Good news on the UK economy has been hard to come by in recent weeks. But lower than forecast inflation figures have raised hopes and resulted in a much-needed positive response from the bond markets, with 30-year bond yields remaining elevated but down from their recent highs.

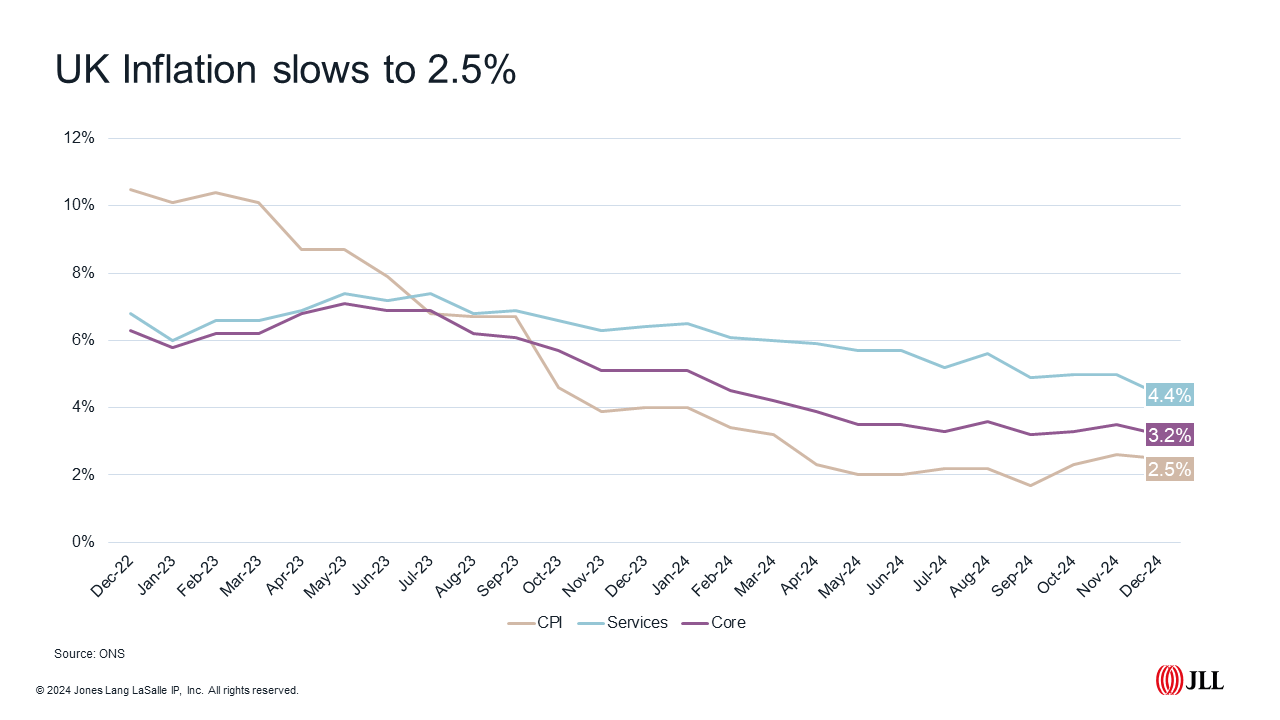

Latest figures from the Office for National Statistics show inflation fell to 2.5% annually in December, down from 2.6% the previous month, and lower than forecast. Core inflation fell to 3.2%, down from 3.5% in October, and services inflation, at 4.4%, was at its lowest since Q1 2022. Economists expected it would drop back to only 4.9%.

There was some positive news from across the pond, too. Consumer prices rose annually by 2.9% but core inflation, a figure which often influences policy makers’ decisions on rates dropped to 3.2%.

The response from the markets has been broadly positive, increasing the probability of further rate cuts when the Bank of England and Federal Reserve rate setters next meet. In the case of the MPC, 6 February is the date for your diaries.

UK Economy

UK GDP edged up in November, rising by a disappointing 0.1%. The back end of 2024 was slow, with growth weak in Q3 and a plateau forecast in Q4. For 2025 the consensus is for a return to growth, with the outlook more positive at 1.3% compared to 0.9% last year. Forecasts, according to Consensus Economics, range from the most optimistic at 1.8%, to the most pessimistic at 0.8%. For 2026 the forecast for growth is the same at 1.3%.

The labour market remains robust if a little underwhelming. Higher public sector pay and an increase in the minimum wage align with rising private sector real wages, which are expected to support real spending this year.

That said, challenges remain, with employers facing increased costs coming out of the Autumn Budget: higher national insurance contributions, the rise in the minimum wage and higher business property rates, all of which will likely impact both recruitment and inflation over the coming months.

Mortgage rates

We expect interest rates to fall, particularly following the latest inflation figures. Indeed, with low inflation and growth lower than the long-term trend, it is hard to see why the MPC wouldn’t act. The question remains when.

We are also facing a global bond sell off that is pushing up benchmark bond yields. Again, we have seen this improve in recent days, but our fiscal situation remains challenging.

That said, the rapid rise in bond yields has not been mirrored by a similar rise in swap rates, meaning best buy mortgage rates haven’t increased quite as much as feared. As we go to press, best buy rates sit at 4.3% for a two-year fix and 4.2% for a five-year (both at 75% LTV).

Prices

The drop in mortgage approvals in November and rates remaining north of 4% are impacting buyer demand. In the latest RICS survey, more agents were still reporting an increase in new buyer enquiries, but the net balance fell back from +11% in November to +5% in December. However, the usual seasonal slowdown could be playing a role here, too.

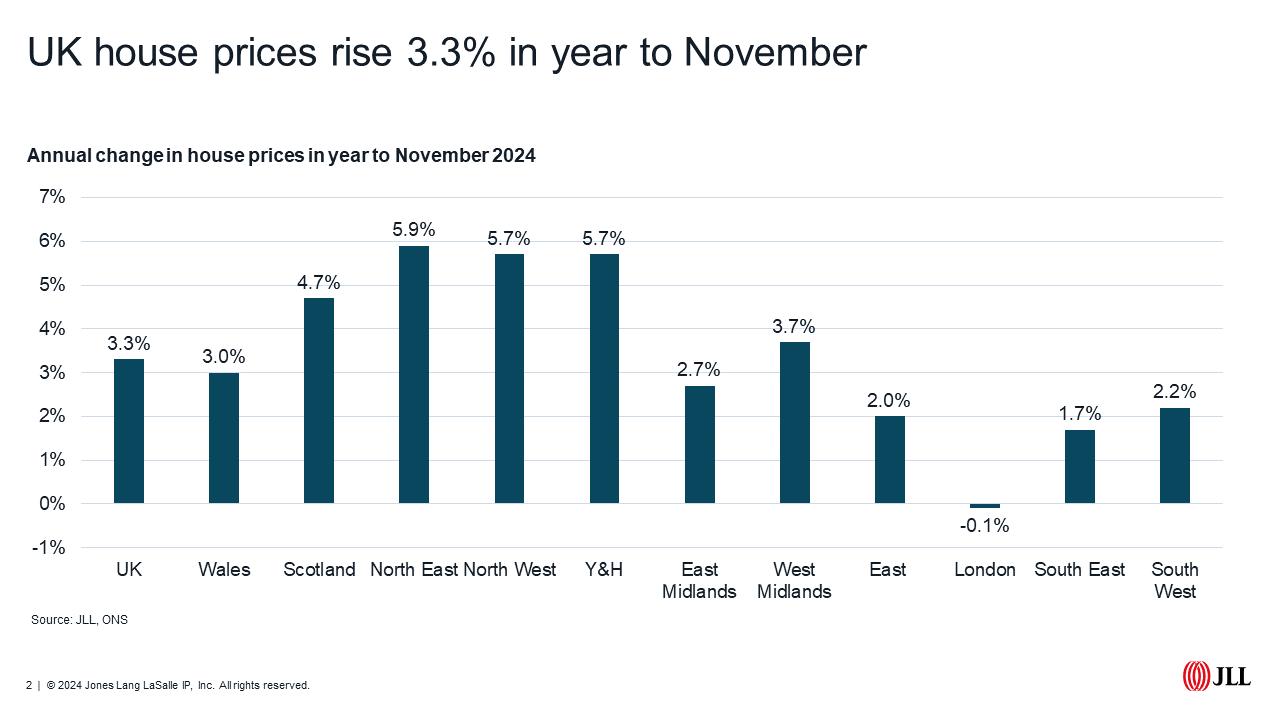

November figures from the ONS show average UK house prices rose 3.3% in the year to November 2024. Prices were broadly flat in London, down 0.1% annually, compared with growth of 5.9% in the North East.

Rents

December isn’t always the best month to take the temperature of the UK rental market. But the ONS rental index is still at near-record levels, averaging 9.0% in December, in line with the 9.1% annual change in November. Achieved rents on new lets show only marginal annual increases, falling to 1.3% across the UK in the year to December according to Homelet. New lets in London saw a modest annual fall of 2.6% in 2024.

But the outlook for rental growth remains positive, with the latest figures from the RICS suggesting a net balance of +37% of agents expected rents to rise in the next three months, up from +29% last month. This is expected to be driven by lack of stock, with more agents reporting new landlord instructions falling, a net balance of -27% from -13% in November.

Housebuilding

Private housebuilding price inflation rose to 3.7%, once again above CPI. Meanwhile, the UK Construction PMI recorded a third consecutive month of housebuilding contraction, in sharp contrast to construction as a whole, which continues to expand.

But some positive news from the housebuilding sector comes from Persimmon Homes, which reported the number of homes delivered in 2024 was up 7% annually, at the upper end of its expectations for the year.

Regulatory update

The Renters’ Rights Bill has now completed its passage through the House of Commons and is off to the House of Lords as it inches closer to becoming law. Several amendments were added this week, including a clause restricting landlords from requiring upfront payments of more than one month’s rent (alongside a security deposit of five or six weeks’ rent). We’ll be updating you separately on the Renters’ Rights Bill in the coming days.