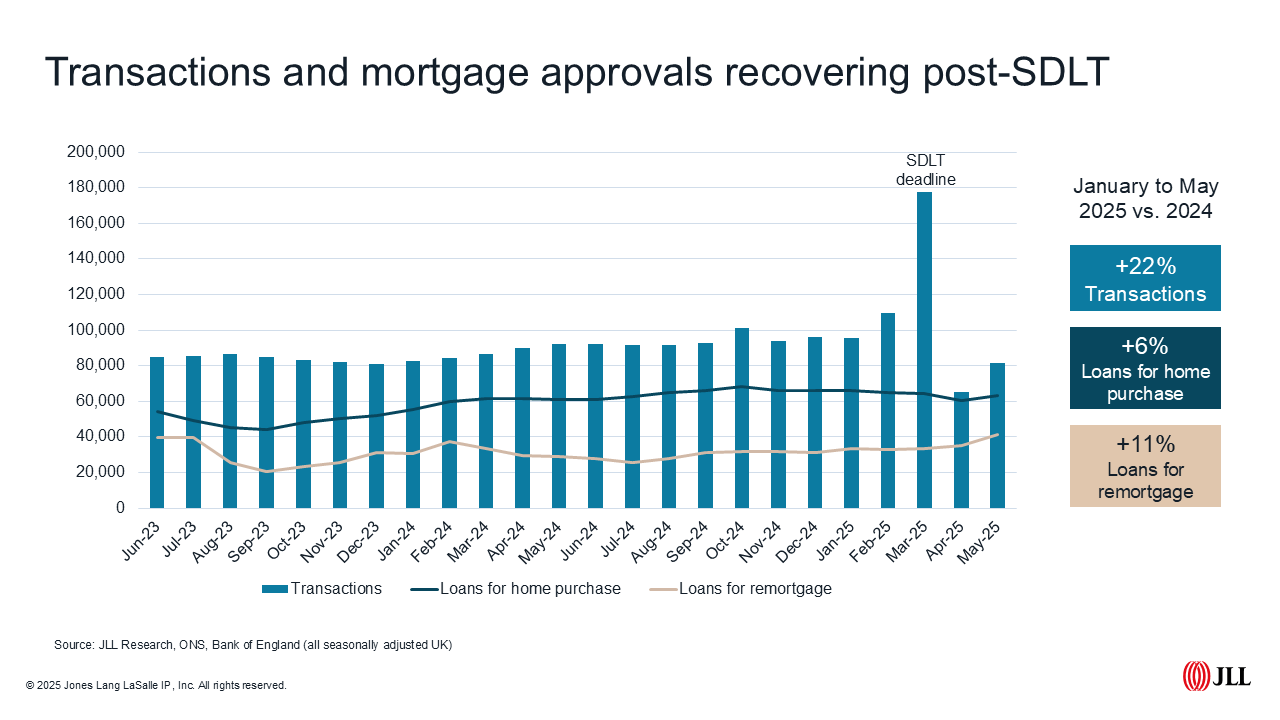

Three months on from the March stamp duty deadline and the housing market is gradually emerging from the SDLT fog.

Zoopla is reporting sales agreed in the four weeks to mid-June are up 6 per cent annually, but stock levels continue to rise more quickly than demand, meaning increases in activity are not driving significant price rises.

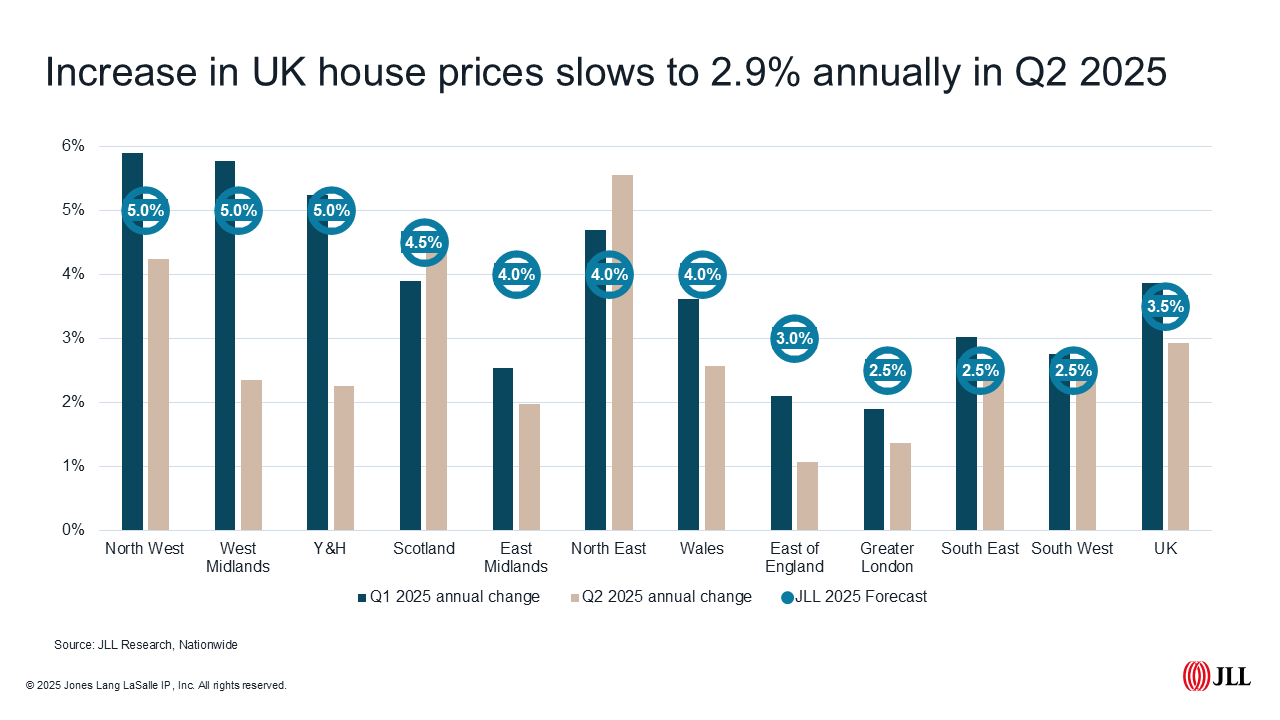

House prices

Nationwide's house price index shows prices dipped 0.8 per cent in June compared with May, meaning annual growth in prices dropped back from 3.5 per cent in May to 2.1 per cent last month. Expect to see annual averages increase a little in the coming months as the market continues to settle.

Zoopla reported asking prices rose 1.4 per cent annually in May, with stock on the market up 14 per cent year-on-year. This outpaced new buyer demand, rising by 7 per cent over the same period. Higher value markets saw the most marked increase in stock for sale, with activity at the top end of the market more sluggish than at the lower end. Prices in areas where house prices average under £200k rose 2.7 per cent compared with falls of 0.7 per cent in areas where prices top £500k.

Market activity

Mortgage approvals numbers began to recover in May, rising 3.9 per cent month-on-month on a slow April and 3 per cent higher than May 2024. But these numbers point to a steady rise in activity rather than a significant uptick. Average rates paid on new loans fell in May to 4.47 per cent with sub-4 per cent rates now available for both two- and five-year fixes for those with higher deposits. Forecasters are still anticipating up to two further rate cuts this year, taking the bank rate to 3.75% by the year end, but uncertainty around swap rates means that we are not expecting to see further significant falls in best buy rates in the near term.

Following a slow post-SDLT April, transactions recovered in May. Seasonally adjusted figures show there were 25 per cent more sales in May than April, but volumes remained 12 per cent lower than the May figure a year ago.

What does this mean for our outlook?

The time taken to sell a home (from listing to completion) now exceeds 200 days according to research by TwentyEA. This means homeowners listing their homes today would be expected to pick up the keys to their new home in late January 2026.

As well as increasing the likelihood of a sale falling through – time is often the killer of deals - this means that prices achieved on completion for homes in 2025 will largely reflect offers already accepted by vendors. As a result, even if we see a pick-up in activity later in the year, with more competitive mortgage rates and improved buyer confidence increasing activity, this uptick will be reflected in the 2026 rather than 2025 stats.

Our forecasts for this year, made back in November, were for a gradual recovery in prices, aided by more competitive mortgage rates and political certainty following a Labour majority at the General Election. While the benefits of a strong majority have been tested in recent weeks and the outlook for the UK economy remains underwhelming, the housing market continues to follow a path of slow but steady recovery.

Despite the stamp duty changes muddying the waters more recently, we are leaving our current forecasts for 3.5 per cent annual growth in UK prices in 2025 unchanged. Similarly, our expectations that higher value markets would lag in 2025 are still evident in the latest house price data, meaning we still expect that price growth in London will be more modest, rising by 2.5 per cent in 2025.

A different story in Central London

The only market where we are revising our 2025 forecast is Central London. Ongoing uncertainty around government plans to tax (or not) non-doms on their global assets means fewer prospective buyers at the top end of the market this summer. Here at JLL we've seen 8 per cent fewer new applicants registering with our offices in Q2 this year versus last, with LonRes data showing the numbers of sales so far this year at £5million or more are down 14 per cent and £10million plus sales down 20 per cent.

Sold prices (excluding new homes) fell 3.9 per cent annually across Prime Central London in Q2 2025, meaning our expectations for 3 per cent growth by the year end is increasingly unlikely. Additional tax liabilities for overseas buyers and those buying additional properties from April, alongside ongoing uncertainty around the non-dom regime, are all impacting buyer appetite. A U-turn on the exposure of non-doms' global assets to UK inheritance tax could help, but many will be waiting for further clarity before making their decision to stay, go or relocate. In the meantime, buyers remain cautious and stock levels in the second-hand market, up 13 per cent annually, are outstripping demand.

Relative scarcity of stock in the new homes market in central London means we are not seeing any notable reduction in prices, but activity remains skewed towards owner-occupiers and needs-based purchasers rather than investors, with sales volumes lower than historic norms.

We expect some markets - particularly those neighbourhoods more reliant upon high-net-worth overseas buyers - will see prices end the year lower than they started, but others could see small single digit annual increases this year. This means overall we expect prices to be flat in 2025, with growth of 2 per cent forecast in 2026.

The slowdown in rental growth experienced across most UK markets is following the path we forecast in November, so we'll be maintaining our current forecast for growth nationally of 3.0 per cent in 2025.

JLL Research

JLL’s Residential and Living team consists of over 300 professionals who provide a comprehensive end-to-end service across all residential property types, including social housing, private residential, build to rent, co-living, later living, healthcare and student housing.

Disclaimer: © 2025 Jones Lang LaSalle IP, Inc. All rights reserved. Data within this report is based on material/sources that are deemed to be reliable and has not been independently verified by JLL. JLL makes no representations or warranties as to the accuracy, completeness or suitability of the whole or any part of the report which has been produced solely as a general guide and does not constitute advice. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of JLL. JLL, its officers, employees shall not be liable for any loss, liability, damage or expense arising directly or indirectly from any use or disclosure of or reliance on such report. JLL reserves the right to pursue criminal and civil action for any unauthorized use, distribution or breach of such intellectual property.