It’s been a busy couple of weeks in Westminster. A changing of the Labour guard has seen Angela Rayner depart from her three posts as Deputy Prime Minister, Deputy Labour Party Leader and Housing Secretary. David Lammy takes on the Deputy Prime Minister role, Steve Reed replaces her as Housing Secretary and hustings have begun for the Deputy Leader post.

What Rayner’s departure – triggered by Stamp Duty – means for property taxes in the autumn Budget is unclear. What is, is the need for good advice. Let’s hope for more clarity in the run up to the Budget on 26 November.

UK economy stagnates

UK GDP appears to be following a similar path this year to last, with stronger growth earlier on in the year petering out over the summer. The latest monthly GDP figures show growth stagnated in July, following a rise of 0.4 per cent in June, taking growth

in the three monthly to July to 0.2 per cent. Tariffs, employer NI and potential tax changes in the Budget will all be impacting figures here, but it is important to take these monthly GDP figures with a heavy pinch of salt. They are often revised

and tend to fluctuate month-on-month.

Bond market headache

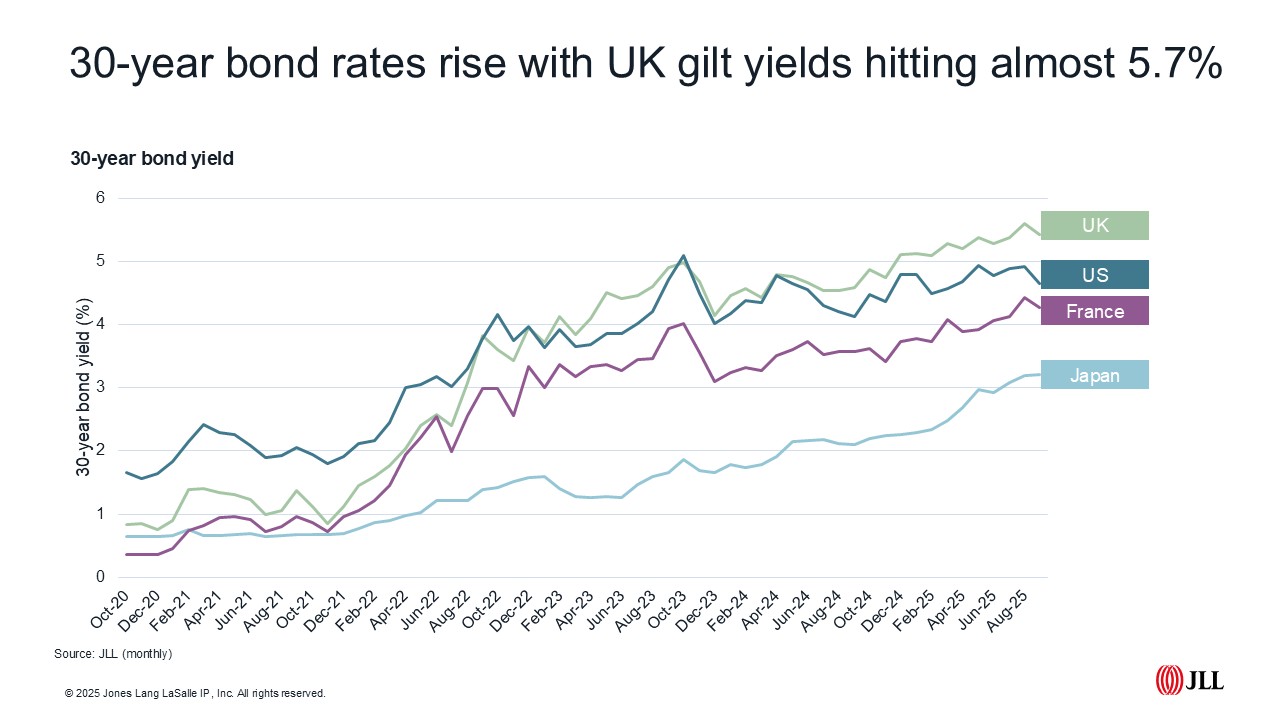

The Chancellor will be acutely aware of recent bond market volatility. Long-dated UK gilts – essentially IOUs from the government – hit a 27-year peak in early September, with 30-year gilt yields just shy of 5.7 per cent. But rates have eased somewhat since then, with the latest 30-year figure now sitting below 5.45 per cent.

Rising gilt yields directly increase government's debt servicing costs, creating a challenging fiscal backdrop and increasing the chance of further tax rises and/or spending cuts. This has implication for the housing market too, more directly through fixed rates, which are less likely to see any significant reduction while bond yields remain elevated, but also in terms of fiscal headroom. With much hoped for demand side incentives somewhat reliant on a healthier Treasury balance sheet.

Recent increases in long-dated bond yields aren't solely a UK phenomenon – other major economies have experienced similar upward movements in recent months. However, there are several UK-specific elements that cannot be overlooked, demonstrated by UK gilt yields moving from a middle-ranking position against other G7 nations' 30-year government bonds to amongst the highest.

While scepticism surrounding persistent inflation and Britain's economic prospects certainly plays a role, the story runs deeper. There's been a marked decline in appetite for long-dated bonds from pension funds and insurers – traditionally the most reliable buyers of government debt. This has left fewer purchasers in the marketplace. Adding to this challenge, recent modifications to UK pension regulations – ironically introduced to stimulate investment in growth assets – have further dampened demand.

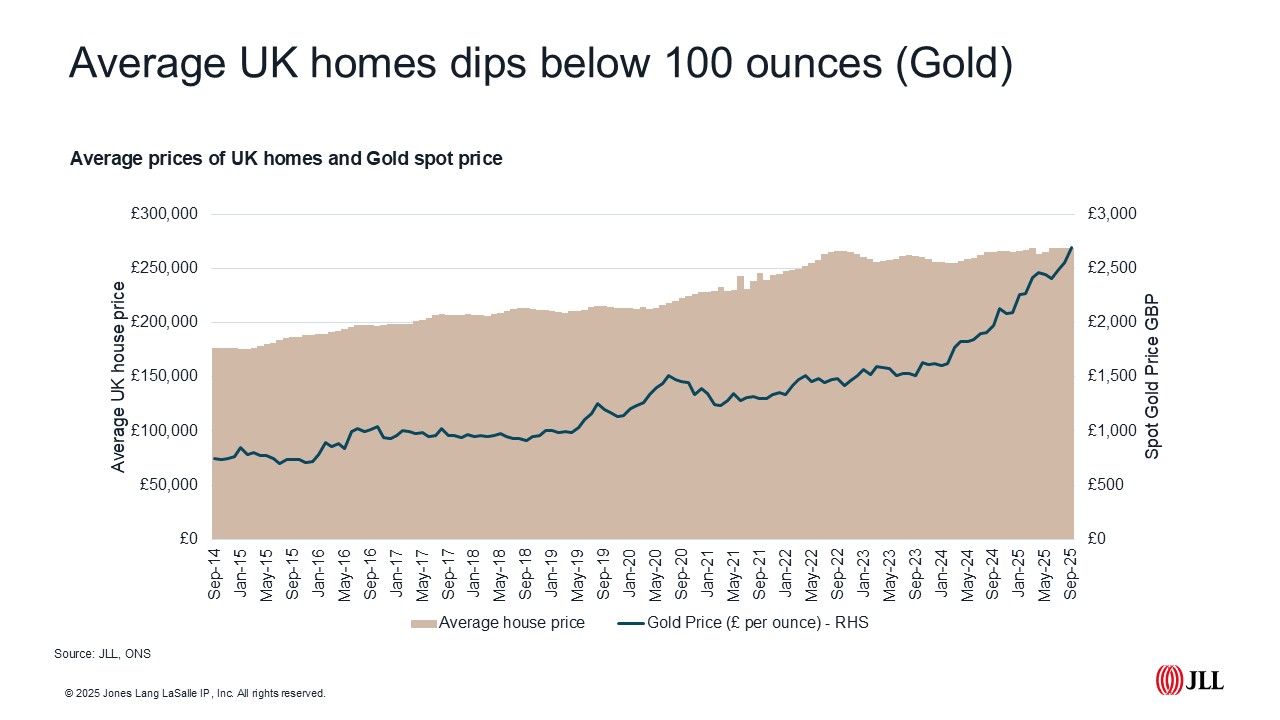

All that glitters

With an uncertain outlook globally, investors are flocking to safe-haven assets, reflected in the recent rally in gold prices. Spot gold prices exceeded US $3,500 per ounce in early September, with values up by nearly a third so far this year. Comparing gold prices with UK housing clearly demonstrates not only the recent outperformance but also the relative value in UK real estate. A decade ago, the average UK home cost the equivalent of 253 ounces of gold, in September with the price of gold exceeding £2,600 per ounce the average home could be bought for the equivalent of less than 100 ounces.

Housing market

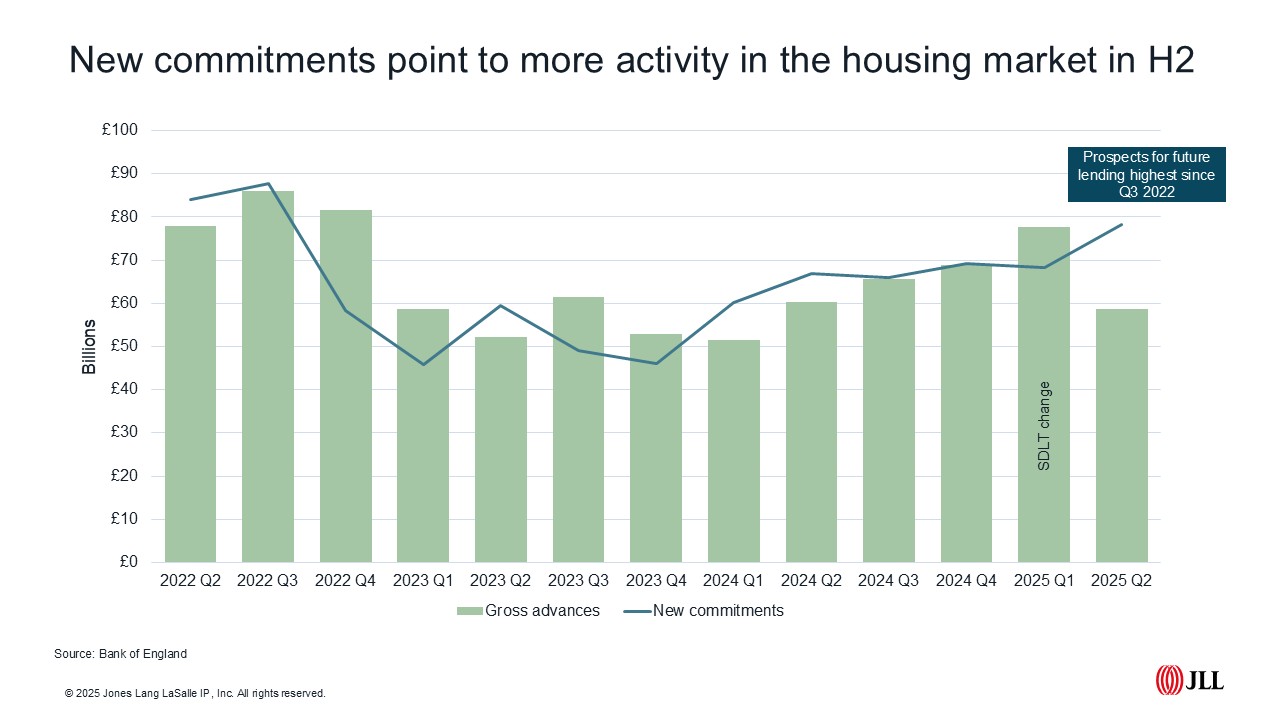

We’d expected fewer new mortgage advances in Q2 following the pre-1 April SDLT changes, with gross advances dropping 24 per cent on Q1 levels to their lowest since Q1 2024. Nothing to get too het up about though, as overall activity in H1 was up by almost £25bn or 18 per cent on H1 2024. Of greater interest were the new commitments figures (an indicator of future advances), which rallied, having plateaued in Q1. In Q2 more than £78 billion of new lending was agreed, up 15 per cent on Q1 and 17 per cent higher than the same period a year earlier. This was the highest quarter since pre-mini budget in Q3 2022.

The RICS Survey has made for gloomy reading in recent months, and the August edition was no different. The short-term outlook for prices and activity remains downbeat, due in part to the quieter summer period but also increasingly uncertainty around what could happen in the Budget.

Despite many of the key fundamentals being in a stronger position than they have been for some time (more stock, more motivated sellers and more options for borrowers) the temptation to sit on one’s hands remains, with Budget speculation doing little to tempt buyers out of the long grass.

It is a similar story for the rental market, with the latest RICS survey reporting demand holding steady with marginally more respondents seeing demand rise than fall. At the same time new landlord instructions remained firmly in negative territory, with a net balance of -37 per cent the weakest reported for over five years. With less stock reaching the market respondents were more positive on the outlook for rental growth over prices, with a net balance of +27 per cent of respondents expecting rents to rise in the next three months. For prices the short-term outlook was more negative but more still expected prices to rise than fall over the next 12 months.

Renters’ Rights Bill

The Renters’ Right Bill returned to the Commons on 8 September, edging closer to gaining Royal Assent. Most of the amendments suggested by the House of Lords were rejected. Amendments which ended up on the cutting room floor included the ability to charge higher deposits for tenants wanting pets, the inclusion of military housing, and the extension of student exemptions to smaller one- and two-bedroom properties. It’s now back with the Lords, who’ll have another chance to tweak the recommendations before returning to the Commons. Expect further back and forth as we keep you updated on progress over the coming weeks.

New research

Our residential research team has been busy this summer, with our latest Big Six Residential Development Report, Buyers and Tenants Survey and our Landlord Survey all released in recent weeks. If you missed any of our latest reports click here.

JLL Research