The Autumn Budget is still more than two months off, but the rumour mill is in full swing. Press reports suggest the government is considering a replacement for Stamp Duty Land Tax (SDLT), a new fairer approach to council tax and a revision to Capital Gains Tax for higher value homes.

One of the proposals replaces SDLT with a new national tax to be paid by owner occupiers on houses worth more than £500,000 when they sell their home. The proposed levy would vary dependent upon the value of the property, but the complexity of implementation would mean it would take years rather than months to phase out the current system. And with a government looking for an increase in income in the short term, it could well find itself back on the shelf.

Many in the industry (including us here at JLL) have been advocating for an overhaul of property taxes for some time now. So, news that in advance of the budget the Treasury is looking at different aspects of property taxation should be welcomed. However,

the focus on higher value properties, a sector of the market where purchasers are often most discretionary, could lead to some shelving their plans until we have further clarity. Not helpful for an already sluggish market.

The case for stamp duty reform

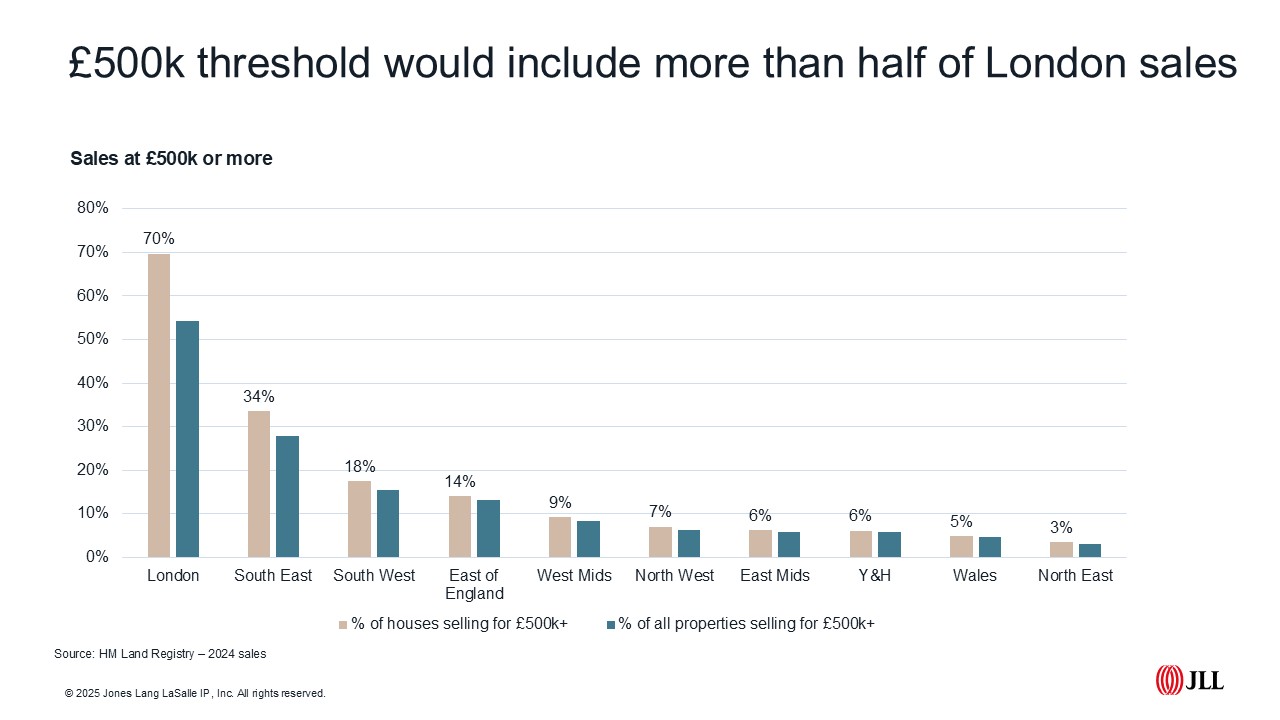

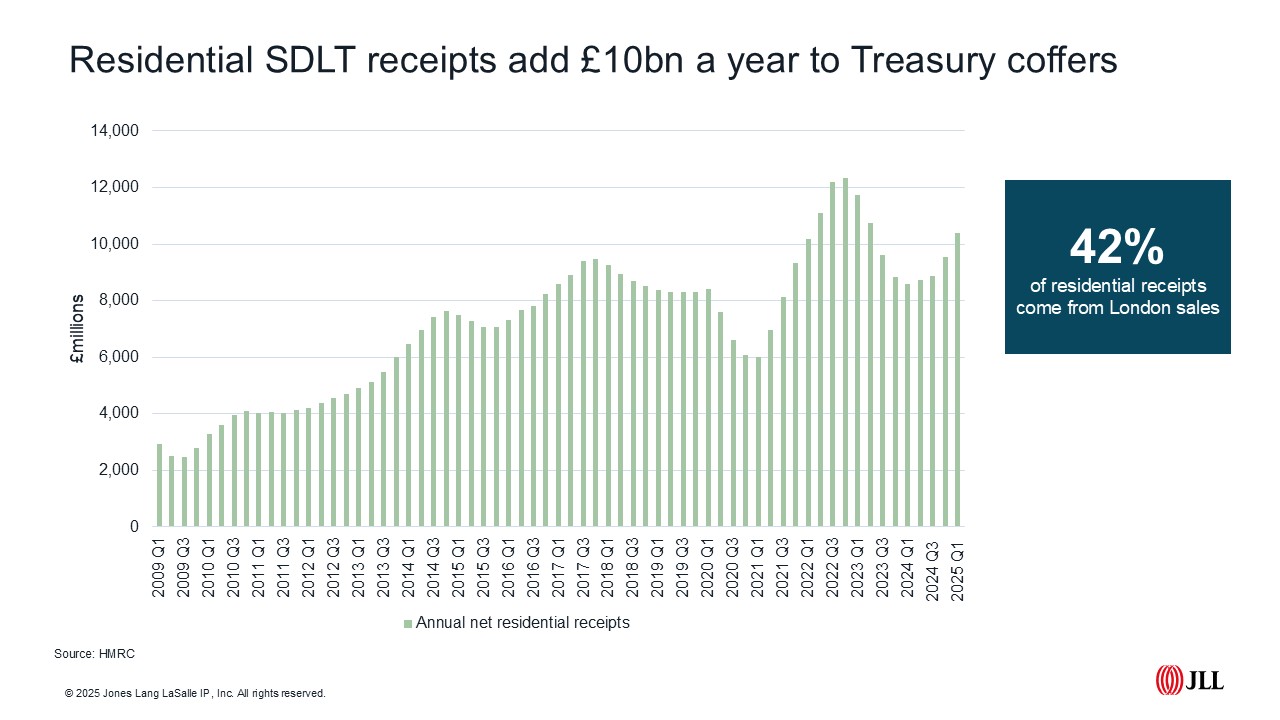

Stamp Duty on residential property added more than £10bn to government coffers in the year to March. But an increase in buying costs has meant fewer homes transacting, bad news for labour mobility and the many industries which rely on an active and fully functioning housing market. This is particularly true for London, which accounts for just over 10 per cent of UK sales but more than 40 per cent of SDLT revenues.

An overhaul of buying costs (SDLT) and holding costs (mainly council tax) is long overdue. But setting new valuation thresholds (effectively valuing every home) has been put in the ‘too difficult’ pile each time it’s been mooted by governments of all colours since the first set of 1991 property values were applied.

The latest idea purportedly under consideration takes inspiration from the work by think-tank Onward, which advocates replacing stamp duty and council tax (in part) with a national property tax for homes valued at more than £500,000. This would roll up and be paid once the property was sold. Revenues would be split between local government and the Treasury, with a minimum rate set to mirror revenue currently collected through council tax, effectively shifting the current purchasing cost (SDLT) to a sales cost (national tax). An obvious advantage for those purchasing their first home or upsizing but doing little to encourage downsizing.

Proposals exempt social housing, with tax for tenanted properties paid by the owner rather than the occupier (meaning private landlords with homes valued at over £500,000 would pay rather than the tenant – albeit likely just added to rent).

The challenge for government will be keeping the Office for Budget Responsibility happy, as the scrapping of SDLT could result in lower revenues in the short term.

Housing market

All this speculation isn’t helpful for a market where buyers remain cautious - the latest residential survey from the RICS painting a gloomy picture for activity in July. Rightmove figures, while still mixed, are a bit more positive, particularly for those vendors willing to be more realistic with their asking prices. There’s more stock on the market this year than last, with homes for sale up 10 per cent, a ten-year high. More choice means properties not priced competitively are failing to attract buyers, with more than a third of properties for sale having been reduced in price, the highest for two years. Asking prices dropped 1.3 per cent in August, in line with the usual seasonal trend, albeit following more substantial price cuts in June and July. Asking prices are now almost £10,800 lower than they were last summer.

But more competitive asking prices are encouraging buyers to commit, with sales agreed in July up 8 per cent on the same period in 2024 and their highest since 2020.

Latest figures from the ONS put UK house prices 3.9 per cent higher annually in June, up from a revised 2.7 per cent in May. Private rents rose 5.9 per cent in the year to July according to ONS figures, with the rate of growth slowing to levels last seen in early 2023. Rents for new lets remained broadly unchanged over the last 12 months, with Homelet data showing rents 0.4 per cent higher this July than last.

In other news

UK inflation rose to 3.8 per cent in July. This was marginally above the 3.7 per cent consensus forecast but in line with the latest Bank of England view, which expects UK inflation to peak at 4 per cent in September. Food, fuel and airfares appear to be the main culprits in July, all of which came in hotter than forecasters had predicted.

What this means for the rate cutting cycle is far from clear, it likely narrows the odds on a further cut in September, but there will be two further data releases prior to the November meeting, where expectations remain broadly positive for a further 25bps drop.

JLL Research