House prices rose 4.1% in the year to January 2025 according to the latest figures from Nationwide, down from 4.7% in December but still a higher annual growth figure than any other month in 2024. This follows an uptick in mortgage approvals in December, with seasonally adjusted numbers showing a 0.7% rise on November levels and a 28% increase on a slow December 2023. If the MPC lower rates, as expected, at their next meeting on 6 February we could see a further increase in activity in February, although those shopping for fixed rates may find these reductions have already been factored into current deals.

Growth taking off?

Heading out to Davos Rachel Reeves was keen to stress Britain was open for business. And on her return the growth narrative continued, with announcements on the intention to support a third runway at Heathrow and investment in the Oxford Cambridge Growth Corridor, which could bring in an additional £78bn for the UK economy by 2035. In addition, Reeves reiterated commitments to rail improvements, new mass transit infrastructure and the regeneration of Old Trafford, potentially including a new stadium for Man United – all of which involve unlocking additional sites for viable housing development.

To accelerate the timeline for a third runway, planning changes will be pushed through to ensure gaining planning for infrastructure projects becomes simpler and less ponderous. Similar changes have been proposed for our sector, with planning reform sitting alongside Labour’s ambitious plans for housing delivery.

UK housing starts subdued

Released this week, the latest starts and completions figures (for Q3 2024) make for sobering reading, with 37,000 new homes started, 28% lower than the Q3 average pre-pandemic. Starts in the year to September were down 35% on the previous 12 months. Completions dropped back too, with 7% fewer in the 12 months to September and a 13% drop annually in Q3. To put these numbers in context, completions across England totalled less than 157,000 in the last 12 months, meaning that if we relied on completions alone it would take us more than nine years to get the 1.5 million homes the government has committed to deliver in five.

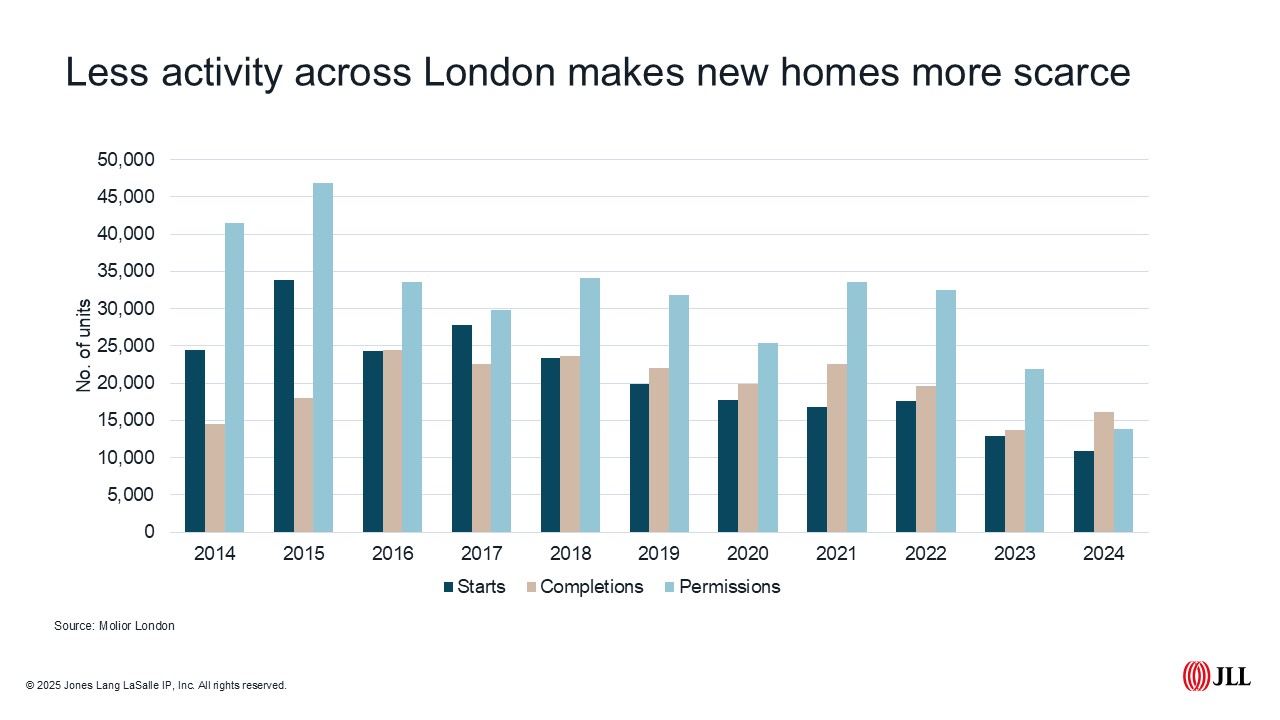

A similar picture in London

According to Molior London, the number of homes started across Greater London last year fell 16% on 2023 and were 50% lower than the previous 10-year average. It was a similar story for completions, down 20% on the 10-year average, and planning permissions, down 58% on the 10-year and 37% annually. But ending with better news, applications rose annually in 2024, the number of units at application stage up by a third compared with 2023.

Relaxing the rules on non-dom taxation

A recent report by New World Wealth and Henley & Partners suggests the UK has seen 26,000 millionaires depart since the start of 2017, with a net outflow of 9,500 in 2024 alone. With many countries now courting footloose high net worths with more attractive tax rates, the UK is looking increasingly out of step. Plans to change tax rules around non-doms were initiated under the Conservatives and re-iterated in the Budget, but in a recent interview Rachel Reeves suggests the Government is ‘re-thinking’ it’s plans.

Reeves stated they will be tabling an amendment to the Finance Bill to include a more generous Temporary Repatriation Facility, which enables non-doms to bring money into the UK at a lower tax rate. She also reassured non-doms over double taxation and inheritance tax liabilities for those fearing they would become liable for tax in more than one country.

Prime Central London

Conflicting messages were coming out of Prime Central London in Q4. Activity rose, with the number of homes changing hands at a 10-year high for fourth quarter sales, but fewer buyers were in the market at the top end and overall prices dipped 4% in 2024 due in part to fewer higher value homes trading towards the year end.

As usual the fourth quarter was relatively quiet for the Prime Central London lettings market, but activity was in line with Q4 2023, with 3% fewer new lets agreed. Full year figures show there were almost 4,400 new lets agreed in Prime Central London in 2024, 5% higher than 2023. While activity gradually increased during the year, we saw slower growth in rents. The JLL PCL Rental Index shows average annual rental growth cooling over the past two years from a high of 15% annual growth in Q1 2022. Rents ended the year 0.4% higher than at the end of 2023. Looking ahead stock levels are lower as we move into Q1 2025, with 15% fewer homes on the market to let than at the end of the third quarter and 8.5% fewer than in the same period a year earlier.

Click here to read our latest PCL report.

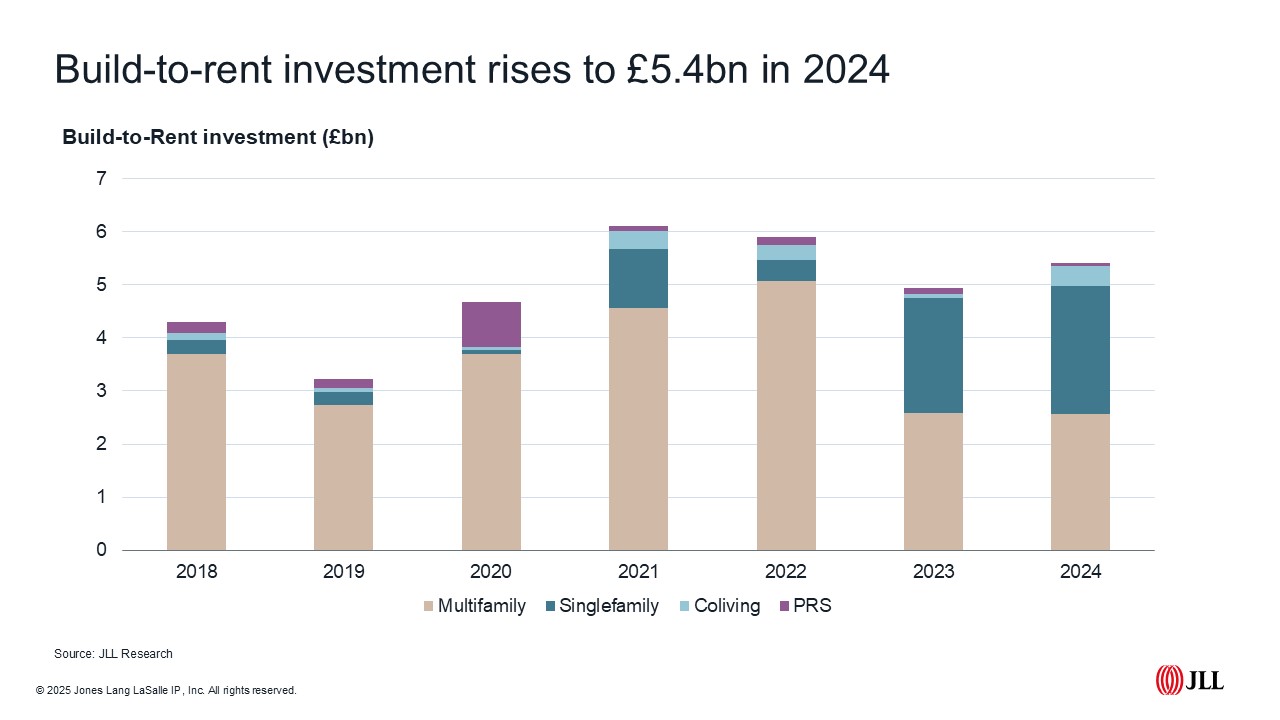

Build-to-rent investment rises in Q4

Q4 2024 was the most active quarter for build-to-rent investment since 2021, marking a significant increase on a lacklustre third quarter. Investment in the fourth quarter totalled £2bn, taking the full year total to £5.4bn.

Single family housing proved popular with investors, as they acquired 7,000 new rental homes in 2024. However, despite a record year for single family investment, a rise in multifamily in Q4 meant it ended the year marginally higher in overall volumes. Operational stock accounted for the bulk of multifamily transactions, with forward funding accounting for just a fifth of total investment. This is due in part to the fact the sector is maturing, with more stabilised stock to trade, but also reflects continued viability challenges faced by both the build-to-rent and build-to-sell markets.

To read more on our latest build-to-rent numbers Click here.