Residential

The UK multifamily sector turns 10 years old this year. While growth at first was slow, make no mistake, it is ramping up through the gears now.

The past 12 months saw just under £6bn invested in UK multifamily – making it the second largest market in Europe, still some way off Germany in first place, but with a gap starting to open on the rest.

But what scale will the sector be when it celebrates its 20th birthday in 10 years’ time?

The JLL Living Research team undertook some exercises comparing UK multifamily with its transatlantic cousin in the USA to try to answer this question. And, if our estimates prove to be correct, UK multifamily could become a £25bn-plus sector by the mid-to-late 2020s.

UK and US similarities

Now, it should be acknowledged that our workings are based solely on tracking the growth of US multifamily and then applying it to the UK. There is no certainty that the UK will grow exactly as the US did. However, there are some very good reasons to assume it might.

Both the UK and US have very similar trends in home ownership. In 2005, around 70% of American homes were owner occupied compared with 71% in the UK. By 2018, home ownership in the US had fallen to 64% in the US and 62% of UK households.

In both countries this fall in home ownership is driven not only by declining affordability, but also by the growth of a cohort of people who can see the benefits and flexibility that private renting can offer – particularly in dense urban areas where demand often outstrips supply.

The £25bn Question

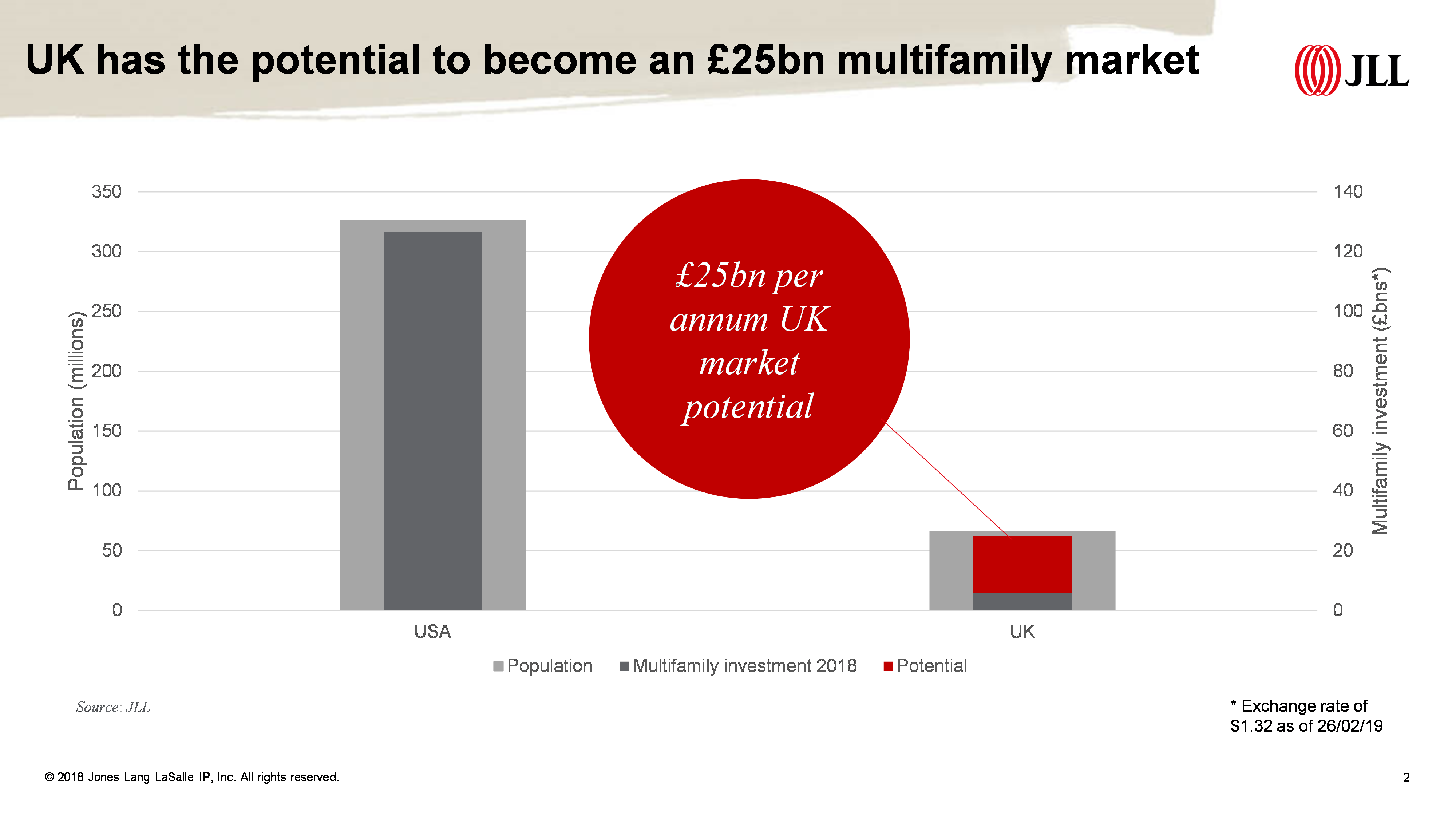

Firstly, we looked at the overall population of the UK and the USA and the current multifamily investment volumes in each country. The USA has a population of 326m and saw multifamily volumes of £126.7bn in 2018. The UK has 66 million people and its 2018 volumes were just under £6bn. If the UK was to see a proportionally similar investment in multifamily compared with its overall population as is currently the case in the USA, investment would increase to around the £25bn pa mark.

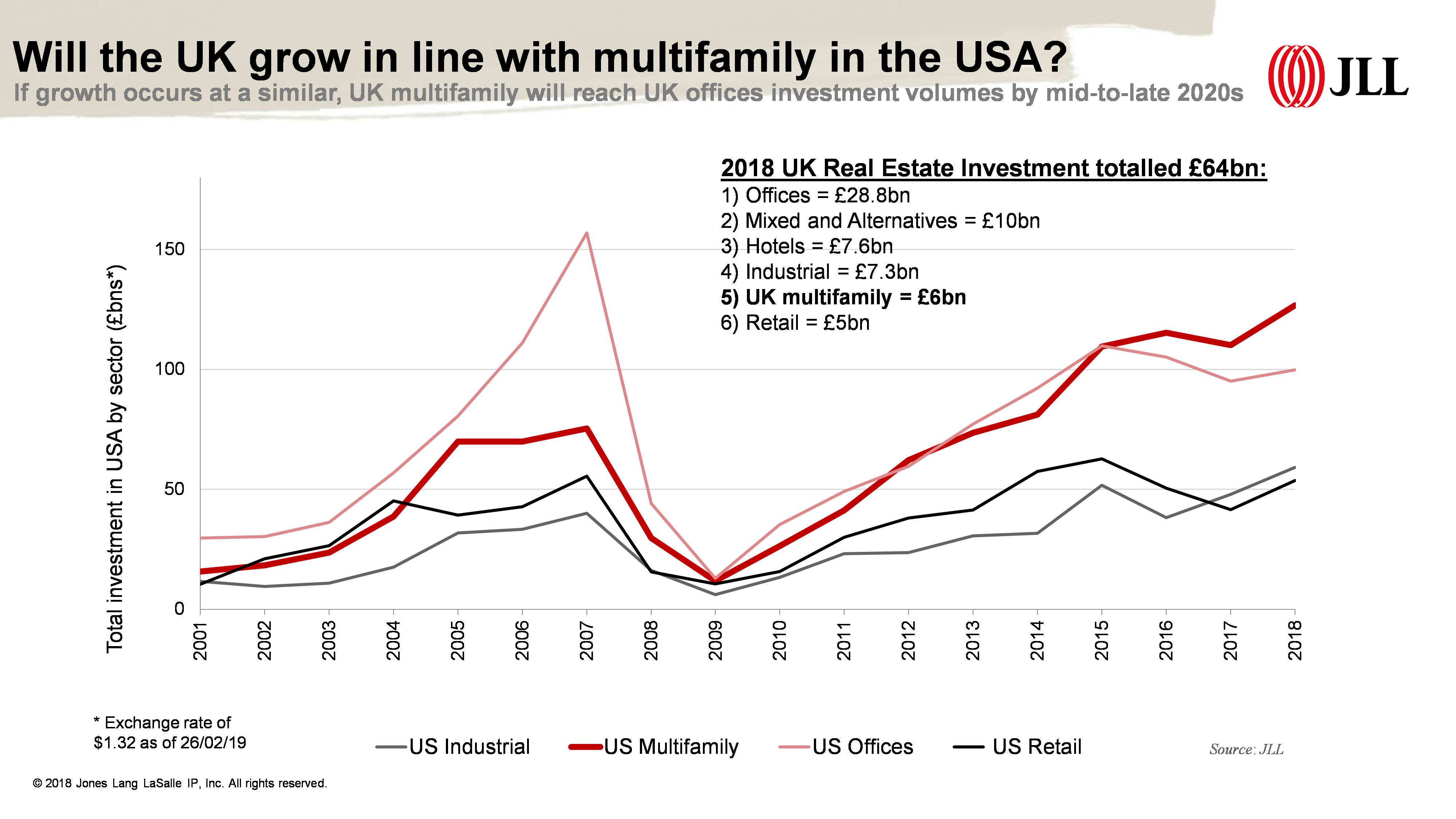

But how long would that growth take? Well, if we compare the growth story in the US, about 10 years.

Between 2000 and 2009 US multifamily was a similar scale investment class to US industrial and US retail. Incidentally, those three sectors are currently a similar scale in the UK.

Following the global financial crisis, US multifamily came more into line with the US offices sector – historically the largest sector - and from 2015 onwards multifamily has become the undisputed largest real estate investment class in the US finishing 2018 with volumes of £126.7bn compared with US offices at £100bn.

In comparison, the office sector is currently the largest sector in the UK with volumes of £28.8bn in 2018. If UK multifamily investment was to move in line with the offices sector, it could potentially even exceed our £25bn pa estimate.

Firstly, we looked at the overall population of the UK and the USA and the current multifamily investment volumes in each country. The USA has a population of 326m and saw multifamily volumes of £126.7bn in 2018. The UK has 66 million people and its 2018 volumes were just under £6bn. If the UK was to see a proportionally similar investment in multifamily compared with its overall population as is currently the case in the USA, investment would increase to around the £25bn pa mark.