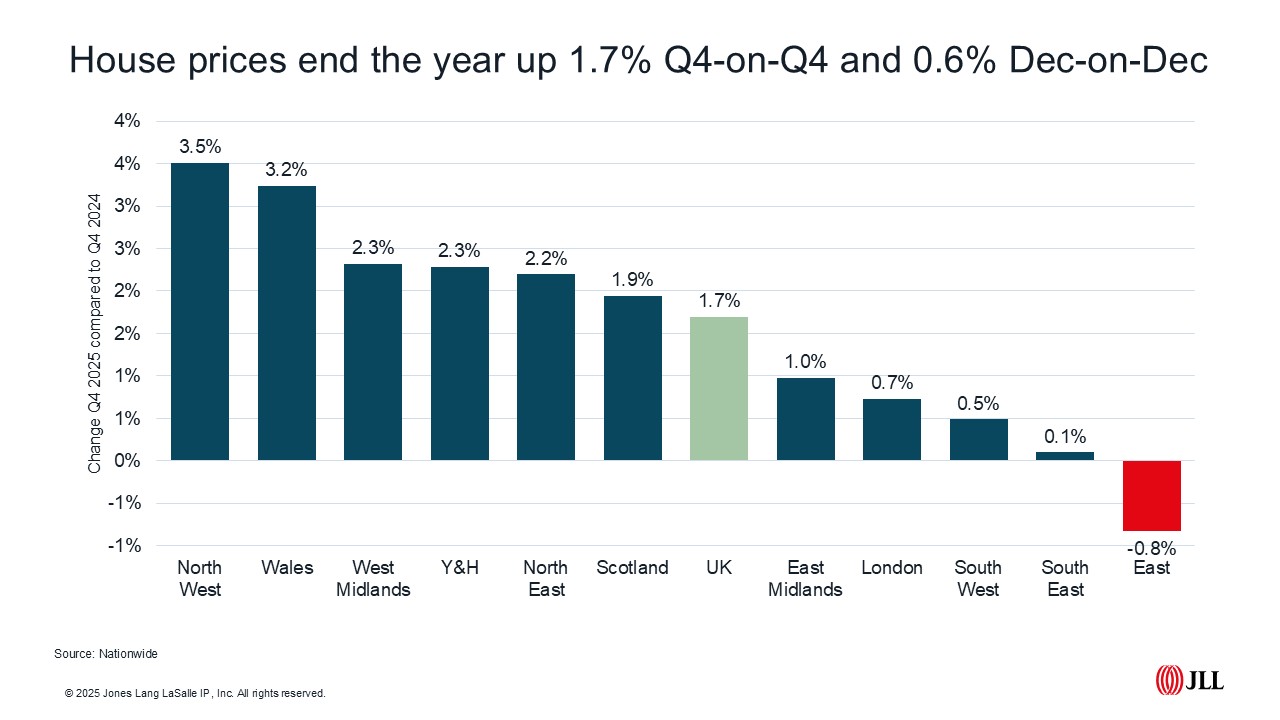

Budget jitters acted as a dampener on house prices in the final months of 2025. Both Halifax and Nationwide reported UK house prices declining month-on-month in December, with Halifax showing a 0.6 per cent decrease and Nationwide recording a 0.4 per cent drop. Despite these monthly declines, annual price growth remained marginally positive at 0.3 per cent (Halifax) and 0.6 per cent (Nationwide) for the year ending December 2025. At a country and regional level prices in Q4 2025 rose in all areas bar East Anglia, where prices fell 0.8 per cent annually. Growth in the price of houses continues to outpace flats, with semi-detached houses recording 2.4 per cent growth annually, UK wide, compared with a 0.9 per cent fall for flats.

Rents

The rental market followed typical seasonal patterns, with the final months traditionally bringing higher stock levels and modest rental adjustments. December 2025 saw average rents for new lets fall 1.5 per cent month-on-month, resulting in annual growth of 2.6 per cent for the year according to Homelet. The North East was the strongest English region at 6.6 per cent, Scotland recorded a solid 4.0 per cent annual increase, with Wales achieving 2.9 per cent growth over the same period.

Mortgage market

UK mortgage approvals dipped in November, with 0.7 per cent fewer approvals month-on-month and 6.7 per cent fewer annually. But considering this coincided with the run up to the Budget, falls were more marginal than some predicted and the 12-month rolling rate remains resilient.

This points to increased activity this year, supported by an increase in more competitive mortgage rates reaching the market. The effective interest rate on newly drawn mortgages averaged 4.20 per cent in November, down from 4.53 per cent in February, with best-buy fixed rates falling to 3.5 per cent in mid-January.

JLL Research

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.