It’s been a busy couple of weeks since we last updated you following the UK Budget. Trump is heading back to the White House for a second time, the Bank of England has dropped the bank rate 25bps to 4.75%, and here at JLL we’ve released our latest house price forecasts. The latter obviously grabbing the lion’s share of headlines….

The latest figures from the Office for National Statistics show the UK economy all but plateauing in Q3, with economic growth of 0.1% recorded, below the 0.2% forecast and lower than the 0.5% figure for Q2. Understandably the Chancellor is disappointed with these numbers and will be hoping that with the budget behind us we’ll see more activity and a shift away from pre-Budget inertia.

Wages rising

Annual growth in weekly earnings rose 4.8% in the three months to September, according to the latest figures from the Office for National Statistics. Wage growth remained above inflation, rising 1.4% in real (inflation adjusted) terms. These figures support assertions by the Bank of England that some heat is coming out of the labour market as we move towards the end of the year and remains in line with expectations.

The latest from the RICS

In contrast to the lacklustre economic news, the latest RICS survey showed some signs of cautious optimism in the housing market. The headline net balance (remember the RICS report on balance of opinion so anything in positive territory suggests more agents reporting a rise than a fall) for new buyer enquiries was positive for the fourth consecutive month, albeit little changed from September at +12%. Sales activity looked to be edging up too, with a net balance of +9% of agents reporting an increase. This is the third consecutive monthly rise, following broadly negative readings since early 2022. Outlook on price growth remained positive too, with the net balance of agents expecting prices to rise over the next 12 months increasing to +20% in October, up from +12% the month prior.

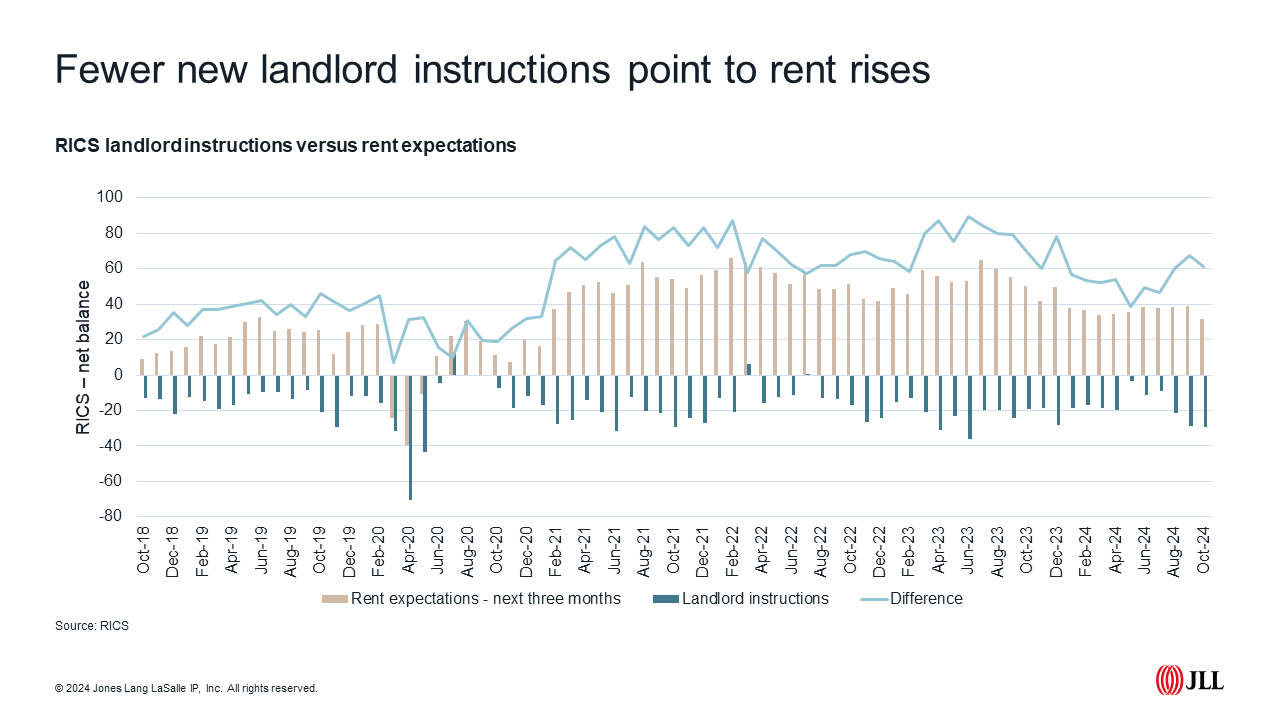

For lettings, results from the October survey show tenant demand rising in the three months to October, with more respondents seeing an increase than a fall, returning a positive net balance of +19%. But there were fewer landlord instructions, possibly reflecting pre-Budget caution from landlords, with a net balance of -29% of agents reporting a fall in the three months to October. The most negative figure for three years. Unsurprisingly, with demand increasing and fewer instructions, respondents were more optimistic about the prospect for rent rises in the coming months. A balance of +33% of agents expecting rents to rise over the next three months.

The ONS rental index (all lets) shows rents up 8.4% annually, but new lets (via Homelet) are showing a 3.4% annual increase nationally. For sales, Nationwide show prices up 2.4% annually with Halifax figures suggesting higher growth of 3.9%.

Base rates fall but fixed rates rise

In the run up to the Monetary Policy Committee meeting on 7th November most were forecasting a further reduction in the base rate. Even with a mixed reaction following the budget this view didn’t waiver much and was confirmed with a 25bps reduction. The MPC members voting eight to one to reduce rates (the one voting to stick). But messaging from the MPC suggests chances of a further 2024 reduction when they next meet on 19th December remain slim.

The November drop is good news for those on variable or tracker rates, but for those shopping for fixed rates a rise in swap rates, which started to build pre-Budget, means a host of lenders have increased their fixed rates. At the time of writing most sub 4% five-year fixes have been pulled from the market, rates are still lower than the 4.7% best-buys a year ago but expect them to sit slightly higher until we have some clarity on swaps.

Starts drop in London

A new approach to measuring housing need in London suggests we should be targeting 80,000 completions a year in the capital. But Molior London figures show housing starts in London so far this year (January to September) are down 53% on the ten-year average. Figures from the GLA show the number of affordable housing starts in the six months to September 2024 fell 23% on 2023 levels, with just shy of 2,700 affordable homes completed. Over the same six-month period there were just 582 GLA-funded affordable homes started, up on 2023 levels but nowhere near target. Expect continued scarcity in the London new homes market until we see an uptick in activity.

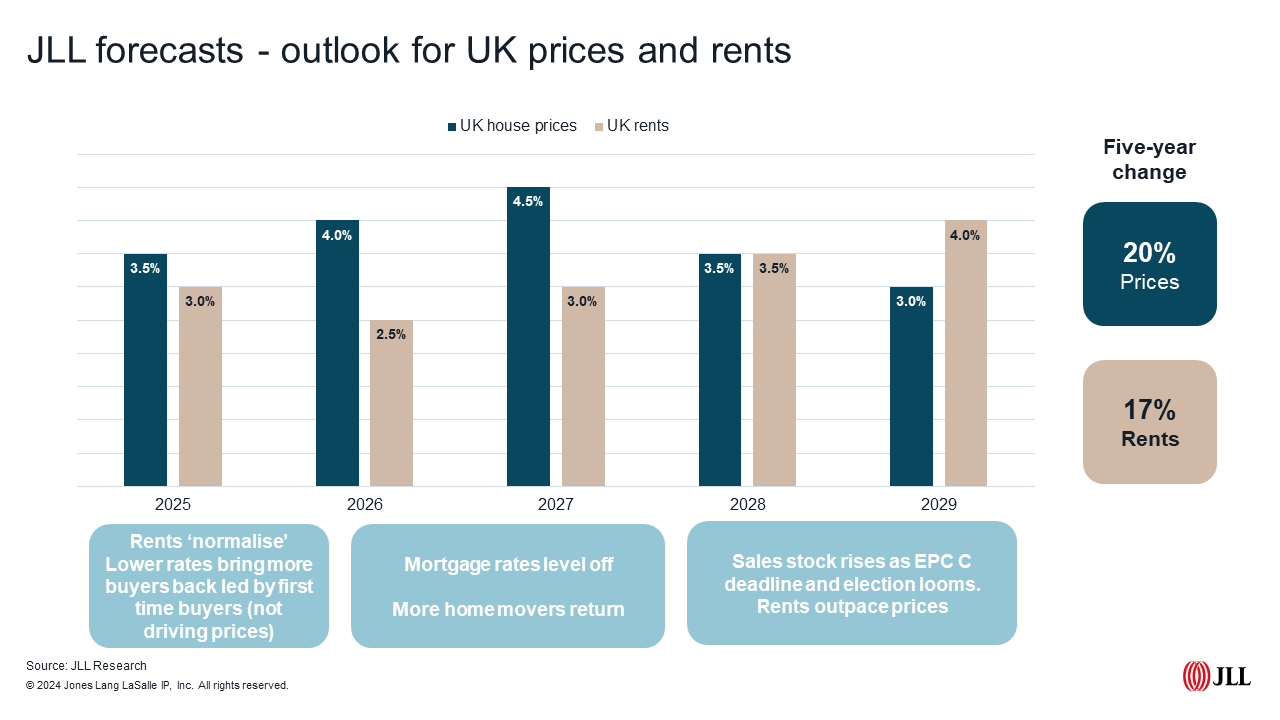

Updated JLL forecasts

Back in May our revised forecast coincided with the announcement of a UK General Election and in November we were upstaged again when our forecast launch fell on the same day as the US election.

So, for those who may have missed it, our updated 2025 to 2029 forecast expects activity to increase steadily from 2025 onwards, with prices up 20% and rents up 17% by the end of the five-year forecast period. To read more on our latest outlook for 2025-2029 click here.